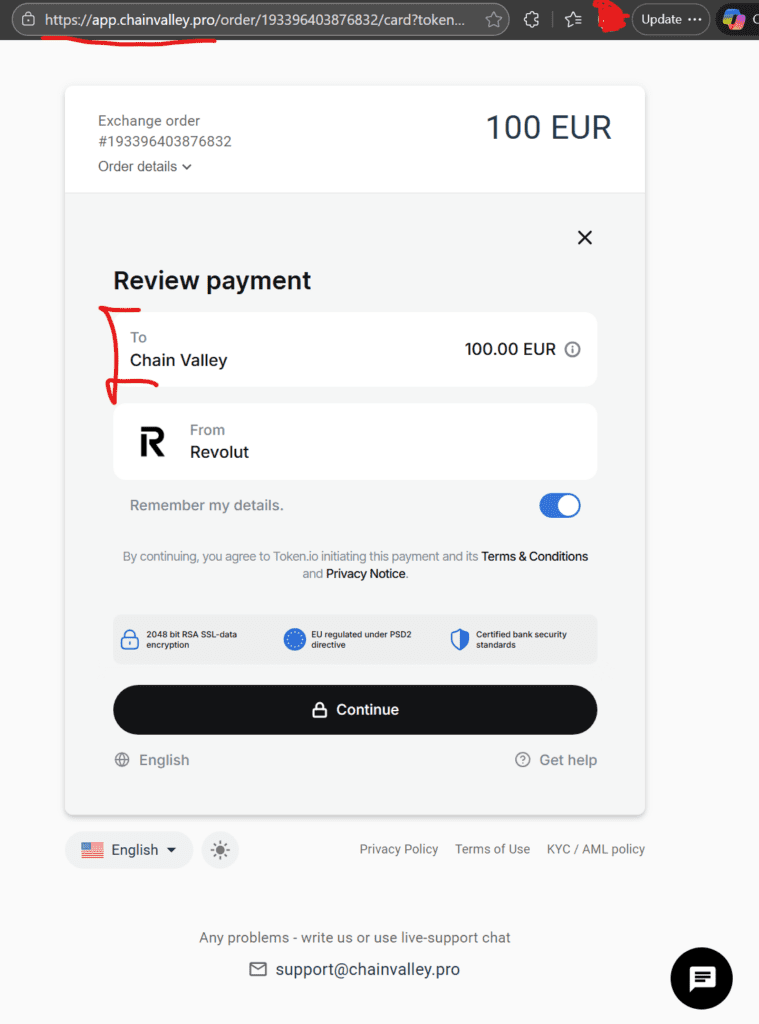

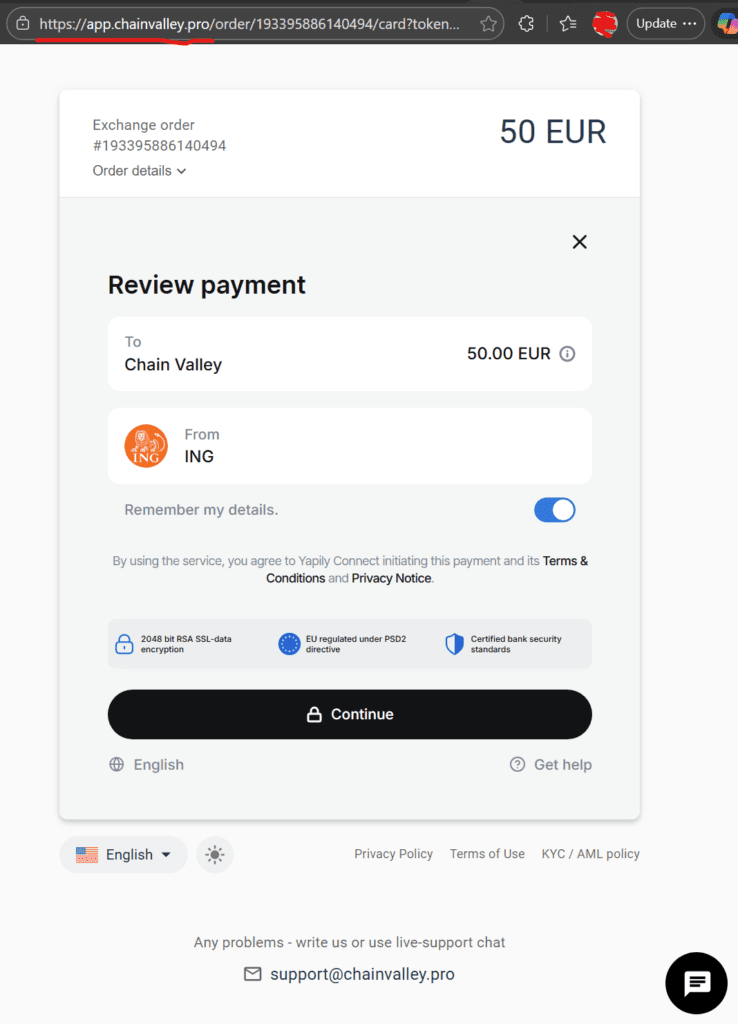

FinTelegram’s review of the offshore casino Rooli (rooli.com), operated by Curaçao-based Dama N.V., shows a recurring Open Banking pattern: the player’s bank transfer is made to “Chain Valley” as the recipient. In multiple flows, the deposit confirmation screen identifies Chain Valley as payee while the payer is a retail bank (e.g., Revolut, ING). That is not a neutral technicality—it is a compliance chokepoint.

Key Facts

- Illegal casino activities: Rooli is an offshore casino without license or permission to operate in the UK, EU, or in North America.

- Observed Rail: Player chooses Open Banking in Rooli cashier → payment initiation screen → “To: Chain Valley” (payee) → funds leave player’s bank (e.g., Revolut/ING) and land at Chain Valley. (Confirmed by screenshots.)

- Entity: Chain Valley Sp. z o.o. (Warsaw) operates chainvalley.pro; terms identify KRS 0001036419 and Warsaw address.

- Status in Poland: Chain Valley is listed in Poland’s virtual-currency activity register (RDWW-765, entry date 25.05.2023) with services including exchange between “virtual currencies and means of payment” and related intermediation.

- Regulatory reality check: Poland’s Ministry of Finance has explicitly warned that virtual-currency activity in this register is not “licensed or supervised” as a financial licence; oversight is primarily AML/CFT compliance control.

- Operator context: Rooli states payments are processed via Dama N.V. (Curaçao) and places the legal burden on players to assess legality in their jurisdictions.

- Pattern signal: ChainValley previously surfaced in FinTelegram’s Legiano rail investigation (FIAT→USDC “conversion” narrative risk).

Illegal Casino Activities

First, it must be stated plainly: the underlying activity being funded is unlawful in large parts of the market. Rooli—like many Dama-branded casinos—appears to accept players and deposits from multiple EU jurisdictions without holding the required local gambling authorisations. In our review, registration and funding from EU-based banks worked without meaningful friction, while the cashier dynamically surfaced EU languages and bank options tailored to those jurisdictions.

That combination is a strong indicator of active cross-border targeting rather than accidental access. If the gambling offer is not lawfully authorised where the player is located, then the payment rail is not a neutral utility—it becomes an enabler. Payment facilitators and open-banking intermediaries should therefore treat Dama/Rooli exposure as a high-risk, often non-permissible use case and apply refusal and off-boarding controls accordingly.

Yet the operational reality we observe is different: “open banking,” “instant banking,” and crypto on-ramps are increasingly used to route around local licensing, card gambling blocks, and merchant scrutiny—making the regulatory perimeter look optional when it is not.

Short Analysis

- The compliance issue is the payee. In the Open Banking flow, the recipient of the transfer is Chain Valley—not the casino, not a licensed EU payment institution branded as merchant acquiring, not an e-money wallet with regulated safeguarding disclosures. That means ChainValley functionally sits as a collection account / payment agent for casino deposits (or as a “merchant of record” via a “crypto purchase” wrapper). Either way, this is a high-risk typology for circumventing gambling blocks: bank statements show “Chain Valley,” not “casino.”

- VASP registration ≠ right to run FIAT payment rails. Under PSD2, payment services in the EU must be provided by authorised/registered payment service providers in scope of the directive. ChainValley’s publicly visible positioning is crypto-service (KYC/AML policy; “buy crypto”; APMs including instant bank transfers). If casino deposits are being routed through a VASP-labeled “crypto purchase,” regulators and banks should treat this as regulatory arbitrage: gambling funding disguised as crypto on-ramp activity.

- Who should be asking hard questions (now):

- Chain Valley: Who is the ultimate beneficiary of these casino-related transfers? Is ChainValley the merchant of record? Are transfers credited as casino deposits or as crypto buys? What is the settlement path to Dama/its PSP stack?

- Open Banking enablers: Why is a casino cashier initiating payments where the payee is a crypto VASP? What enhanced due diligence is applied for unlicensed/offshore gambling exposure?

- Banks: Why are repeated transfers to “Chain Valley” not treated as potential gambling funding / third-party collection patterns requiring review?

Call for Information

Do you work at ChainValley, an Open Banking provider, a bank risk team, or an offshore casino payment desk—and have documentation on how these “To: Chain Valley” deposits are booked (crypto purchase vs. casino funding), settled, and screened? Send evidence securely via Whistle42.com (screenshots, transaction references, merchant agreements, settlement files, risk rules).

{kind=link}