Excerpt: A New Stablecoin, An Old Shadow

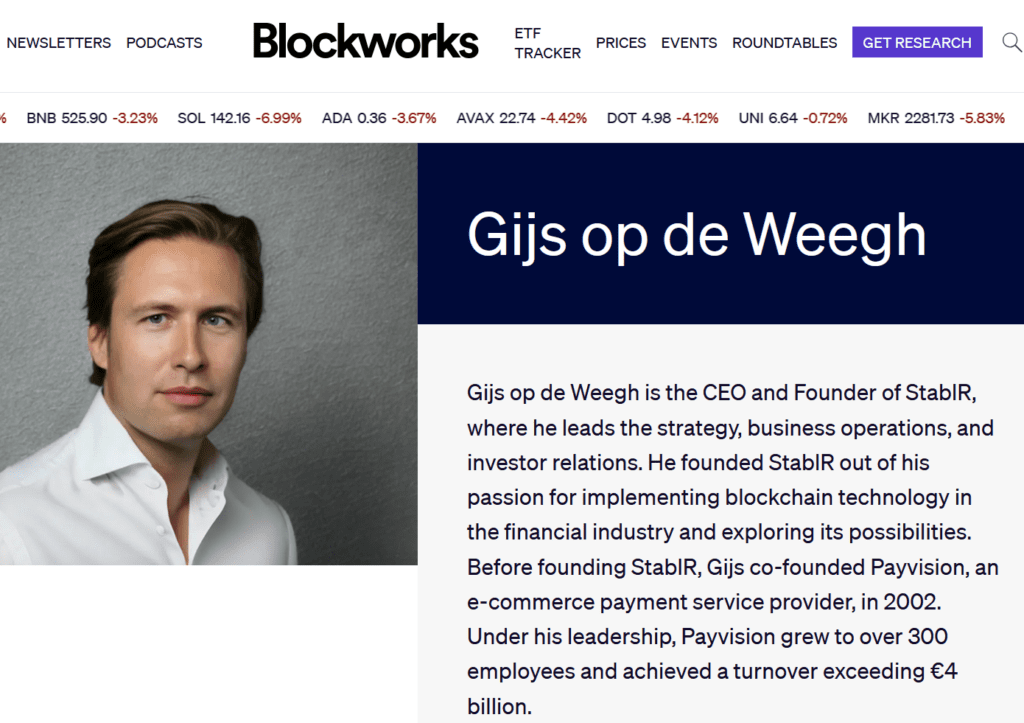

StablR, the Malta-based and MFSA-regulated issuer of EURR and USDR stablecoins, promotes itself as a compliant, euro-denominated digital currency provider under the EU’s new MiCA regime. However, what is missing in its clean-cut public image is the checkered past of its founder and CEO, Gijs op de Weegh, who served as COO of Payvision, a Dutch payment processor infamous for facilitating cybercrime.

Despite damning regulatory findings and a criminal complaint filed by the Dutch central bank (DNB) in 2020, none of this history is disclosed in StablR’s MiCA white paper—an omission that could amount to regulatory misrepresentation and a violation of EU law.

5 Key Points

- StablR is regulated by the Malta Financial Services Authority (MFSA) and issues EURR and USDR stablecoins under MiCA.

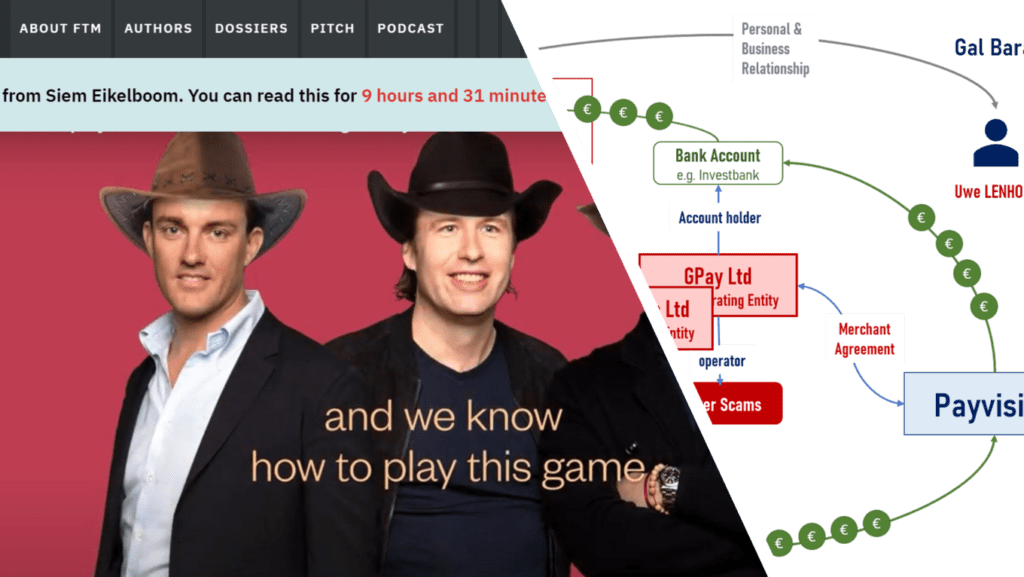

- Gijs op de Weegh (LinkedIn), StablR’s founder and CEO, was COO of Payvision, which laundered funds for major cybercrime networks like those of Uwe Lenhoff and Gal Barak.

- In 2020, the Dutch Central Bank (DNB) filed a criminal complaint against Payvision and its board members for money laundering.

- While Op de Weegh was not convicted, crimanal court documents name him as responsible for onboarding cybercriminal clients as COO.

- The StablR white paper makes no mention of this past—raising serious ethical and regulatory questions under MiCA’s full disclosure requirements. Payvision is not mentioned once in the white paper although several StablR key people have Payvision legacy.

Short Narrative: The Silent Legacy of Cybercrime

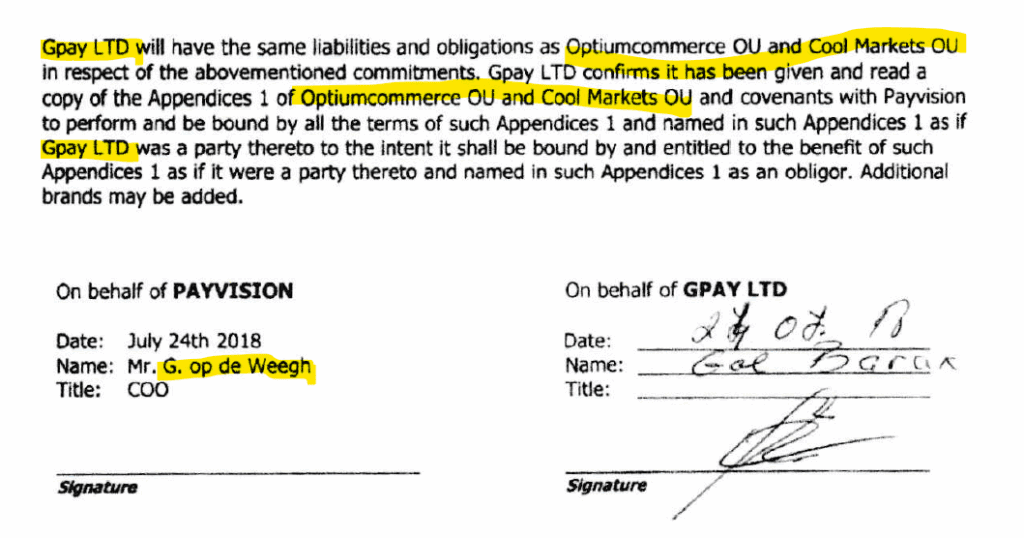

Payvision, a mediocre Dutch fintech, gained notoriety for providing payment services to some of Europe’s most damaging cybercrime organizations. As COO, Gijs op de Weegh played a pivotal operational role—he oversaw onboarding, risk management, and client relations at the time when Payvision processed payments for boiler room scams and binary options frauds. In the criminal files, you find his name on the application forms and agreements with cybercrime organizations and entities, including Barak’s GPay Ltd (screenshot above).

Among Payvision’s most prominent criminal clients were Uwe Lenhoff and Gal Barak, both of whom ran massive scams that defrauded thousands of European investors. After an investigation by DNB, Payvision’s board was charged with facilitating money laundering. Though Op de Weegh escaped conviction, internal records referenced in court filings confirm that he personally handled onboarding these criminal enterprises.

Now, Op de Weegh has re-emerged in Malta with StablR, presenting a white paper that promises full transparency and compliance under MiCA—but fails to disclose his involvement with Payvision’s criminal history.

Extended Analysis: Legal and Regulatory Risk under MiCA

Under the Markets in Crypto-Assets (MiCA) Regulation, stablecoin issuers (asset-referenced tokens and e-money tokens) must meet enhanced transparency standards, especially in their white papers. Article 5 and Article 6 of MiCA emphasize the obligation to provide:

“All information necessary for potential holders of the crypto-asset to make an informed decision… including risks, governance, and the track record of the issuer’s management.”

Failure to disclose material facts—including past regulatory investigations or legal involvement of executives—could constitute a “material omission” and violate MiCA’s Article 14 on false or misleading information.

Moreover, Recital 38 of MiCA stresses that issuers whose activities may be systemically relevant must be held to heightened scrutiny due to potential financial stability risks. This is directly relevant for stablecoin issuers like StablR, which position themselves as infrastructure providers for Europe’s crypto-finance future.

If the MFSA and the European Securities and Markets Authority (ESMA) take MiCA’s standards seriously, StablR’s white paper may be non-compliant, and enforcement action could be warranted.

Actionable Insight: Due Diligence is Not Optional

- Regulators: The MFSA must urgently review whether StablR‘s white paper complies with MiCA’s full disclosure requirements. A formal review under Article 16 MiCA may be appropriate.

- Partners and Custodians: Counterparties engaging with StablR—particularly custodians, DeFi platforms, and liquidity providers—should demand transparency about its founder’s past.

- Competitors: Euro-denominated stablecoin issuers like Circle (EURC) or Anchorage-backed projects should highlight their compliance edge in contrast to StablR’s opaque origins.

Download StablR white paper here (V3.1).

Recommendation: A Risk Disclosure Audit is Needed

Before any further adoption or promotion of StablR’s EURR and USDR stablecoins, the MFSA should initiate a regulatory audit of the white paper and background checks on all executives. Given MiCA’s emphasis on financial integrity and market trust, the concealment of Payvision’s criminal legacy is a ticking time bomb—one that may backfire on investors, partners, and European financial stability alike.

{kind=link}