AXIOM’s “Buy Crypto” function appears to be far more than a simple widget. In substance, it works as a fiat deposit rail into AXIOM’s DeFi-branded trading stack, using Dutch aggregator Onramper and licensed or registered onramp partners to move users from card, bank, or wallet-based payment into immediate crypto trading access. For regulators and compliance analysts, the key issue is obvious: when a platform structures, controls, and monetizes that funding journey, the “DeFi” label alone may no longer be enough to keep it outside MiCA’s reach.

Key Findings

- FinTelegram’s March 13, 2026 review found that AXIOM could be accessed by EU users from multiple jurisdictions, with signup via email or Google and no meaningful onboarding friction before access to the deposit flow.

- AXIOM’s direct crypto deposit rail appears to accept transfers in multiple assets without platform-level KYC at the point of wallet funding.

- AXIOM’s fiat deposit path is effectively outsourced to Onramper, which dynamically routes users to third-party fiat gateways.

- Onramper publicly describes itself as a Netherlands-based fiat-to-crypto aggregator with 130+ payment methods, coverage in 190+ countries, and 30+ gateway partners.

- Onramper’s own terms say it is not a fiat gateway, is not party to the user’s transaction with the selected provider, and does not take custody of user funds.

- AXIOM and Onramper publicly announced their partnership in December 2025, describing the integration as a seamless way for AXIOM users to top up BNB and SOL with localized payment methods.

- Ramp Network states that Ramp Swaps (Ireland) Limited received MiCA CASP authorisation from the Central Bank of Ireland in December 2025, and the AMF’s whitelist confirms its passporting into France.

- Swapped publicly presents itself as registered with AUSTRAC, FinTRAC, FinCEN/NMLS, and Norway’s FSA, which supports the view that at least part of AXIOM’s rail is being executed by regulated or registered partners rather than by AXIOM itself.

- Topper is marketed by Uphold as a regulated fiat on-ramp product within the Uphold group.

- Link’s support materials say users can buy crypto on Link-supported sites from third-party exchange providers, which suggests Link acts as a checkout/payment layer rather than the crypto counterparty itself.

Compliance Analysis

AXIOM’s “Buy Crypto” Rail Is Functionally A Fiat Deposit Channel

FinTelegram’s review indicates that AXIOM’s “Buy Crypto” feature should not be treated as a minor convenience tool. In substance, it operates as a fiat deposit rail into AXIOM’s trading environment.

The user journey is simple and commercially coherent. A user enters AXIOM, chooses a fiat funding option, is routed through Onramper’s aggregation layer, completes payment and any partner-level KYC with the selected provider, and then receives crypto into the wallet environment used for AXIOM trading.

That matters. Even if the fiat-to-crypto conversion is legally executed by third-party providers, the overall structure functions as a funding funnel into AXIOM. In practical terms, AXIOM’s “Buy Crypto” feature looks far less like a peripheral widget and far more like an integrated deposit mechanism.

Read our initial AXIOM compliance report here.

The Real MiCA Question Is Control, Not Branding

This distinction is central under MiCA. Recital 22 does not create a safe harbor merely because parts of a service are decentralized or outsourced. The real question is whether crypto-asset services are performed, provided, or controlled, directly or indirectly, by identifiable persons.

That is where AXIOM becomes problematic.

AXIOM’s own materials identify Axiom Innovations Inc. as the company behind the service. At the same time, AXIOM markets itself as a trading platform and hybrid wallet product. This means it is not just a neutral protocol endpoint or a piece of passive software. It is an identifiable commercial interface that structures access to funding, wallets, and trading.

From a compliance perspective, AXIOM therefore cannot rely on “DeFi” branding alone. The stronger and more defensible reading is that AXIOM presents a serious MiCA perimeter-risk case because it appears to organize access to crypto-asset services for users, including EU-based users, through a branded and operationally integrated front end.

Onramper’s Formal Position: Aggregator, Not Gateway

Onramper’s role is more nuanced. On paper, Onramper presents itself as a technical aggregation and routing layer. Its public materials describe a widget and API solution that compares providers dynamically based on geography, payment method, pricing, and conversion probability.

Its legal positioning is drafted with care. Onramper says it is not itself the fiat gateway, not a party to the user transaction, does not settle the transaction, and does not take custody of user fiat or crypto.

Formally, that is a classic infrastructure model. It is designed to keep Onramper outside the legal role of exchange, broker, or custodian.

The Practical Reality Looks More Complicated

The difficulty is that FinTelegram’s March 2026 testing suggests the practical reality may be more complex than the contractual wording implies.

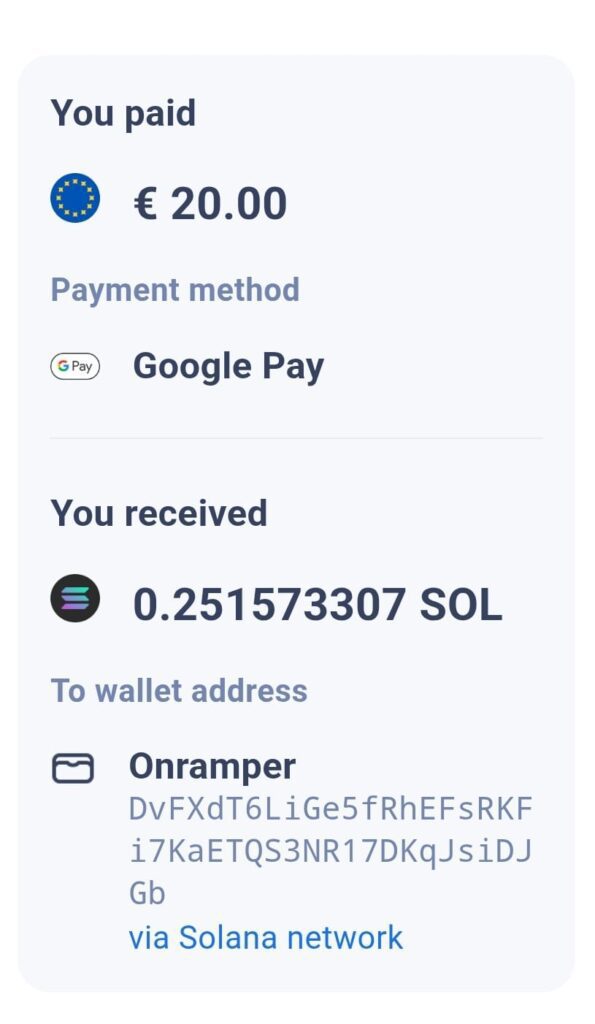

The AXIOM-Onramper flow appears to prefill the destination wallet. More importantly, the TopperPay payment confirmation (screenshot left) suggests that the purchased SOL was first sent to a wallet labeled for Onramper before appearing in the AXIOM context.

That is a relevant compliance signal.

If the purchased crypto is routed through an operational wallet, forwarding wallet, or omnibus wallet within the onramp stack, then the process may involve more than neutral comparison technology. It may amount to transaction orchestration with wallet-layer intermediation.

That does not prove, on the currently available evidence, that Onramper legally acts as a custodian. But it does raise legitimate questions about who controls the destination wallet, who determines the delivery path, and whether any entity in the chain momentarily receives, directs, or operationally handles crypto on behalf of the user or AXIOM.

Those questions are material under MiCA, AML/CFT analysis, and safeguarding logic.

The Cleanest Reading Of The Rail

Based on the available evidence, the clearest regulatory reading is this:

- The third-party onramp partners appear to be the regulated or registered execution entities for the fiat-to-crypto purchase.

- AXIOM appears to be the commercial destination platform that owns the user relationship and provides the trading environment.

- Onramper appears to be the technical routing and orchestration layer connecting users to execution partners.

That structure is important because the presence of licensed or registered partners inside the payment rail does not solve AXIOM’s own perimeter problem.

MiCA does not only concern the entity that books or settles the conversion. It can also capture the entity that commercially organizes access to crypto-asset services through a branded interface. That is precisely why AXIOM cannot simply point to Ramp Network, Topper, MoonPay, Swapped, or Link by Stripe and argue that compliance stops there.

Read our reports on Swapped here.

If AXIOM structures the rail, predefines the wallet logic, captures the client relationship, and converts fiat onboarding into immediate trading access on its own platform, regulators may reasonably ask whether AXIOM is operating as a brokerage-adjacent or platform-style access layer in substance.

The stronger legal formulation is therefore not that AXIOM has already been definitively found to be an unauthorized CASP. It is that AXIOM presents a serious and visible MiCA perimeter-risk profile.

Onramper Is A Material Boundary Case

A similar logic applies to Onramper.

Its terms are clearly designed to frame the business as technical infrastructure only. That may be correct as a matter of formal legal design. But supervisors do not assess risk solely through disclaimers. They also look at operational reality.

If an aggregator goes beyond neutral comparison and becomes deeply embedded in user-flow control, provider recommendation, wallet handling, conversion optimization, and transaction routing inside third-party trading platforms, then it starts to move closer to a regulated intermediation problem.

For now, the most defensible conclusion is that Onramper is a material boundary case.

On the available evidence, it does not appear to be the principal crypto seller. But neither does it look like a trivial software plug-in. Its role appears central to AXIOM’s fiat entry architecture, and that alone makes it compliance-relevant.

The Partner Layer Looks Stronger Than The Platform Layer

The onramp partner layer appears stronger on paper. Ramp Network is MiCA-authorized in Ireland and passported into France. Swapped presents itself as registered across several jurisdictions. Topper sits within the Uphold group’s regulatory perimeter. Link by Stripe appears to function primarily as a payment and checkout layer rather than the direct crypto counterparty.

That means the weakest link in the AXIOM rail is not necessarily the formal status of the payment partners themselves.

The more sensitive issue is the combined AXIOM-Onramper model: a DeFi-branded trading platform using a localized, partner-driven fiat onboarding stack to feed users directly into a trading environment that does not appear to have visible EU authorization of its own.

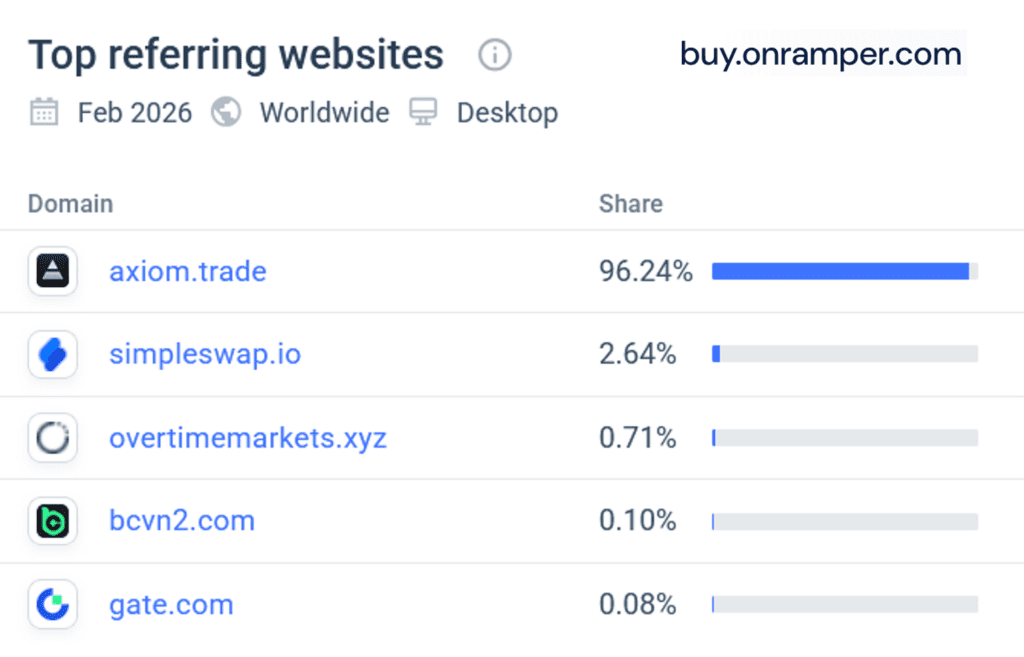

The Traffic Pattern Supports The Integrated-Rail Thesis

FinTelegram’s traffic findings support that interpretation. If AXIOM accounts for the overwhelming majority of referral traffic into buy.onramper.com, then Onramper is not incidental to AXIOM’s business model. It is a core access rail.

That concentration strongly suggests that AXIOM’s “Buy Crypto” function is not a loose affiliate arrangement or a detached third-party tool. It is an integrated fiat onboarding funnel.

Combined with AXIOM’s sizeable traffic and visible EU user participation, that increases the relevance of MiCA and UK perimeter questions, even if the formal fiat-to-crypto leg is executed by licensed partners.

Summary Compliance Statement

FinTelegram’s March 2026 review indicates that AXIOM’s “Buy Crypto” feature functions in substance as a fiat deposit rail into a DeFi-branded trading environment. While regulated or registered partners appear to execute the fiat-to-crypto leg, that does not remove AXIOM’s own MiCA perimeter risk.

AXIOM captures the user relationship, structures the funding journey, and channels users directly into its trading stack. Onramper, meanwhile, appears to act as a central routing and orchestration layer and should be viewed as a material boundary case rather than a neutral plug-in. The overall result is a sophisticated fiat onboarding architecture feeding a platform that, on the currently visible facts, remains outside any clearly identifiable EU authorization framework.

Summary Table: AXIOM And Its Payment Rails

| Element | Observed / Reported Role | Regulatory / Compliance View |

|---|---|---|

| AXIOM | Trading platform and hybrid wallet interface; destination environment for funded users. | Serious MiCA perimeter-risk case if it is organizing access to crypto-asset services for EU users without authorisation. |

| Onramper | Dutch aggregation/routing layer embedded in AXIOM’s “Buy Crypto” rail; selects provider/payment path dynamically. | Publicly positions itself as non-custodial technical infrastructure, but in practice appears central to user onboarding and transaction flow. |

| Topper, TopperPay / Uphold | Fiat-to-crypto execution partner observed in FinTelegram’s test purchase. | Appears to sit within a more mature regulated environment than AXIOM itself. |

| Ramp Network | Suggested partner for bank transfer / Apple Pay / Google Pay flows in review. | Ramp Swaps (Ireland) Limited states it holds MiCA CASP authorisation; AMF whitelist confirms passporting into France. |

| Swapped | Suggested onramp partner in reviewed flows. | Publicly states registrations with AUSTRAC, FinTRAC, FinCEN/NMLS, and Norway FSA; not the same as saying it solves AXIOM’s perimeter issue. |

| MoonPay | Presented in AXIOM/Onramper flow for some payment methods and also referenced by AXIOM’s broader partner mix. | Regulated partner model strengthens execution side, but not AXIOM’s own authorisation posture. |

| Link by Stripe | Checkout/payment layer shown for debit-card crypto purchase routes. | Appears to support crypto purchases from third-party providers rather than acting as the crypto exchange itself. |

| User KYC | Partner-level KYC observed in FinTelegram’s test, but not AXIOM-level KYC before accessing rail. | Suggests compliance is pushed outward to providers, while AXIOM retains commercial front-end relationship. |

| Wallet handling | Review screenshots suggest destination wallet data is prefilled via the rail and may involve an Onramper-labelled wallet in the payment path. | Raises unresolved questions about custody, forwarding, settlement flow, and wallet control. |

| Overall structure | AXIOM front end → Onramper routing layer → licensed/registered onramp partner → crypto delivered into AXIOM trading context. | Functionally resembles a fiat deposit funnel into a DeFi platform. |

Call To Whistleblowers

Do you have internal information about AXIOM, Onramper, Topper, Ramp, Swapped, MoonPay, Link by Stripe, or other entities involved in AXIOM’s buy-crypto rail?

FinTelegram is particularly interested in:

- internal routing logic and wallet-handling architecture,

- custody or forwarding arrangements,

- KYC/AML escalation procedures,

- partner contracts,

- country blocking or geo-targeting policies,

- compliance opinions on MiCA perimeter exposure,

- suspicious transaction monitoring and sanctions screening,

- how AXIOM users are classified inside the payment stack.

Share information confidentially with FinTelegram via Whistle42.

{kind=link}