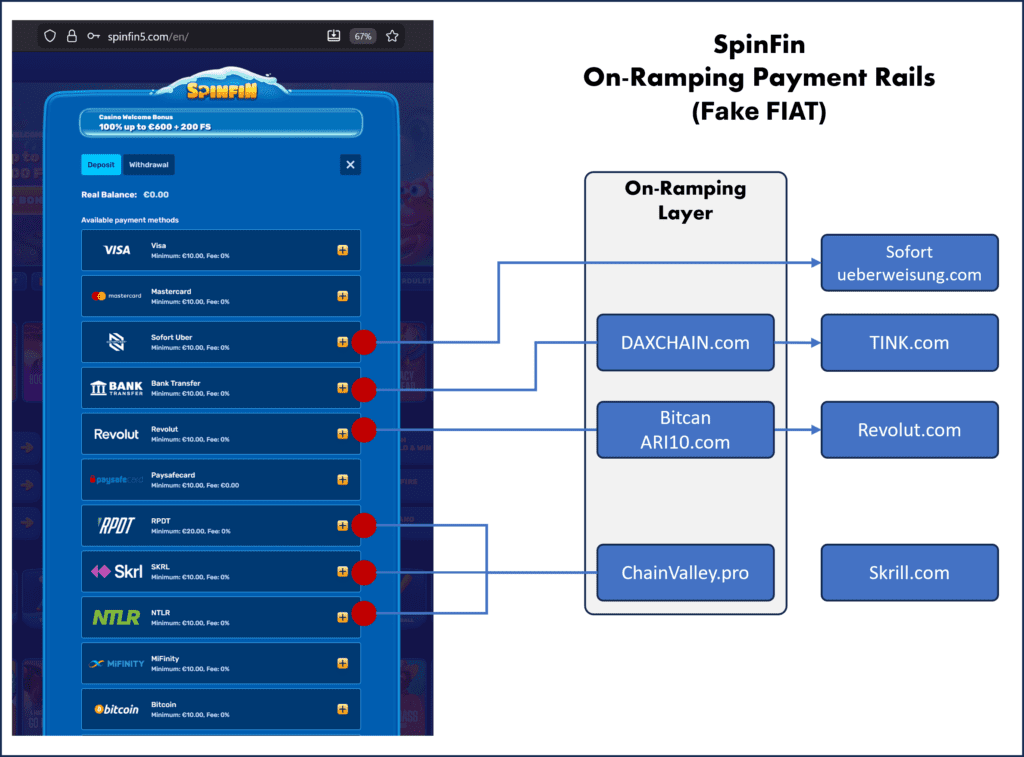

A fresh cashier review of the SpinFin offshore casino (accessed via SpinFin5.com) shows a familiar pattern: “FIAT” deposit labels that actually route players into fiat-to-crypto purchases and onward transfers to operator wallets. Screenshots confirm multiple on-ramping layers — including **DAXCHAIN OÜ using Tink, Chain Valley Sp. z o.o. issuing “exchange orders” behind Skrill/Neteller/Rapid, and Bitcan sp. z o.o. converting deposits into USDC while the UI still reads like a bank payment flow.

Key Points (evidence-led)

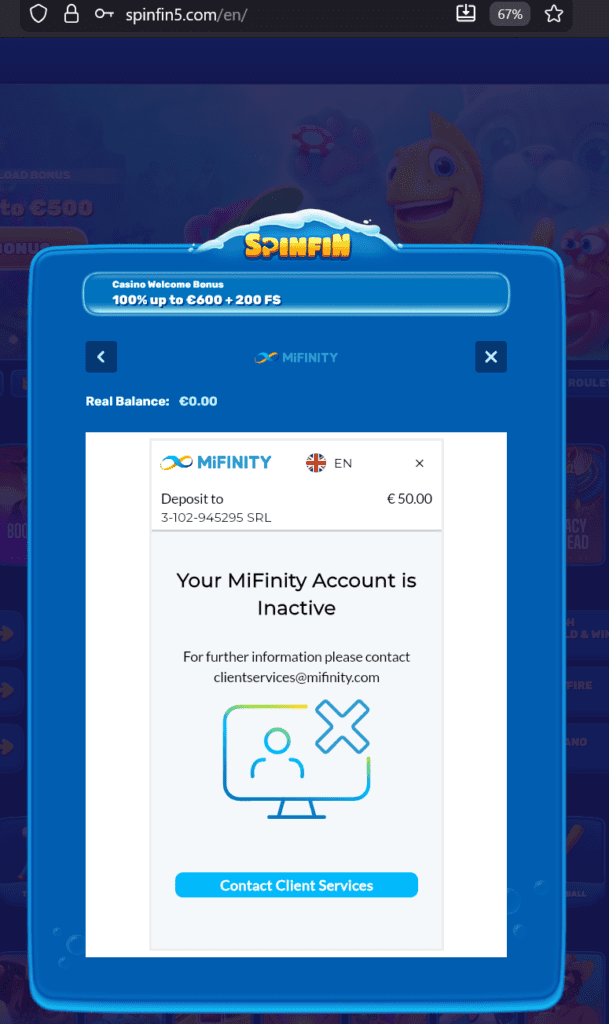

- Confirmed (screenshots): MiFinity deposits are directed to “3-102-945295 SRL” (shown as payee/recipient in the MiFinity overlay).

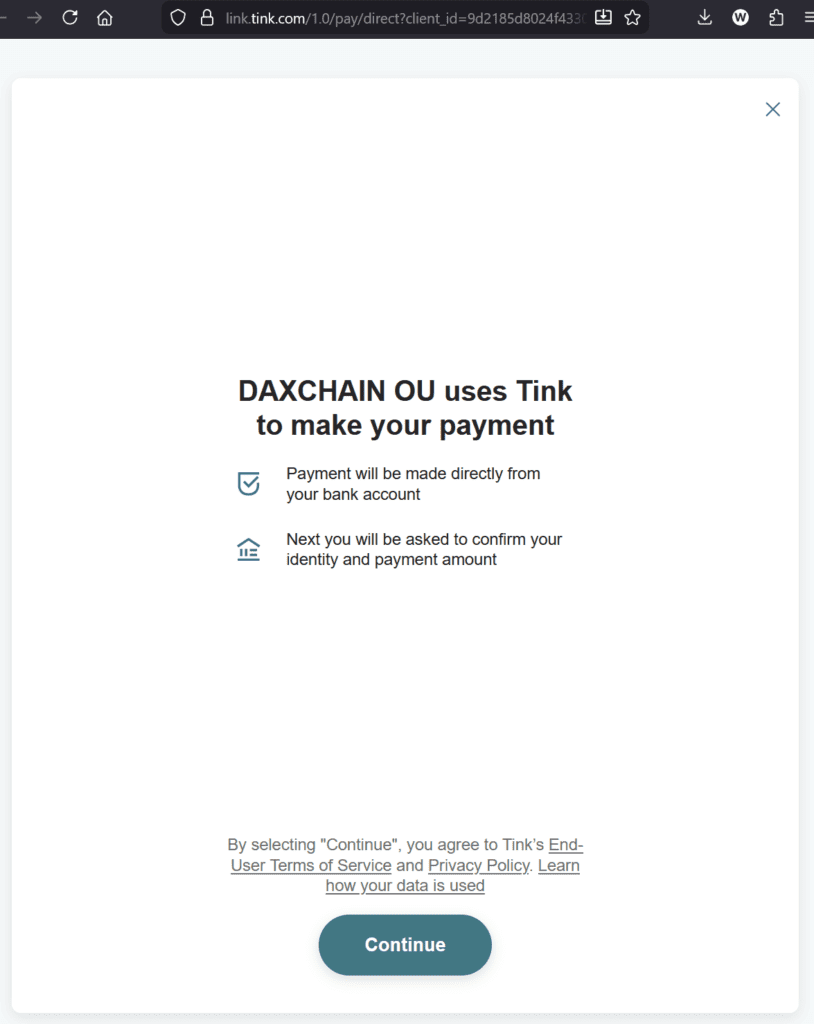

- Confirmed (screenshots): “Bank Transfer” routes into DAXCHAIN OÜ with a payment step stating: “DAXCHAIN OU uses Tink to make your payment” (open-banking payment initiation via Tink, now owned by Visa).

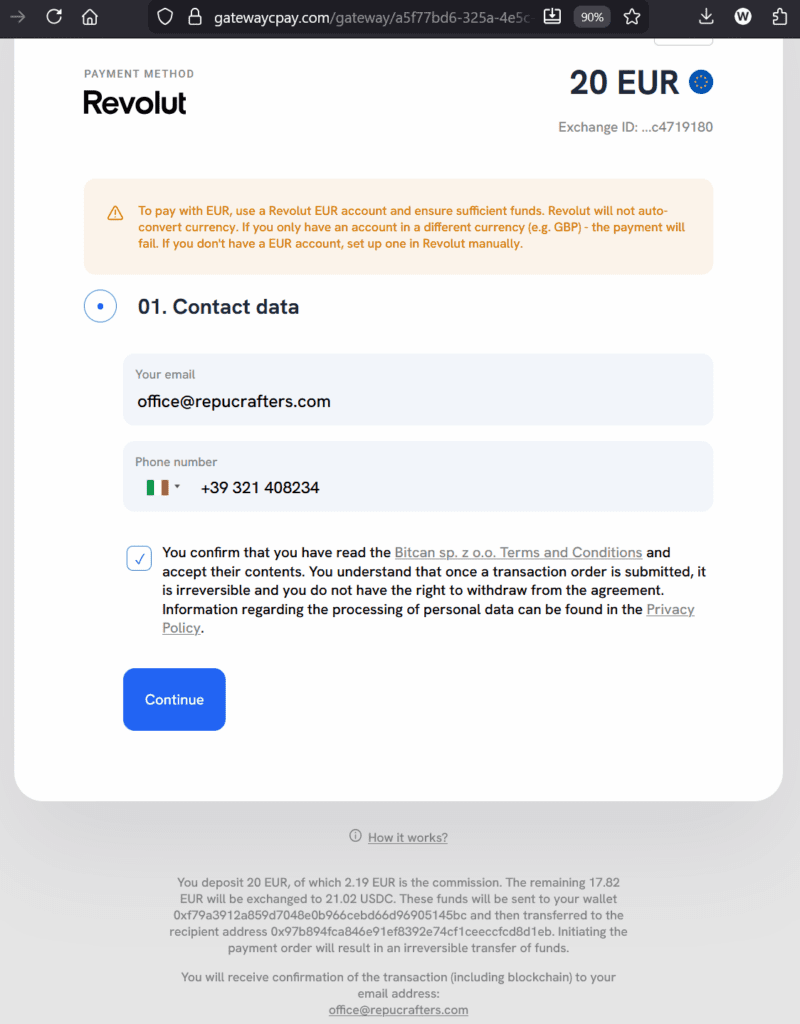

- Confirmed (screenshots): “Revolut” deposits open a gateway page that discloses a fiat→USDC conversion and an irreversible transfer to specified wallet addresses; the consent text references Bitcan sp. z o.o..

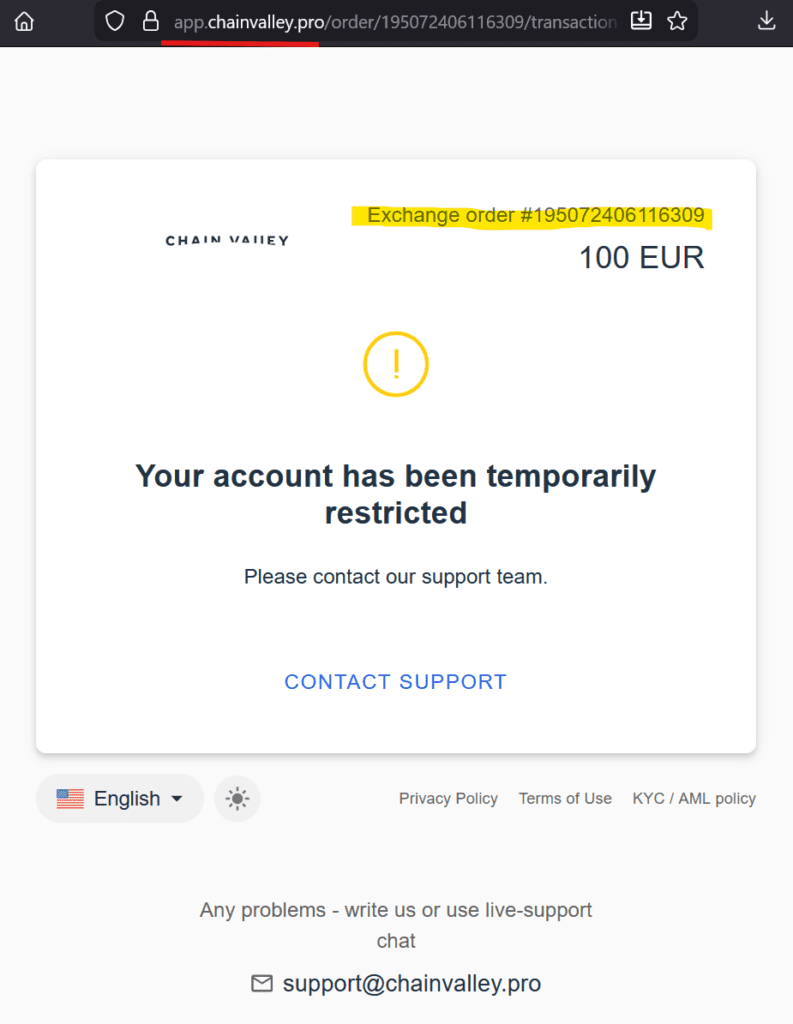

- Confirmed (screenshots): Skrill/Neteller/Rapid routes into a ChainValley “Exchange order” flow (app.chainvalley.pro) — we captured an exchange order page + a “temporarily restricted” notice with support contact.

- Change vs. Dec 2025 review (internal comparison): utPay is no longer visible in the cashier; ChainValley appears to have replaced the Skrill/Neteller/Rapid rail and is operated as a “fake FIAT” on-ramp (crypto purchase first, operator funding second).

- Macro driver: the replacement of Baltic-linked rails with Polish rails fits the broader MiCA transitional “timing gap” dynamic across EU member states.

Short Narrative

SpinFin’s cashier is not just a list of payment buttons — it’s a routing layer. Players click “Bank Transfer,” “Revolut,” “Skrill,” or “MiFinity,” but the transaction logic quickly shifts into crypto on-ramps (USDC conversion, exchange orders, and wallet settlement). The resulting effect is predictable: regulated bank rails do the collection, while crypto rails do the delivery — often with the casino deposit narrative preserved on the front-end.

Your uploaded “SpinFin On-Ramping Rails (Fake FIAT)” graphic captures this dissolution well: multiple cashier labels converge into an on-ramping layer (DAXCHAIN / Bitcan-ARI10 / ChainValley), and only then into the branded payment systems (Tink / Revolut / Skrill).

Extended Analysis: Rail-by-rail compliance picture

1) MiFinity → “3-102-945295 SRL” (payee shown)

The MiFinity overlay in your screenshot shows “Deposit to 3-102-945295 SRL” (EUR 50). This strongly suggests the player is not depositing to a transparently identified EU/UK-licensed gambling operator but to an intermediary/agent entity.

This number-based Costa Rica-based entity is associated with the Tobique Gaming Commission (TGC) ecosystem. The TGC positions itself as a gaming regulator supporting Tobique First Nation economic development.

Compliance angle: Regardless of any offshore licensing narrative, this does not equate to a national gambling licence for the European Union or the United Kingdom — and the MiFinity UI provides no obvious “who is the gambling operator” disclosure at the moment of payment.

2) “Bank Transfer” → DAXCHAIN + Tink (open-banking initiation)

Your screenshot shows the intermediate step: “DAXCHAIN OU uses Tink to make your payment.”

This is a classic PIS/open-banking handoff: the player believes they are performing a bank transfer deposit confirming an amount; the rail actually routes to a crypto gateway that can complete a fiat-to-crypto conversion downstream.

Why this matters: open-banking payments are often treated as “safer” and “more bank-like” by consumers, but in this pattern they become collection rails for high-risk merchant categories (offshore gambling), with crypto used as the settlement path.

3) “Revolut” → Bitcan/ARI10 gatewaycpay flow (explicit USDC conversion)

This is the cleanest “fake FIAT” evidence in the set. The gateway page discloses:

- deposit amount (EUR 20),

- fee,

- conversion to USDC,

- transfer to a first wallet, then to a recipient wallet,

- and “irreversible transfer” language — while the UI still reads like a payment method choice.

FinTelegram has already documented this Bitcan/ARI10 stack (same gateway family) in other offshore casino contexts.

4) Skrill/Neteller/Rapid → ChainValley exchange order (replacement for utPay)

The ChainValley screenshot shows an exchange order (EUR 100) and a restriction banner — consistent with an on-ramp workflow rather than a pure wallet-to-merchant “casino deposit.” ChainValley’s own disclosures identify Chain Valley Sp. z o.o. and provide governance/AML language (including the ability to suspend/freeze transactions).

Additionally, ChainValley’s KYC policy indicates one-off transactions up to EUR 1,000 can be processed without establishing a “formal business relationship” (per their wording).

Key compliance read: If a casino cashier button quietly triggers a crypto purchase, then an onward transfer to an operator wallet, the “Skrill/Neteller/Rapid” labels risk becoming misdirection for:

- consumer understanding,

- bank AML monitoring,

- and regulator enforcement narratives (“we only take X method”).

Summary Table: PayFacs / On-Ramp Operators and Roles (SpinFin cashier)

| PayFac / On-Ramp | Legal entity & jurisdiction | What the user sees | What the rail appears to do | Evidence grade |

|---|---|---|---|---|

| MiFinity | Payee shown as “3-102-945295 SRL” (claimed offshore operator/agent; jurisdictional context points to Costa Rica in your review) | “MiFinity” deposit | Deposit routed to a third-party SRL entity (operator/agent carousel pattern) | Confirmed (screenshot) |

| DAXCHAIN | DAXCHAIN OÜ (Estonia) | “Bank Transfer” | Open-banking initiation via Tink (Visa group), consistent with fiat-to-crypto on-ramp | Confirmed (screenshot) + ownership context |

| Bitcan / ARI10 | Bitcan sp. z o.o. + ARI10 Sp. z o.o. (Poland) | “Revolut” | Explicit disclosure of EUR→USDC conversion + wallet settlement chain | Confirmed (screenshot) + background |

| ChainValley | Chain Valley Sp. z o.o. (Poland) | “Skrill / Neteller / Rapid” | “Exchange order” flow; appears to be crypto purchase first, casino funding second (“fake FIAT”) | Confirmed (screenshot) + company disclosures |

| Sofort Uber (as reported in review) | Destination cited as ISX Financial EU Plc (Cyprus), EMI regulated by Central Bank of Cyprus | “Sofort Uber” | Multiple gateway hops → bank account at a Cyprus EMI (collection layer) | Indicated (needs screenshot) |

| PaySafeCard (as reported in review) | SegoPay / pgway stack (domains provided) | “PaySafeCard” | Redirect through gateway domains to complete payment | Indicated (needs screenshot) |

Actionable Insight for regulators, banks, and PSPs

SpinFin’s cashier design suggests a standard laundering risk pattern: consumer-facing “payment method branding” + back-end crypto settlement. For compliance teams, the control point is not the casino UI — it’s the on-ramp entity and its bank/PIS providers.

Practical next steps:

- Bank/PSP monitoring: treat “casino deposit” narratives masked as “crypto purchase” as high-risk merchant behaviour, especially where stablecoins are the settlement instrument.

- Regulatory triage: focus on (a) cross-border offering to EU/UK users, (b) unclear merchant-of-record, and (c) systematic stablecoin routing to operator wallets.

- Evidence hardening: capture full checkout disclosures (T&Cs, payee identity, wallet destination) for each rail, and preserve session metadata.

Call for Information

If you have documentation showing (a) the contracting entity behind SpinFin5/SpinFin, (b) merchant-of-record disclosures, (c) wallet destination reuse across other casinos, or (d) bank/EMI accounts linked to these rails, please share it securely via Whistle42.com. Screenshots, email confirmations, and bank descriptors are particularly valuable.

{kind=link}