FinTelegram’s MiCA Day One test suggests that MEXC not only continued to accept EU users, but operated a multi-layer third-party onboarding and payment-routing model designed to keep fiat access functional despite no disclosed MiCA CASP authorisation.

Key Takeaways

- FinTelegram’s live test on 1 July 2026 shows that a KYC-verified EU user could access MEXC fiat deposit and crypto purchase flows.

- The MEXC deposit process routed the user through multiple third-party layers, including Harmoniie SAS dba OuiTrust / Heuro, Ocean Wave Fintech Pty Ltd, Legend Trading, and Finetix.

- During the MEXC bank-transfer flow, a French IBAN at Heuro / OuiTrust was presented for payment.

- MEXC automatically triggered account creation with Ocean Wave Fintech Pty Ltd, an Australian company whose historical ABN records show earlier names including MXC Tech Pty Ltd and MEXC Australia Pty Ltd.

- Another MEXC flow triggered an account application with Legend Trading.

- A card payment verification screenshot showed the descriptor “Finetix*mexc.com”, strengthening the hypothesis that Finetix acts as a central MEXC-linked EU-facing payment orchestration layer.

- FinTelegram does not currently allege that MEXC, Heuro / OuiTrust, Ocean Wave, Legend Trading and Finetix are under common ownership. The structure requires further whistleblower evidence and regulatory clarification.

- FinTelegram keeps MEXC at Radar Status: Black under its MiCA/MiFID-II Perimeter Radar.

Radar Classification Update

| Field | Updated Assessment |

|---|---|

| Platform | MEXC (www.mexc.com) |

| EU user status | KYC-verified EU resident and national |

| MiCA status | No disclosed MEXC MiCA CASP authorisation identified in the tested flow |

| Fiat access | Bank transfer, card and third-party rails observed |

| Key payment layers | Finetix, OuiTrust / Heuro, Ocean Wave Fintech, Legend Trading |

| Heuro / OuiTrust role | French EMI / IBAN and SEPA rail layer |

| Ocean Wave role | Australian service-provider layer; former names include MEXC Australia Pty Ltd and MXC Tech Pty Ltd |

| Legend role | Third-party crypto/fiat gateway; European contracting entity appears to be Legend Financial Ireland Limited |

| Finetix role | Appears to be central payment orchestration / merchant-descriptor / contractual gateway layer |

| Core risk | Continued EU-facing onboarding and fiat access after MiCA Day One |

| Radar Status | Black |

| Watch Type | Active EU Onboarding Watch / Payment Relay Watch / Jurisdictional Arbitrage Watch / Payment Facilitator Risk Watch |

The Core Finding

FinTelegram’s first MiCA Day One MEXC report showed that MEXC continued to onboard EU users on 1 July 2026. This update goes further.

The newly documented flow suggests that MEXC did not merely leave its platform open to EU users. It appears to have embedded a multi-layer payment relay that routes an EU customer through a chain of third-party service providers while keeping the MEXC trading and deposit experience functionally available. The architecture observed by FinTelegram can be summarised as follows:

EU user → MEXC onboarding → MEXC fiat deposit / buy crypto flow → third-party account creation or consent → Finetix / OuiTrust / Heuro / Ocean Wave / Legend Trading layers → EUR or card payment → crypto or fiat crediting into MEXC environment.

That is not an orderly wind-down pattern. It looks like an operational fiat-onramp stack.

MiCA Day One: Why This Matters

ESMA’s message for 1 July 2026 is clear. Unauthorised CASPs must immediately stop onboarding new EU clients, refrain from opening new client relationships or accounts, cease marketing and solicitation, and limit services to actions necessary to sell, transfer, reallocate or close positions. Custody may continue only for the period strictly necessary to complete an orderly exit. ESMA also reminds non-EU CASPs that they cannot provide MiCA services to EU clients or solicit EU clients, except under the narrow reverse-solicitation regime.

MEXC’s own support materials, however, still describe EUR online bank-transfer deposits as available to verified KYC users from supported countries and list many EU/EEA jurisdictions, including Austria, Belgium, France, Germany, Ireland, Italy, Lithuania, Luxembourg, Malta, Poland, Romania, Spain and others. The same MEXC page states that fiat deposit limits are up to €20,000 per transaction and €200,000 daily. (MEXC)

MEXC’s User Agreement lists several prohibited jurisdictions, including the United States, United Kingdom, Canada, mainland China, Singapore and others, but the reviewed prohibition list does not name the EU or EEA as such. The User Agreement also expressly refers to risks associated with transactions in digital assets and their derivatives. (MEXC)

That is the legal tension: MiCA says no unauthorised EU-facing onboarding; the MEXC ecosystem still appears to deliver fiat and crypto access to EU users.

Evidence Layer 1: The OuiTrust / Heuro Consent Layer

FinTelegram’s MEXC bank-transfer test first presented a consent screen requiring the user to accept terms involving MEXC and Harmoniie SAS, trading as OuiTrust. The same screenshot indicated links to OuiTrust and Finetix legal materials.

OuiTrust’s legal page states that OuiTrust is the trading name of Harmoniie SAS, a French simplified joint stock company registered in Paris, headquartered at 1 Rue de la Bourse, 75002 Paris, and authorised by the French ACPR as an electronic money institution under licence number 17478. (OuiTrust)

TheBanks.eu profile for Heuro SAS, doing business as OuiTrust, states that Heuro is an electronic money institution authorised and regulated by the Banque de France, offering multi-currency IBAN accounts, debit cards, e-money tokens, international transfers, foreign exchange and white-label cards. It also lists BIC HRSAFR22 and clarifies that Heuro is not a bank and does not participate in deposit-guarantee schemes, though it must safeguard customer funds under applicable EMI rules. (thebanks.eu)

Heuro’s own website describes Heuro as a “leading web3 payment service provider in Europe” and states that Heuro SAS is an electronic money institution authorised by the ACPR / Banque de France. It also highlights stablecoin-related liquidity and “100% backed” reserves. (HEURO)

This role is therefore critical. Heuro / OuiTrust may be a legitimate French EMI, but an EMI licence is not a MiCA CASP authorisation for MEXC. The key question is whether a French regulated payment institution is facilitating fiat access to an offshore crypto exchange that has no disclosed MiCA authorisation for EU users.

FinTelegram has previously reported on the MEXC–Heuro–Finetix rail and highlighted Heuro’s strongly international and Asian-linked background. The existing evidence does not prove that Heuro and MEXC are commonly owned or directly affiliated. That question requires whistleblower information, contractual documentation and regulatory clarification. (FinTelegram)

Evidence Layer 2: The Heuro French IBAN

After the consent stage, the MEXC flow generated an order for a €100 bank transfer. The payment screen showed a French IBAN, BIC HRSAFR22XXX, bank name Heuro, and the Paris address corresponding to the OuiTrust / Harmoniie public legal footprint. FinTelegram will not publish the full IBAN or reporter-specific details for privacy and security reasons, but screenshots are on file.

From a compliance perspective, this matters because the user was not merely reading a MEXC article or browsing a landing page. The platform generated a concrete bank-transfer order for an EU resident, in euros, through a French EMI rail, inside the MEXC deposit process.

That is difficult to reconcile with a no-new-EU-business posture.

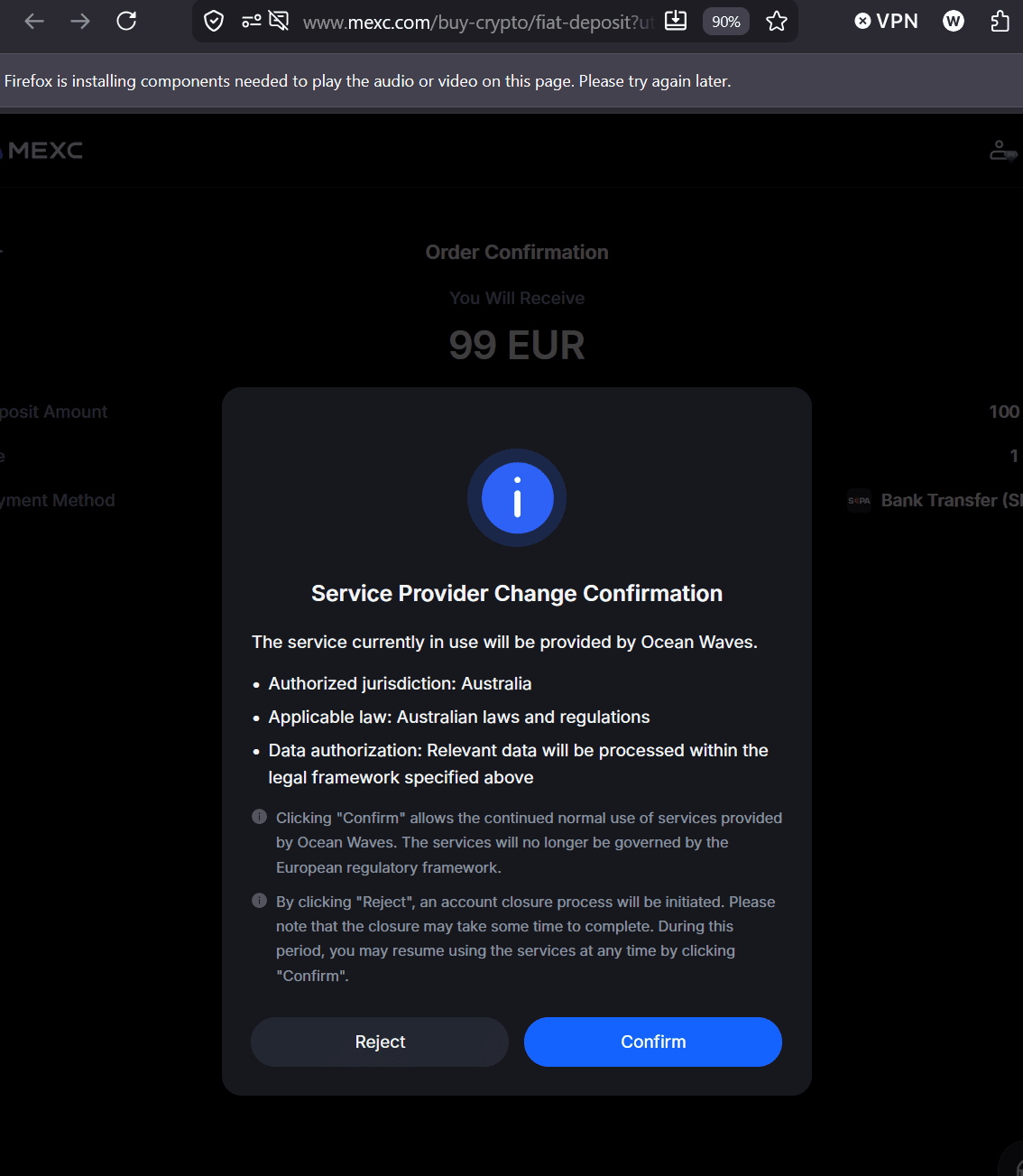

Evidence Layer 3: Ocean Wave Fintech — The MEXC Australia Link

The most striking new element is Ocean Wave Fintech Pty Ltd.

During the MEXC bank-transfer process, a “Service Provider Change Confirmation” appeared, stating that the service currently in use would be provided by “Ocean Waves,” that the authorised jurisdiction would be Australia, that Australian laws and regulations would apply, and that clicking confirm would allow continued normal use of services provided by Ocean Waves. The same screen stated that the services would no longer be governed by the European regulatory framework (Screenshot left).

Shortly thereafter, FinTelegram received emails from Ocean Wave Fintech Pty Ltd confirming account creation and a deposit request.

Public Australian ABN history shows that Ocean Wave Fintech Pty Ltd is not an unrelated new name. The ABN history for ABN 59 638 473 211 shows the current name Ocean Wave Fintech Pty Ltd, preceded by Ocean Waive Fintech Pty Ltd, preceded by MEXC Australia Pty Ltd, preceded by MXC Tech Pty Ltd. The entity is an Australian private company with ASIC ACN 638 473 211. (abr.business.gov.au)

This is a major finding. MEXC appears to have routed a KYC-verified EU user into an Australian service-provider layer whose own corporate history includes the MEXC name.

The compliance question is obvious:

Is Ocean Wave Fintech a genuine independent third-party service provider, or a renamed MEXC-linked entity used to relocate EU customer relationships outside the European regulatory framework?

FinTelegram does not yet answer that question. But the corporate-history link makes the Ocean Wave layer a priority investigation target.

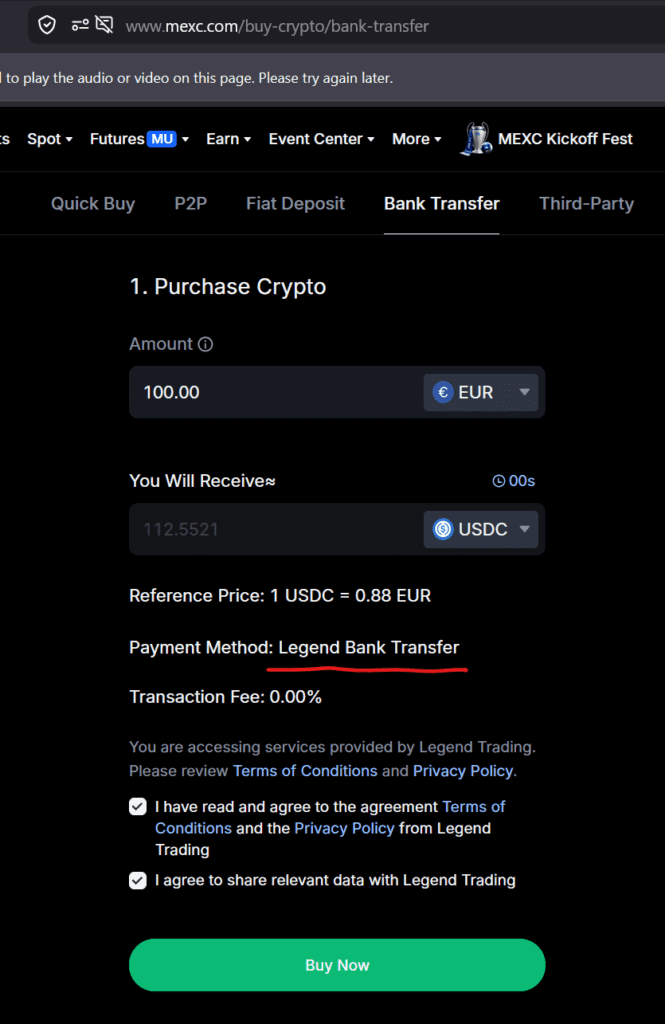

Evidence Layer 4: Legend Trading

FinTelegram also tested the Bank Transfer option under MEXC’s buy-crypto flow and observed “Legend Bank Transfer.” The user was required to accept Legend Trading terms and data sharing, and then received an email titled “MEXC via Legend Trading” concerning an application to a fiat trading account.

Legend Trading’s Terms of Use state that European users contract with Legend Financial Ireland Limited, trading as Legend Trading, while rest-of-world users contract with Legend Trading Inc. in Delaware. (legendtrading.com)

This layer must be handled carefully because Legend Financial Ireland Limited appears to be MiCA-authorised. The AMF white list states that Legend Financial Ireland Limited is licensed under MiCA in Ireland and authorised to provide services in France under freedom of services, with authorised services including exchange of crypto-assets for funds and exchange of crypto-assets for other crypto-assets. (amf-france.org)

Legend itself announced that Legend Financial Ireland Limited had received CASP authorisation from the Central Bank of Ireland and presented Legend FXN as a regulated stablecoin-to-fiat settlement platform for European banks, EMIs, payment institutions and other institutions. (legendtrading.com)

This creates a different, but equally important, issue. If a MiCA-authorised CASP is embedded in a MEXC fiat flow, regulators and compliance officers must ask: What is Legend’s role? Is it merely providing an independent regulated exchange service? Is it onboarding the customer as its own client? Does it transfer value or liquidity into MEXC? Does it know that the platform context is MEXC? What due diligence has it conducted on MEXC’s EU authorisation status?

A MiCA-authorised gateway cannot simply become a regulatory bridge for a non-authorised offshore exchange without raising perimeter, outsourcing, conduct and client-disclosure questions.

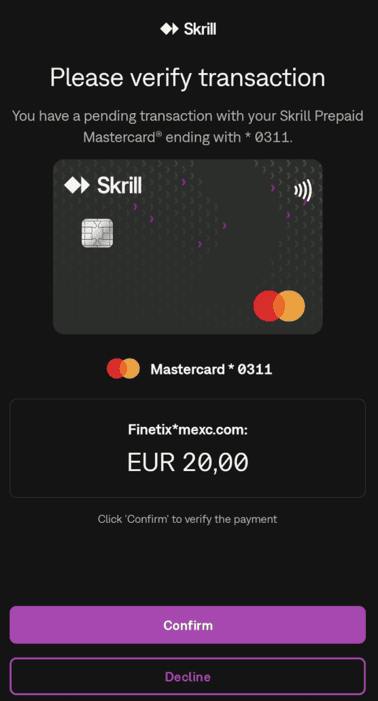

Evidence Layer 5: Finetix Appears As The Connecting Layer

The Finetix evidence has now become stronger. First, Finetix’s own website states that it is a Romania-based crypto exchange offering “secure fiat payment gateway services to customers across European jurisdictions.” (finetix.net)

Second, Finetix’s Terms of Use identify the counterparty as FINETIX LIMITED S.R.L., registered in Bucharest, Romania, with registered number 51736231. The same terms define digital-asset transactions as purchases or sales of digital assets through its services, including crypto-fiat and fiat-crypto transactions. They further state that Finetix provides a platform to buy digital assets using approved fiat currencies or sell digital assets for supported fiat currencies through partnered payment institutions. (finetix.net) (finetix.net)

Third, the Finetix terms state that Finetix acts as principal in each digital-asset transaction, while also relying on partnered payment institutions and third-party providers for wallets and liquidity. (finetix.net)

Fourth, FinTelegram’s screenshots show a card payment verification descriptor “Finetix*mexc.com” during a MEXC crypto purchase attempt.

Taken together, this supports a strong working hypothesis:

Finetix appears to operate as a central EU-facing payment orchestration, merchant-descriptor and settlement bridge for MEXC-related fiat flows.

However, FinTelegram should still avoid the overstatement that Finetix is “the operator of MEXC in the EU” unless additional contractual, corporate or regulatory evidence emerges. The stronger formulation is:

Finetix appears to be a central contractual and payment gateway layer in the MEXC EU fiat stack. Whether Finetix is also the de facto EU operator of MEXC crypto services remains a key question for regulators and whistleblowers.

The Payment Relay Model

Based on FinTelegram’s live test, the MEXC EU fiat flow appears to include at least four operating modes:

| Flow | Observed Layer | Compliance Question |

|---|---|---|

| Online bank transfer | MEXC + OuiTrust / Heuro + Finetix references | Is a French EMI facilitating MEXC fiat inflows for EU users? |

| Service-provider change | Ocean Wave Fintech Pty Ltd | Is MEXC shifting the contractual service relationship to an Australian former MEXC entity? |

| Bank-transfer crypto purchase | Legend Trading | Is a MiCA-authorised Legend entity acting as an on-ramp into MEXC? |

| Card purchase | Finetix*mexc.com descriptor | Is Finetix the merchant/payment facilitator for MEXC card purchases? |

This is the pattern FinTelegram calls the MEXC Payment Relay.

It is not simply outsourcing. It looks like a sequential regulatory relay: MEXC remains the user-facing platform, while specialised third parties appear at different points of the fiat transaction chain.

Regulatory Assessment

The central legal issue is not whether every individual payment provider is regulated somewhere. Heuro may be an EMI. Legend may be MiCA-authorised for specific services. Ocean Wave may be an Australian entity. Finetix may have Romanian corporate status and contractual terms. The question is whether the combined structure enables MEXC to keep serving EU users without MEXC disclosing a MiCA CASP authorisation.

From a MiCA perspective, the problematic pattern is:

- EU resident and national completes MEXC KYC.

- MEXC allows fiat deposit and crypto purchase flows.

- The user is routed through multiple payment and crypto gateways.

- The flow includes a French EMI IBAN, an Australian service-provider switch, a Romanian Finetix layer and an Irish/US Legend gateway.

- No clear MEXC MiCA-authorised EU legal entity is disclosed in the observed customer journey.

- No clear wind-down, restriction or no-new-EU-business warning is presented.

That is why this case is now more than an “offshore exchange access” issue. It is a regulatory-arbitrage and payment-facilitation issue.

FinTelegram Assessment

MEXC appears to have built a post-MiCA regulatory relay for EU users.

The user enters through MEXC, is KYC-approved as an EU resident, sees EUR bank-transfer and card options, is routed through a French EMI rail, pushed toward Australian and Irish third-party account relationships, and exposed to Finetix-linked payment descriptors — while no MiCA-authorised MEXC entity is disclosed.

FinTelegram does not allege, at this stage, that MEXC, Heuro / OuiTrust, Finetix, Ocean Wave and Legend Trading are commonly owned or controlled. Nor does FinTelegram allege that Heuro or Legend have intentionally facilitated regulatory avoidance. The evidence does, however, show that their infrastructure appears in live MEXC fiat flows for an EU user after MiCA Day One.

The key question for regulators is therefore:

Which entity is responsible for ensuring that a KYC-verified EU resident is not onboarded into MEXC’s crypto services after MiCA Day One without a disclosed MiCA CASP authorisation — MEXC, Finetix, OuiTrust / Heuro, Ocean Wave, Legend Trading, or nobody?

Updated Radar Status

FinTelegram updates the MEXC case as follows:

| Field | Status |

|---|---|

| Radar Status | Black |

| Primary Watch Type | Active EU Onboarding Watch |

| Additional Watch Types | Payment Relay Watch / Jurisdictional Arbitrage Watch / Payment Facilitator Risk Watch / Third-Party Onboarding Watch / MiFID-II Derivatives Watch |

| Key Evidence | EU KYC approval, fiat deposit flow, French Heuro IBAN, Ocean Wave automatic account creation, Legend Trading account application, Finetix*mexc.com descriptor |

| Regulatory Focus | MiCA authorisation, payment-facilitator due diligence, reverse solicitation, client disclosures, outsourcing, AML/CFT, data sharing |

Questions To MEXC

FinTelegram invites MEXC and all relevant MEXC-related entities to answer:

- Which legal entity provides MEXC services to EU users after 1 July 2026?

- Does any MEXC entity hold a MiCA CASP authorisation in the EEA?

- If not, why can a KYC-verified EU resident still access fiat deposit and crypto purchase flows?

- What is the contractual relationship between MEXC and Finetix?

- What is the contractual relationship between MEXC and Ocean Wave Fintech Pty Ltd?

- Why does the MEXC flow tell EU users that services will be provided under Australian jurisdiction by Ocean Wave?

- Why does Ocean Wave’s corporate history include MEXC Australia Pty Ltd and MXC Tech Pty Ltd?

- What is the role of OuiTrust / Heuro in MEXC EUR deposits?

- What is the role of Legend Trading in MEXC bank-transfer crypto purchases?

- Does MEXC consider these services reverse-solicited by EU users?

Questions To Finetix

FinTelegram invites Finetix Ltd S.R.L. to answer:

- Is Finetix a contractual partner, payment facilitator, merchant-of-record, liquidity provider or settlement agent for MEXC?

- Why does a card transaction show the descriptor Finetix*mexc.com?

- Does Finetix process fiat inflows for MEXC EU users?

- Has Finetix assessed whether MEXC holds a MiCA CASP authorisation?

- Does Finetix onboard users directly or indirectly through MEXC?

- Which payment institutions does Finetix use for MEXC-related EUR flows?

- Has Finetix notified Romanian or EU regulators of the MEXC relationship?

Questions To Heuro / OuiTrust / Harmoniie SAS

FinTelegram invites Heuro, OuiTrust and Harmoniie SAS to answer:

- Does Heuro / OuiTrust provide IBAN, SEPA, e-money or payment services for MEXC-related flows?

- Is Finetix a client, partner or intermediary of Heuro / OuiTrust?

- Has Heuro / OuiTrust assessed MEXC’s MiCA authorisation status?

- Does Heuro / OuiTrust permit its EMI rails to be used for crypto exchange inflows?

- Does Heuro / OuiTrust consider MEXC-related users to be its customers, Finetix’s customers, MEXC’s customers or someone else’s customers?

- Has Heuro / OuiTrust notified the ACPR or Banque de France of the MEXC-related flow?

- Is there any ownership, funding, management or commercial link between Heuro / OuiTrust and MEXC or MEXC-related entities?

Questions To Ocean Wave Fintech Pty Ltd

FinTelegram invites Ocean Wave Fintech Pty Ltd to answer:

- What is the relationship between Ocean Wave and MEXC?

- Why did Ocean Wave previously operate under the names MEXC Australia Pty Ltd and MXC Tech Pty Ltd?

- Does Ocean Wave provide services to EU users routed through MEXC.com?

- Does Ocean Wave consider EU users to fall outside the European regulatory framework after accepting the service-provider change?

- Is Ocean Wave registered with AUSTRAC for digital currency exchange services?

- Does Ocean Wave conduct its own KYC, AML and sanctions screening, or rely on MEXC?

- Does Ocean Wave hold or control customer fiat or crypto assets?

- What happens if a user rejects the service-provider change?

Questions To Legend Trading

FinTelegram invites Legend Trading and Legend Financial Ireland Limited to answer:

- Does Legend provide services to MEXC users through embedded MEXC flows?

- Is MEXC an authorised partner or third-party platform of Legend?

- Does Legend onboard EU users directly when they initiate a MEXC bank-transfer crypto purchase?

- Does Legend transfer crypto or fiat liquidity into MEXC wallets or accounts?

- Has Legend assessed whether MEXC is MiCA-authorised?

- Does Legend consider its MiCA authorisation to cover transactions initiated through MEXC?

- Does Legend report MEXC-related activity to the Central Bank of Ireland or other competent authorities?

Right Of Reply

FinTelegram invites MEXC, MX Global Ltd, MEXC Trading Platform, Finetix Ltd S.R.L., Harmoniie SAS / OuiTrust / Heuro, Ocean Wave Fintech Pty Ltd, Legend Trading, Legend Financial Ireland Limited, Skrill / Paysafe and all relevant payment facilitators, banking partners and legal representatives to provide a factual statement on the MEXC EU fiat deposit and crypto purchase flow, MiCA status, contractual relationships, customer onboarding, payment routing, data sharing, AML/CFT controls and client-asset protection arrangements.

Call For Information

FinTelegram invites whistleblowers, former employees, compliance officers, payment professionals, EMI staff, banking partners, regulators, developers, customer-support agents, acquirers, PSPs and users with information about MEXC, Finetix, OuiTrust / Heuro, Ocean Wave Fintech, Legend Trading, Skrill / Paysafe, EU fiat rails, MiCA onboarding or payment-routing arrangements to contact FinTelegram via Whistle42.

{kind=link}