2-Minutes Briefing

FinTelegram’s Rail Atlas has conducted an extended compliance review of The Kingdom Bank Corporation, a Dominica-based offshore/international banking and fintech institution publicly positioning itself toward global payments, digital assets, Forex, Gambling and iGaming.

In an operational review, FinTelegram was able to register with The Kingdom Bank as a resident of Austria and Italy. The onboarding flow used an external KYC verification domain, verify.kyxplatform.com, branded as Plato. The deposit area inside The Kingdom Bank portal offered several funding methods, including Binance Pay, Instant Bank Transfer, Bank Transfer, Crypto and Kingdom Cash.

For Instant Bank Transfer, the flow redirected to pay.banky.io, a Banky-branded account-to-account payment gateway listing numerous UK and fintech banks, including Lloyds Bank, Barclays, Santander, RBS, NatWest, Revolut, HSBC, Monzo, Nationwide, Starling Bank, TSB, Wise and others. In FinTelegram’s test, the instant bank transfer could not be executed and returned the error message: “Cannot execute payment at this time.”

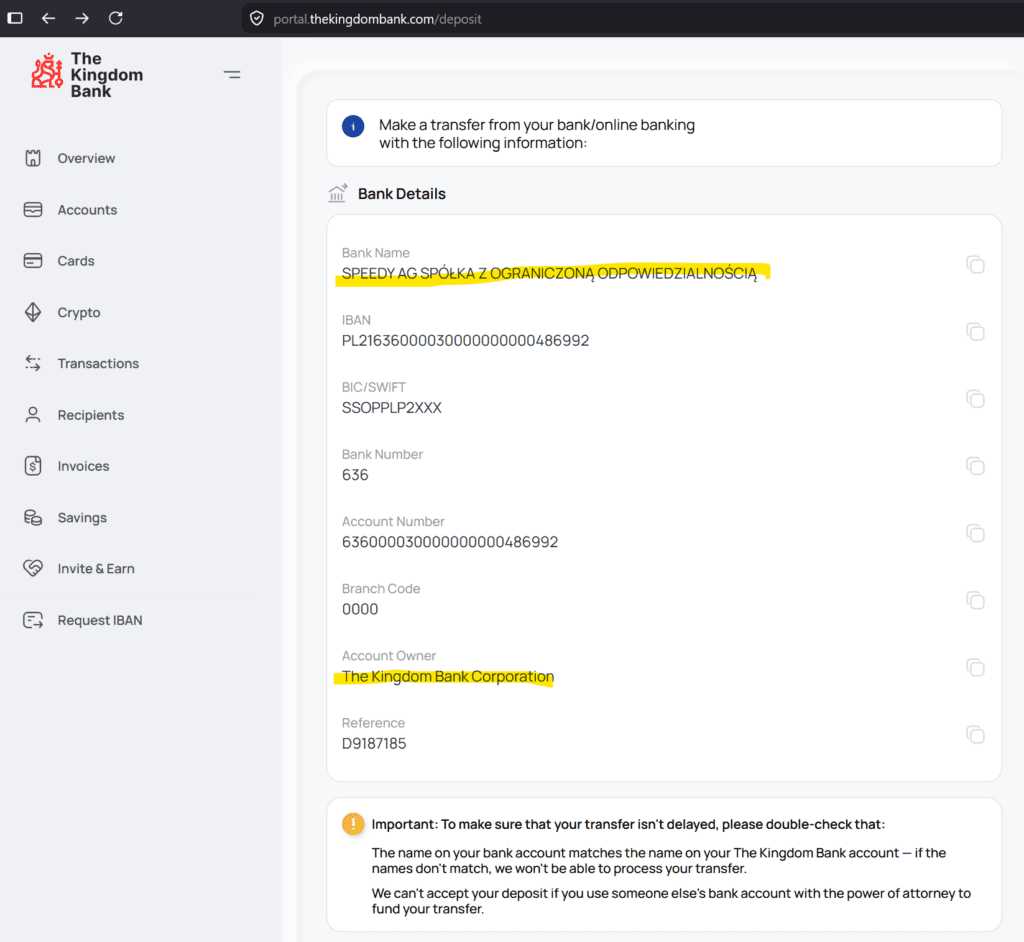

For ordinary bank transfer, The Kingdom Bank generated Polish account details showing Speedy AG sp. z o.o. as the bank / payment institution and The Kingdom Bank Corporation as account owner. The IBAN shown in the test flow was:

PL21636000030000000000486992

BIC/SWIFT: SSOPPLP2XXX

Account Owner: The Kingdom Bank Corporation

Reference: D9187185

This finding is significant. The Kingdom Bank is not an EU-licensed bank. Yet its customer-funding flow appears to rely on an EU-based Polish payment institution account infrastructure through Speedy AG sp. z o.o. Public Polish and business-register data indicate that Speedy is connected to Nebil Serkan Zubari, the founder / key person behind The Kingdom Bank.

This creates a relevant intra-network payment-rail question: an offshore Dominica “bank” appears to access EU payment infrastructure through a Polish payment institution linked to the same principal.

Rail Atlas Snapshot

| Field | Finding |

|---|---|

| Entity | The Kingdom Bank Corporation |

| Domain | https://www.thekingdombank.com |

| Jurisdiction | Dominica |

| EU Licence Status | No EU banking licence identified |

| EU Access Finding | Onboarding possible from Austria and Italy |

| KYC Layer | verify.kyxplatform.com / Plato |

| Deposit Gateway | Banky (pay.banky.io) for instant bank transfer |

| EU Payment Rail | Speedy AG sp. z o.o., Poland (Speedy.io) |

| Observed IBAN | PL21636000030000000000486992 |

| Observed BIC | SSOPPLP2XXX |

| Account Owner | The Kingdom Bank Corporation |

| Risk Verticals | Forex, Gambling, iGaming, crypto |

| Key Risk | Offshore bank using EU payment rails for customer deposits |

| Confidence Grade | Confirmed / Corroborated / Indicated |

| Status | Active Rail Atlas Monitoring Case |

Why This Case Matters

The Kingdom Bank should not be analysed as a conventional EU or UK commercial bank. It presents itself as a licensed international bank in the Commonwealth of Dominica and markets digital banking, global payments, digital assets, crypto-friendly services, FX and payment solutions to international clients.

From a Rail Atlas perspective, the case matters because The Kingdom Bank combines several compliance-sensitive layers:

- offshore/international banking framework;

- digital-asset-friendly positioning;

- public service offering to Forex, Gambling and iGaming;

- customer onboarding from EU residents;

- outsourced KYC / identity verification;

- instant account-to-account payment gateway flow;

- crypto and Binance Pay funding options;

- bank-transfer funding via an EU payment institution;

- apparent linkage between the offshore bank principal and the EU payment institution used for deposits.

This combination creates a high-risk compliance profile requiring enhanced scrutiny by regulators, correspondent banks, payment networks, AML teams and consumer-protection authorities.

Public iGaming And Gambling Positioning

The Kingdom Bank publicly markets Global Payment Solutions for sectors including Forex and Gambling and lists iGaming as an industry served. This is not merely third-party speculation. It is The Kingdom Bank’s own public-facing positioning.

FinTelegram has not yet identified a confirmed casino merchant list or a public casino-domain disclosure stating that a specific casino brand uses The Kingdom Bank as banking, settlement or payment partner. However, the bank’s own market positioning makes iGaming and gambling a legitimate compliance focus.

In high-risk gambling payments, the banking and settlement layer often remains behind the visible cashier, payment gateway, affiliate, crypto or payment-intermediary interface. The absence of public merchant names therefore does not eliminate risk. It only means that transaction-level evidence is required before naming specific operators.

FinTelegram Test: Registration From Austria And Italy

FinTelegram was able to register with The Kingdom Bank as a resident of Austria, Germany and Italy. This is important because The Kingdom Bank is not an EU-licensed bank in the conventional sense. It appears to operate globally on the basis of its offshore/international banking licence from Dominica while allowing EU residents to enter the onboarding process.

The compliance issue is not whether offshore financial institutions may ever serve international clients. The issue is whether EU residents are being onboarded into a banking/payment ecosystem without the customer receiving a clear, prominent explanation of the regulatory perimeter: Dominica supervision, no EU deposit protection, no EU banking licence, and the involvement of EU payment institutions as operational rails.

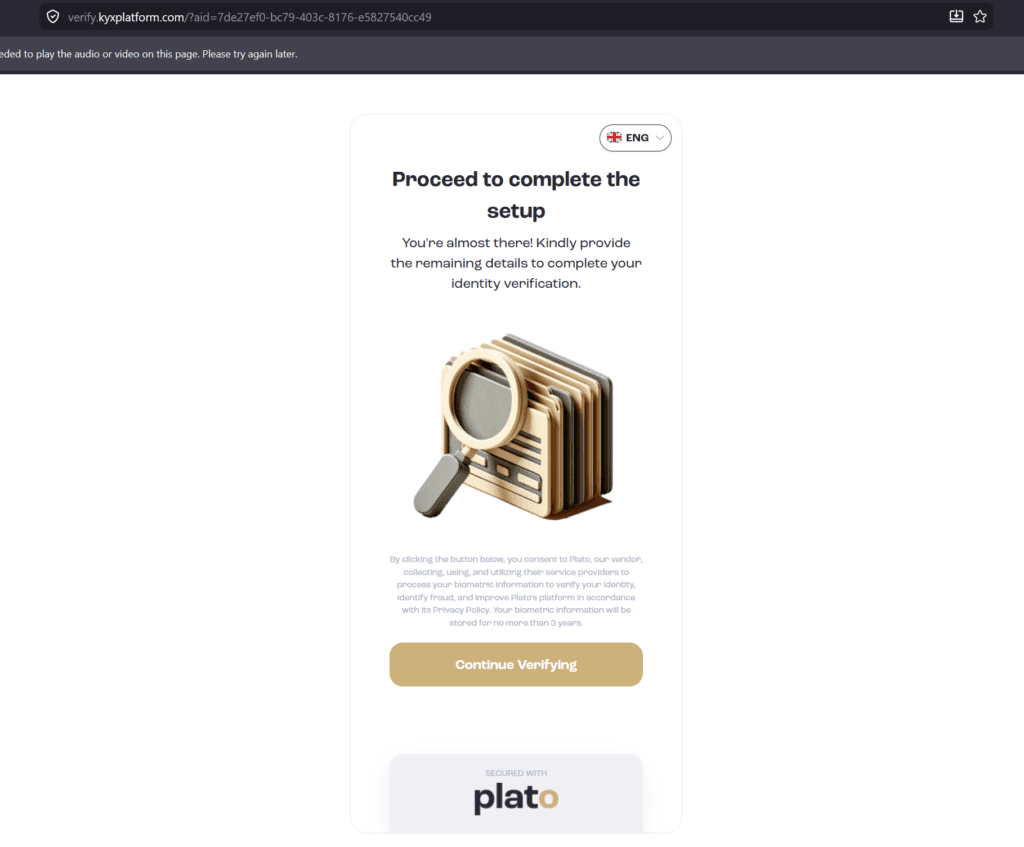

KYC Flow: verify.kyxplatform.com / Plato

The KYC process observed by FinTelegram was conducted through verify.kyxplatform.com, branded as Plato. By clicking the verification button, the user consents to Plato, described as a vendor, collecting and using third-party service providers to process biometric information for identity verification, fraud detection and platform improvement. The screen also states that biometric information will be stored for no more than three years.

Open-source research indicates that the KYXPlatform domain is connected to Plato-branded KYC verification. Plato / Goodfintech publicly describes its services as KYC, KYB, KYT, ID verification, liveness checks, facial expression analysis, sanctions and AML checks, risk scoring and automated KYC flows. Good Fintech Limited appears in UK Companies House as an active private limited company.

A further red flag concerns the user-facing legal disclosure of the KYC provider. The Kingdom Bank onboarding flow redirects users to verify.kyxplatform.com, branded as Plato. Plato is presented under the GoodFintech ecosystem and offers KYC, KYB, KYT, ID verification, liveness checks, facial-expression analysis, sanctions and AML checks. However, FinTelegram’s review of the GoodFintech and Plato web presence found that the reviewed user-facing pages do not clearly and prominently identify the legal entity operating the platform or accepting responsibility for the processing of identity and biometric data.

Open-source corporate records indicate the existence of Good Fintech Limited, a UK company incorporated in October 2023, with the Turkish national Nuri Ozlu listed as director and controlling person.

In the context of EU residents onboarding with an offshore Dominica banking platform, this lack of prominent legal-entity, controller/processor and data-protection disclosure is a material compliance concern. Users asked to submit identity documents and biometric information should not have to conduct external corporate-register research to determine who operates the verification platform and who is responsible for their sensitive personal data.

This raises several compliance questions:

- Who is the contractual KYC processor for The Kingdom Bank: Plato, Goodfintech or another operator behind KYXPlatform?

- Where exactly are biometric data and identity documents stored?

- Which entity is the data controller and which entity is the processor?

- Are EU residents provided with GDPR-compliant disclosures before biometric data collection?

- Are customers clearly told that they are onboarding with an offshore Dominica bank rather than an EU bank?

- How are PEP, sanctions, adverse media and source-of-funds checks calibrated for high-risk sectors such as crypto, Forex and gambling?

The use of external KYC vendors is not unusual. However, in this case, the combination of offshore banking, EU customers, biometric processing, crypto funding and high-risk merchant positioning requires a much higher standard of transparency.

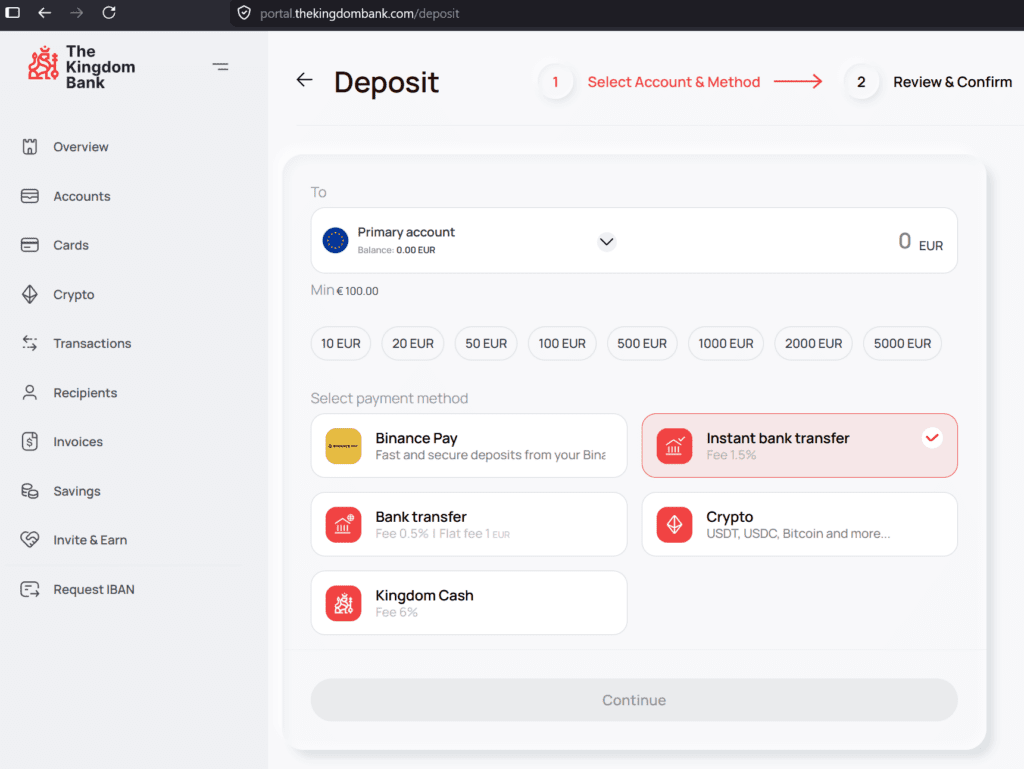

Deposit Options: Binance Pay, Bank Transfer, Instant Bank Transfer, Crypto And Kingdom Cash

Inside the portal, FinTelegram observed the following deposit methods:

- Binance Pay;

- Instant Bank Transfer;

- Bank Transfer;

- Crypto;

- Kingdom Cash.

This funding menu is revealing. It indicates that The Kingdom Bank is not merely presenting itself as a traditional offshore bank account provider. It operates more like a digital banking/payment platform integrating crypto, account-to-account payments and alternative deposit methods.

From an AML perspective, the coexistence of fiat bank transfers, instant payments, crypto and Binance Pay increases the importance of transaction monitoring, source-of-funds review, sanctions screening, wallet risk analytics and real-time fraud controls.

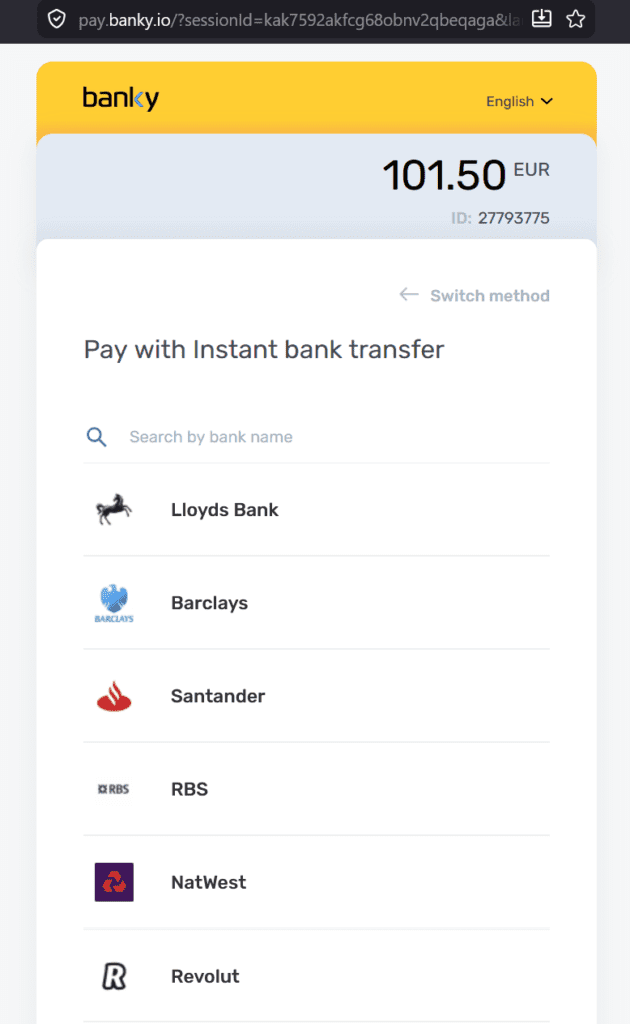

Banky Instant Bank Transfer Flow

For the Instant Bank Transfer option, The Kingdom Bank redirected to pay.banky.io, a Banky-branded gateway. The Banky screen showed a payment amount of EUR 101.50 and allowed the customer to choose from a list of banks. The list included major UK and fintech banks such as Lloyds Bank, Barclays, Santander, RBS, NatWest, Revolut, HSBC, Monzo, Nationwide, Starling Bank, TSB, Bank of Scotland, Ulster Bank, First Direct, Halifax, Danske Bank, Wise, Allied Irish Banks and Bank of Ireland.

In FinTelegram’s review, the instant bank transfer could not be completed and returned the error message:

“Cannot execute payment at this time.”

The failed transaction does not by itself prove misconduct. However, the flow is relevant because it shows that The Kingdom Bank’s deposit infrastructure appears to connect to open-banking-style account-to-account payment rails. This is the type of infrastructure frequently observed in modern high-risk payment ecosystems because it can bypass card-chargeback rails and move customer funds directly from bank accounts.

For Rail Atlas purposes, Banky should be treated as a relevant payment gateway layer in The Kingdom Bank deposit stack.

Ordinary Bank Transfer: Polish Speedy AG Rail

The most important operational finding is the ordinary bank-transfer deposit instruction. The Kingdom Bank portal instructed the user to make a transfer to bank details showing:

Bank Name: Speedy AG spółka z ograniczoną odpowiedzialnością

Domain: Banky.io

IBAN: PL21636000030000000000486992

BIC/SWIFT: SSOPPLP2XXX

Bank Number: 636

Account Number: 636000030000000000486992

Account Owner: The Kingdom Bank Corporation

Reference: D9187185

This means that, in the tested deposit flow, the EU-side funding account was not shown as a direct The Kingdom Bank account at a traditional EU bank. Instead, it was a Polish Speedy AG payment-institution rail where the account owner was The Kingdom Bank Corporation.

Speedy AG sp. z o.o. is a Polish payment institution. Polish regulator KNF granted Speedy AG a national payment institution licence in August 2024. Public sources identify its BIC/SWIFT as SSOPPLP2XXX.

This finding gives The Kingdom Bank an EU payment-rail footprint. It also creates a clear regulatory question: how is a Dominica offshore bank using a Polish payment institution account to receive customer deposits from EU residents?

The Speedy / Zubari Connection

The Speedy finding is particularly sensitive because public Polish register and business data indicate that Nebil Serkan Zubari (LinkedIn) is connected to Speedy AG sp. z o.o. as a board / representative figure and beneficial owner through Speedy Group Holding Limited. Zubari is also the key person behind The Kingdom Bank.

Public sources identify Zubari as the founder and CEO of The Kingdom Bank. The bank’s own blog states that Zubari is the founder and current CEO, while an English court decision in The Kingdom Bank Corporation v Moorwand Ltd identifies Zubari as a director of The Kingdom Bank. West Ham United’s official partnership communication also refers to him as founder of The Kingdom Bank.

This creates an important network-level compliance issue. The flow observed by FinTelegram suggests that The Kingdom Bank customer funds may be routed through a Polish payment institution connected to the same principal behind the offshore bank. This does not automatically mean the structure is illegal. It may be presented as an internal group or partner infrastructure. But from a compliance perspective, it requires transparency:

- Is Speedy acting as payment institution, account provider, correspondent partner or technical payment rail for The Kingdom Bank?

- Does KNF know that Speedy accounts are used for The Kingdom Bank customer deposits?

- Are The Kingdom Bank customers informed that their funds are received through a Polish payment institution?

- Is Speedy conducting independent AML monitoring on the underlying The Kingdom Bank customer and transaction risk?

- Does Speedy classify The Kingdom Bank as a high-risk offshore banking client?

- Are gambling, crypto or iGaming-related funds processed through the same infrastructure?

- Are EU customers protected by any EU safeguards, or are they merely sending money to an offshore bank via an EU payment institution?

These are central Rail Atlas questions.

The Kingdom Bank is not an isolated Dominica offshore bank. It appears to sit within a broader Zubari-linked financial infrastructure that also includes Speedy-branded EU/UK payment entities. One of these nodes, Financial House Limited, is FCA-authorised but currently subject to FCA supervisory restrictions. That significantly strengthens the Rail Atlas risk profile.

Regulatory Perimeter Issue

The Kingdom Bank appears to offer onboarding and deposit functionality to EU residents while operating under a Dominica offshore/international banking licence. FinTelegram has not identified evidence that The Kingdom Bank itself holds an EU banking licence.

The observed Polish deposit rail through Speedy AG does not transform The Kingdom Bank into an EU bank. It may only show that The Kingdom Bank has access to EU payment infrastructure through a regulated Polish payment institution.

This distinction is critical. A consumer in Austria, Italy or another EU country may see an EU IBAN and assume a familiar EU banking environment. However, the account owner remains The Kingdom Bank Corporation, a Dominica offshore entity. The regulatory protection, complaints route and prudential supervision may therefore be very different from those of a conventional EU bank.

Pooled Accounts And Merchant Payment Opacity

The Kingdom Bank publicly promotes pooled-account functionality. In legitimate financial operations, pooled or omnibus accounts may be used to manage client funds efficiently. In high-risk environments, however, they can create transparency problems.

If an offshore bank or payment platform serves gambling, crypto, Forex or high-risk merchant clients through pooled or omnibus-style structures, the visible payee may not clearly reveal the underlying merchant, casino operator, affiliate, crypto broker or beneficiary.

This is one of the central Rail Atlas concerns: in modern payment ecosystems, the entity visible to the customer or the sending bank may be a processor, pooled account, payment institution or banking wrapper rather than the true commercial counterparty.

Compliance Red Flags

| Risk Area | FinTelegram Finding | Compliance Relevance |

|---|---|---|

| Offshore banking | The Kingdom Bank operates from Dominica under an international/offshore banking profile | No conventional EU banking licence identified |

| EU onboarding | Registration possible from Austria and Italy | EU residents appear able to enter the customer funnel |

| KYC / Plato / GoodFintech | Verification through verify.kyxplatform.com / Plato. User-facing pages reviewed by FinTelegram do not clearly disclose the legal operator; external records point to Good Fintech Limited in the UK | Biometric-data, GDPR and data-controller transparency questions. GDPR, biometric-data, controller/processor and contractual transparency concern |

| Crypto funding | Deposit menu includes Crypto and Binance Pay | Requires wallet-risk, sanctions, source-of-funds and Travel Rule controls |

| Instant bank transfer | Deposit flow redirects to pay.banky.io | Open-banking/account-to-account rail relevant for card-chargeback bypass risk |

| Failed test payment | Instant transfer returned “Cannot execute payment at this time” | Operational reliability and gateway availability question |

| EU bank-transfer rail | Deposit instruction uses Speedy AG sp. z o.o. in Poland | Offshore bank appears to receive EU deposits through Polish payment institution |

| Account owner | Account owner shown as The Kingdom Bank Corporation | EU payment rail used for offshore bank funding |

| Nebil Serkan Zubari | Active director of Speedy, Financial House Limited, and The Kingdom Bank | Links The Kingdom Bank principal to UK EMI infrastructure |

| Speedy connection | Public data links Speedy to Nebil Serkan Zubari | Network-level conflict / related-party rail question |

| iGaming positioning | The Kingdom Bank publicly targets Forex, Gambling and iGaming | High-risk merchant vertical explicitly part of target market |

| Pooled accounts | The Kingdom Bank promotes pooled-account structures | Underlying merchant / beneficiary transparency risk |

| Referral / merchant acquisition | Whistleblower material indicates external client-introduction structures | Incentives to source higher-risk merchants require enhanced controls |

Rail Map

A simplified Rail Atlas model based on the review findings is:

EU Resident / Customer

→ The Kingdom Bank Online Portal

→ KYC via KYXPlatform / Plato

→ Deposit Method Selection

→ Banky Instant Bank Transfer / Crypto / Binance Pay / Ordinary Bank Transfer

→ Speedy AG Polish Payment Rail

→ Account Owner: The Kingdom Bank Corporation

→ Offshore Dominica Banking / Payment Platform

For merchant flows, the potential model is:

High-Risk Merchant / iGaming / Forex / Crypto Client

→ External introducer or referral partner

→ The Kingdom Bank onboarding and payment stack

→ Pooled account / IBAN / SWIFT / Crypto / A2A payment layer

→ Customer deposits, merchant settlement or cross-border payouts

The second model remains a working Rail Atlas hypothesis requiring transaction-level confirmation for specific merchants.

FinTelegram Assessment

The extended review significantly strengthens the Rail Atlas case on The Kingdom Bank.

The issue is no longer only that The Kingdom Bank publicly positions itself toward Forex, Gambling and iGaming. The operational review shows that EU residents can enter the onboarding funnel, pass into a KYC process handled through an external KYXPlatform / Plato domain, and receive deposit instructions involving a Polish payment institution.

The Speedy AG connection is the most important new element. A Dominica offshore bank appears to use an EU payment institution rail in Poland for customer deposits, while public register data indicates that the same key person behind The Kingdom Bank is also connected to Speedy.

This does not prove unlawful conduct. But it creates a high-risk related-party payment infrastructure that deserves regulatory and journalistic scrutiny.

For consumers, the risk is transparency. The presence of a Polish IBAN or EU payment institution does not mean the customer is banking with an EU bank. The customer relationship remains with The Kingdom Bank Corporation, a Dominica offshore entity.

For regulators, the risk is perimeter arbitrage. Offshore banking, EU payment institutions, crypto funding, open-banking gateways, pooled accounts and high-risk merchant sectors may combine into a payment architecture that is technically distributed and difficult to supervise end-to-end.

Call For Information

FinTelegram invites whistleblowers, former employees, compliance officers, payment agents, PSP insiders, casino operators, affiliates, customers, regulators and banking partners to provide information about The Kingdom Bank, Speedy AG, Banky, KYXPlatform / Plato, and related payment flows. We are particularly interested in:

- The Kingdom Bank onboarding documents for EU residents;

- deposit screenshots showing Speedy AG, Banky, Binance Pay, crypto or other payment methods;

- account statements showing transfers to or from The Kingdom Bank via Speedy AG;

- contracts or service agreements between The Kingdom Bank and Speedy AG;

- information about the operator and data-controller structure behind KYXPlatform / Plato;

- complaints about frozen deposits, failed withdrawals, blocked accounts or unresolved refunds;

- merchant onboarding files involving gambling, iGaming, Forex or crypto clients;

- payment screenshots linking casino or betting platforms to The Kingdom Bank, Speedy, Banky or related infrastructure;

- internal AML, sanctions, KYC, KYB, PEP, adverse-media or transaction-monitoring concerns;

- evidence concerning pooled accounts or omnibus structures used for high-risk merchants.

Whistleblowers may contact FinTelegram via Whistle42. FinTelegram protects sources and distinguishes clearly between documented facts, open-source intelligence, third-party allegations and editorial assessment.

{kind=link}