FinTelegram has expanded its review beyond Legiano and observed a repeatable pattern across multiple casino brands attributed to the operator Stellar Ltd: near-identical site structures, minimal operator disclosure, boilerplate “applicable law” clauses, and the same payment rails—most notably “fake bank transfers” facilitated by Polish Chainvalley that convert fiat into USDC.e and forward it to casino wallets. This report consolidates the pattern and explains why USDC.e adds bridge-risk on top of the already deceptive “fake-fiat” UX.

Key Facts

- Casino review aggregators attribute brands such as Ragnaro, Astromania, SpinFin (and others) to Stellar Ltd (Source: Online Casino Groups).

- Across Stellar-branded sites we reviewed, operator/jurisdiction disclosure is weak, and legal language is often generic or template-like—e.g., SpinFin’s terms literally include a placeholder “laws of [insert jurisdiction]” (Source: SpinFin Casino).

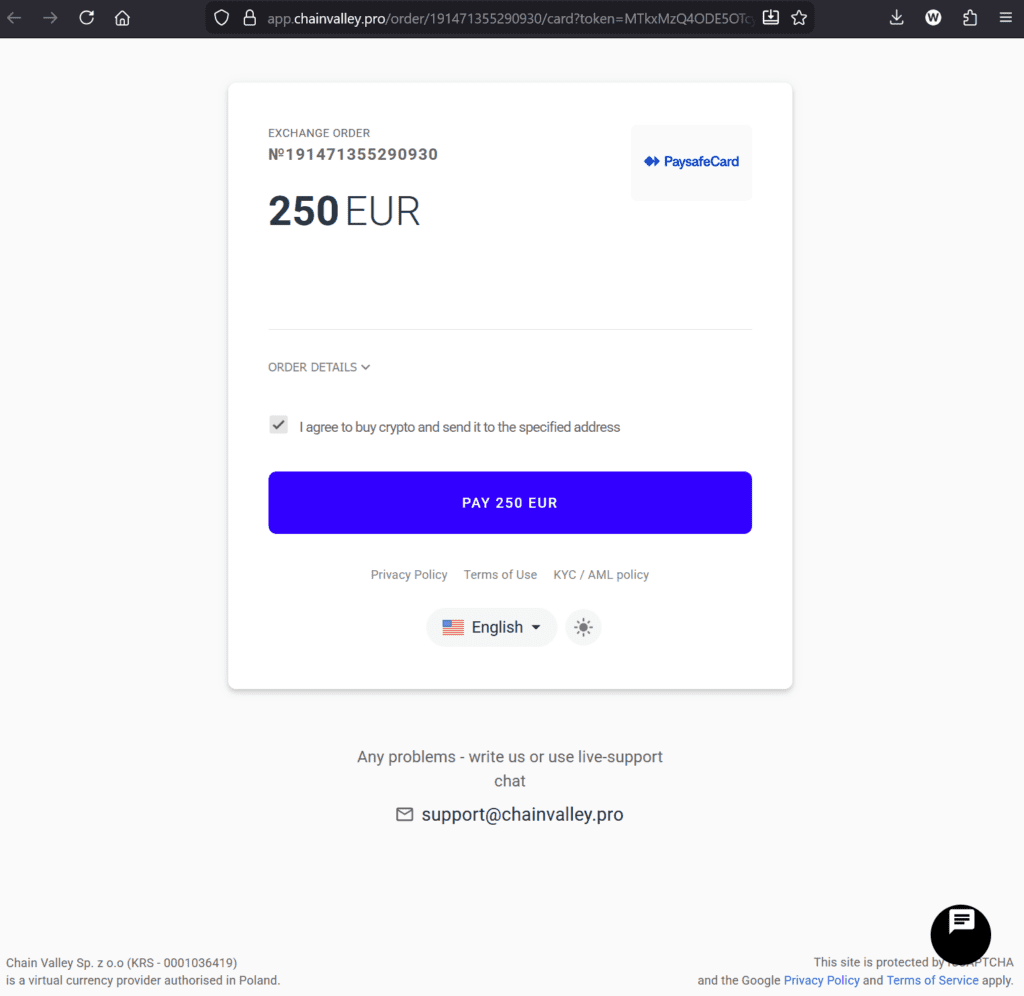

- The Legiano rail (already published) appears reusable across the network: utPay/Chainvalley checkout → Skrill/Neteller funding → USDC/USDC.e purchase → automatic transfer to casino walle (Source: FinTelegram, Chainvalley)

- In MiFinity-branded flows, FinTelegram again observed the payee CANAMONEY EXCHANGE LTD (Canada) d/b/a CenturaPay (Source: CenturaPay).

Read our Legiano reports here.

Short Analysis

1) “Anonymity by Design.”

A legitimate gambling operator typically discloses the licensed entity, the licensing authority, and a concrete governing law/jurisdiction. In the Stellar cluster, those anchors are frequently missing or diluted into non-answers (“applicable law”)—or left as template placeholders. This is not a cosmetic defect; it is a dispute and enforcement obstacle.

2) The Payment Architecture is the Same—Because it’s a Template

What players experience as a “bank transfer” or “fiat deposit” is, in practice, a crypto purchase executed through a third-party on-ramp and forwarded to a casino wallet. Chainvalley’s own terms contemplate delivering virtual currency to a user-specified wallet address and even freezing crypto/fiat under its rules—confirming the flow is built as an exchange/on-ramp product, not a casino deposit product.

For the player, the consequence is predictable: the transaction becomes “I bought crypto and received it,” not “I paid a gambling merchant,” which can undermine chargeback narratives and complicate complaints.

3) Why USDC.e is a second risk layer

FinTelegram’s screenshots show USDC.e being purchased in these cashier flows. USDC.e is typically “bridged USDC”—a representation created via third-party bridge mechanics, not native issuance on that chain. Circle’s own documentation and legal terms state that bridged USDC is not issued/redeemed by Circle and is not backed by Circle’s USDC reserves, adding dependency on bridge integrity (“bridge risk”) (Sources: Circle, Circle, USDC, Avalanche).

In short: fake-fiat rail + bridged stablecoin = less transparency, weaker redress, more technical failure modes.

Call for Information

FinTelegram is expanding the Stellar/Legiano case into a broader investigation of this casino template and its payment chokepoints. If you are a player, affiliate manager, PSP/acquirer insider, or have evidence about merchant descriptors, settlement accounts, token contract addresses for the “USDC.e” used, wallet clusters, chargeback outcomes, or payout/withdrawal issues across Legiano/SpinFin/Ragnaro/Astromania/MonsterWin and related brands, submit securely via Whistle42.com. We will publish dedicated deep-dive compliance notes on Chainvalley and CenturaPay/CANAMONEY as this case expands.

{kind=link}