Nexo markets itself as a premier digital-asset wealth platform, but its licensing posture in Europe appears materially narrower than its branding suggests. A review of Nexo’s public positioning, entity footprint, product stack, and prior regulatory actions indicates a business model that sits at the intersection of crypto-asset services, lending, and investment-like products, with MiCA likely to force sharper legal boundaries in the EU.

- Nexo operates a broad crypto platform spanning exchange, custody, crypto-backed lending, OTC, and interest-bearing products, while publicly presenting itself as a “wealth platform” for digital assets.

- The group appears to rely on a mix of offshore and European entities, including Nexo Capital Inc. in the Cayman Islands, while using EU VASP registrations as the visible regulatory basis for parts of its European activity.

- Italy’s VASP registration regime supports AML-supervised crypto services, but it does not by itself authorize traditional wealth management, portfolio management, or broad banking-style activity.

- Nexo’s interest and yield products represent the clearest compliance pressure point, as past enforcement in the United States shows that such products can be treated as unregistered securities or analogous regulated products.

- Nexo’s MiCA messaging suggests strategic adaptation to the new EU framework, but available public materials do not show that the group already holds a full MiCA CASP authorization.

- Corporate onboarding practices may rely on aggressive, OSINT-influenced risk assumptions, raising questions around proportionality, relevance, and data minimization in KYB/KYC reviews.

The Nexo Narrative and the Regulatory Reality

Nexo’s public-facing narrative is straightforward: the company presents itself as a one-stop digital wealth platform where clients can buy, trade, borrow, and earn on crypto assets. That framing is commercially effective, but from a compliance perspective it blurs a critical distinction between regulated crypto-asset services and classical financial services such as portfolio management, investment advice, or deposit-taking.

This distinction matters because the legal foundation visible in Europe is not a conventional investment-firm or banking licence. Instead, Nexo points to VASP registrations in several EU jurisdictions and to its ongoing MiCA alignment, which is a materially narrower basis than the expression “wealth platform” may imply to retail and corporate clients.

Nexo at a Glance

| Category | Information |

|---|---|

| Brand | Nexo, marketed as a digital-assets or crypto-wealth platform. |

| Primary domain | nexo.com, including localized variants such as /en-us. |

| Other domain/site | Nexo Markets https://nexo-markets.com/ |

| Core visible legal entities | Nexo Capital Inc.; Nexo Inc.; Nexo Financial LLC; additional Nexo group entities organized primarily in European jurisdictions according to enforcement records. |

| Publicly visible offshore anchor | Nexo Capital Inc., Cayman Islands, appears repeatedly in app-store disclosures and enforcement materials. Nexo Markets Ltd, Seychelles (Securities Dealer license) |

| Key jurisdictions | Cayman Islands, Seychelles, Switzerland, Italy, Poland, and other European jurisdictions; U.S. footprint appears in enforcement and licensing-related disclosures. |

| Product scope | Spot trading, swaps, custody, crypto-backed credit lines, Earn/yield products, OTC services, corporate accounts, and payment-card-related offerings. |

| Founders / key figures | Antoni Trenchev, Kosta Kantchev/Kanchev, Kalin Metodiev; Georgi Shulev appears in historical founder-related reporting and litigation context. |

| Ownership / control | Privately held group with no fully transparent public UBO picture on the website; public materials point to concentrated founder influence. |

| EU regulatory framing | VASP registrations in multiple member states and MiCA transition messaging. |

| Key regulatory pressure points | Earn products, lending representations, cross-border marketing, entity transparency, and MiCA transition readiness. |

Entity Structure, Key Persons, and Beneficial Ownership Questions

Nexo is a privately held group and does not provide a transparent, consolidated UBO map on its public-facing website. What is visible through public records and enforcement materials is a recurring set of core entities and individuals, above all Nexo Capital Inc. and the founding circle around Antoni Trenchev, Kosta Kantchev, and Kalin Metodiev.

This matters from a compliance standpoint for two reasons. First, a fragmented multi-jurisdiction structure can complicate customer understanding of the actual contracting entity, client-asset exposure, and recourse options. Second, concentrated founder control combined with cross-border structuring raises recurring questions around governance, transparency, and intra-group risk allocation that should be central to any institutional due-diligence review.

Key Persons and Apparent Control Cluster

| Person | Apparent Role | Compliance Relevance |

|---|---|---|

| Antoni Trenchev (LinkedIn) | Co-founder and public-facing senior executive; frequently associated with Nexo in public reporting. | Central control person, reputational anchor, and likely key individual for governance review. |

| Kosta Kantchev / Kanchev (LinkedIn) | Co-founder, Executive Chairman, and core control figure in founder-related reporting. | Likely central to beneficial ownership and strategic control assessment. |

| Kalin Metodiev (LinkedIn) | Co-founder and recurring key executive figure in reporting and proceedings. | Material for governance mapping and historic decision-making review. |

| Georgi Shulev (LinkednIn) | Historical co-founder figure referenced in reporting and litigation context. Managing Partner until 2019 | Relevant to early ownership history and internal disputes over assets/control. |

| Trayan Nikolov (LinkedIn) | Named in reporting around Bulgarian proceedings involving Nexo-linked individuals. | Relevant to expanded key-person screening and contextual risk review. |

| Peter Serdev (LinkedIn) | Contact person Nexo Markets | Nexo Markets is registered as a security dealer in the Seychelles |

Europe: VASP Registrations vs. Actual Licensing Reality

Nexo’s European licensing narrative is difficult to verify from its own public materials. The group has publicly claimed since 2022 that it secured VASP registration in Italy and later stated that it holds VASP registrations in several EU member states as part of its preparation for MiCA. Yet the latest available OAM list in Italy does not show any Nexo-branded or obviously Nexo-controlled entity among the registered virtual asset operators. This discrepancy alone would warrant caution. Taken together with the group’s own website disclosures, it raises a broader transparency problem around Nexo’s actual regulatory footing in the EEA.

First, Nexo’s public-facing website does not provide a clear, consolidated, and current overview of which legal entities are licensed or registered in which jurisdictions, and for which products. The site relies heavily on broad trust and safety messaging, including references to “proven regulatory compliance”, technology partners, audits, and security infrastructure, while omitting the kind of entity-by-entity licensing map that customers would normally expect from a serious cross-border financial services provider. Even on the US-facing site, the footer points to Bakkt disclosures without clearly explaining which Nexo products or entities are covered by which regulated framework.

Second, Nexo’s EEA Terms of Service do not identify a specific contracting entity. Instead of naming a particular legal person with its registered office, registration number, and competent supervisor, the terms define “Nexo” in broad group language as any holding company, subsidiary, or entity belonging to the Nexo group of companies. From a compliance perspective, that is highly problematic. It leaves EEA clients without clear visibility on who the actual counterparty is, which entity bears liability, and which supervisory framework, if any, governs the relevant service relationship.

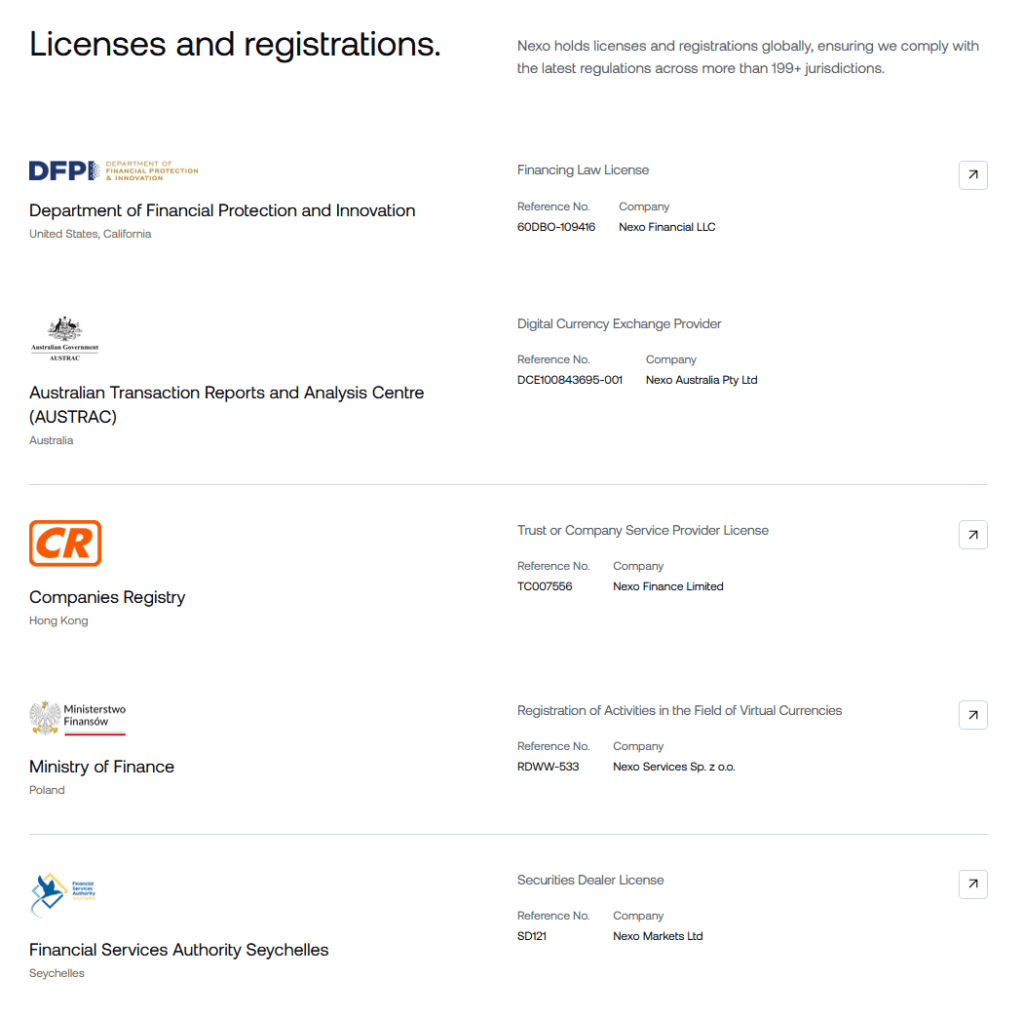

Third, the licensing picture only becomes marginally clearer through a separate Security page that is not the obvious first stop for clients seeking legal or regulatory transparency. There, Nexo lists selected licences and registrations in California, Australia, Hong Kong, Poland, and Seychelles, including a Polish registration for activities in the field of virtual currencies. Notably absent are any current references to an Italian OAM VASP registration, any other clearly identified EEA registrations, or any MiCA/CASP authorisation. In other words, Nexo’s own dedicated licensing page appears to confirm a fragmented and selective regulatory footprint rather than a transparent EEA licensing framework.

Against that background, the regulatory significance of a VASP registration should not be overstated even where one can be verified. National VASP regimes such as Italy’s OAM framework are primarily AML-centered registration systems for defined crypto-asset services such as exchange, transfer, and custody-wallet activity. They are not equivalent to authorisation as a traditional asset manager, discretionary portfolio manager, investment adviser, or bank, all of which sit under separate legal regimes depending on product design and distribution model. In Nexo’s case, however, the more immediate issue is even more basic: the company’s public narrative suggests a wider European regulatory foundation than can currently be verified from official registers, contractual documentation, and its own licensing disclosures.

Product-Level Compliance Analysis

The compliance risk around Nexo becomes clearest at product level. Some parts of the business fit relatively comfortably within the evolving CASP/VASP perimeter, while others move toward securities, investment-management, or banking-like territory depending on how they are structured, marketed, and distributed.

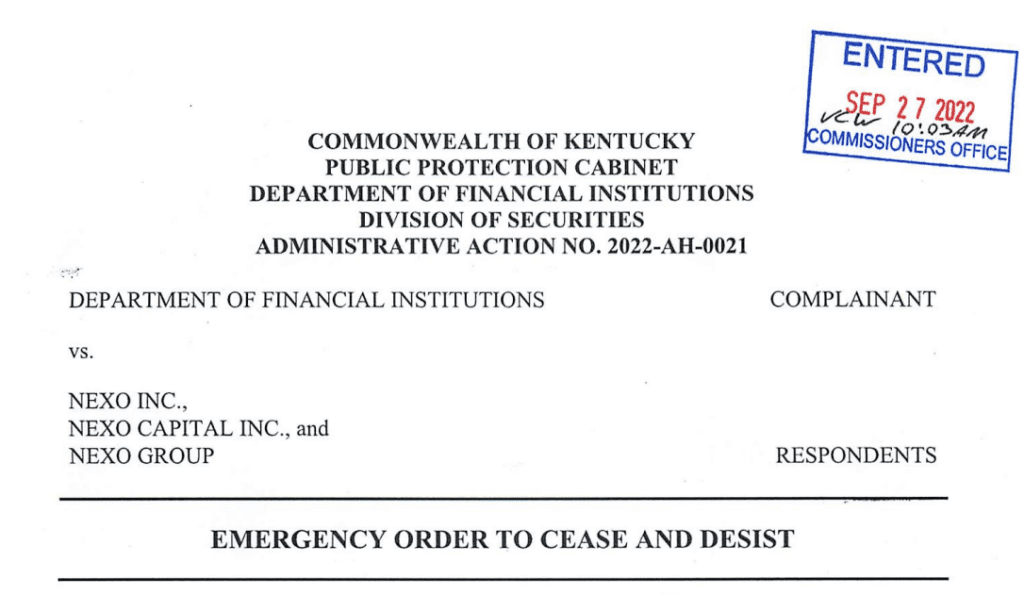

Enforcement History and Why It Matters

Nexo’s regulatory history matters because it shows how supervisors interpret the group’s product set when legal classifications become contested. In the United States, Nexo and related entities entered settlements with the SEC and multiple state regulators over the Earn Interest Product, while other proceedings and public notices raised issues around unregistered securities activity and lending-related licensing.

- Securities Commission of South Carolina: Cease and Desist (2023)

- New York State Attorney General: $24 million settlement over illegal offerings (2023)

- NEXO blog on the US settlement: Nexo reaches landmark solutions with U.S. regulators

These cases do not automatically determine Nexo’s status in the EU, but they are highly relevant compliance signals. When multiple regulators across jurisdictions converge on the view that interest-bearing crypto products may fall outside a platform’s claimed licensing perimeter, European supervisors and compliance officers have little reason to treat similar marketing claims as low-risk.

Corporate Onboarding and the Risk of Compliance Drift

Nexo’s corporate-account page targets businesses and family offices and emphasizes relationship management, OTC execution, custody, and yield opportunities. That positioning is consistent with an attempt to move beyond pure retail crypto intermediation and into treasury-style client relationships.

The risk emerges when onboarding controls expand beyond relevant KYB/KYC into speculative or OSINT-driven assumptions. Available evidence and user reports suggest that Nexo may, in some cases, request documents tied to third-party media platforms or inferred affiliations that are not obviously connected to the applicant entity. If accurate, that would reflect a problematic drift from risk-based due diligence into compliance overreach, with implications for fairness, data minimization, and procedural integrity.

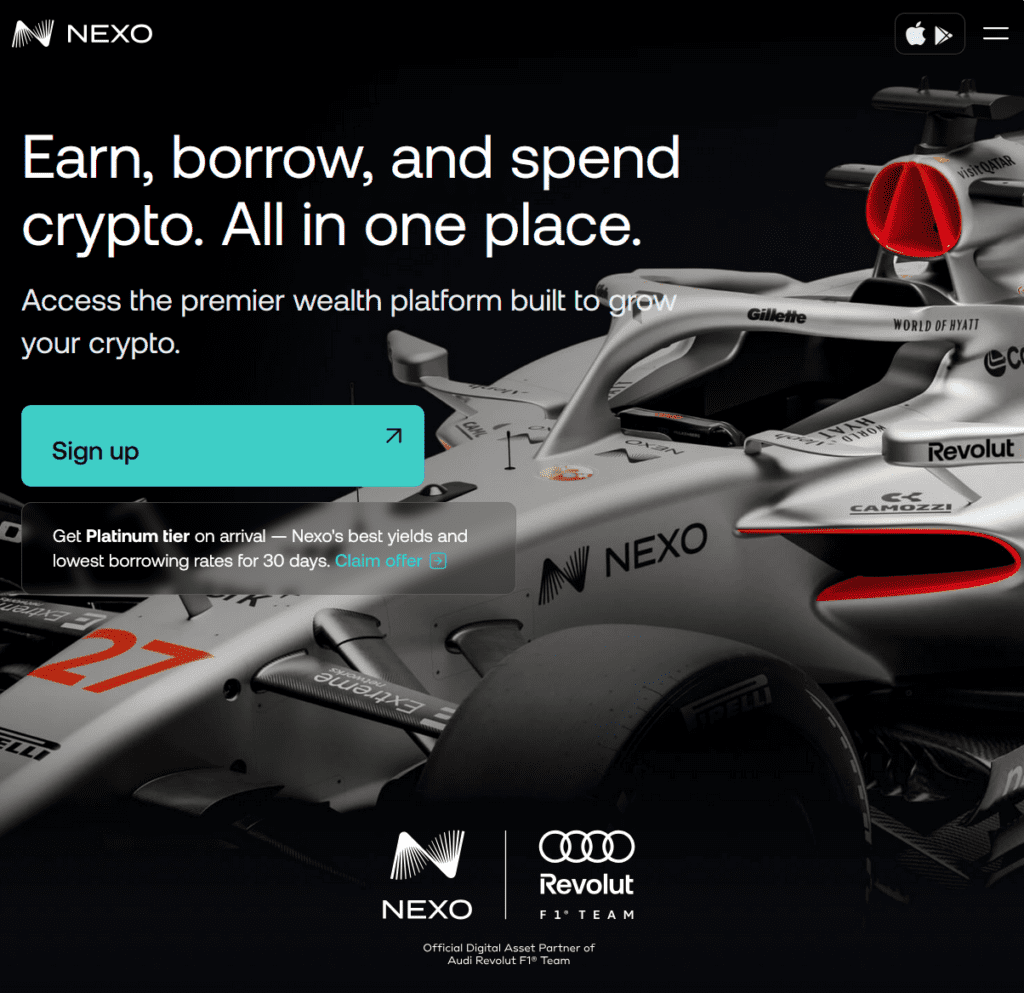

Formula 1 Branding and the Credibility Narrative

Nexo has also moved into high-visibility sports marketing through a multi-year partnership with the Audi Revolut F1 Team, where it is presented as the official digital-asset partner. The Formula 1 car already appears prominently on Nexo’s own website and serves a clear reputational purpose: to project scale, permanence, and mainstream legitimacy at a moment when the group’s EU-facing licensing narrative remains in transition from VASP-era registrations toward MiCA.

From a compliance perspective, that distinction matters. Premium sports sponsorship may strengthen brand trust, but it does not answer the underlying questions around entity transparency, product classification, and the legal basis for marketing yield-bearing and wealth-style crypto services in Europe.

MiCA: The Pressure Test Ahead

MiCA is likely to become the decisive pressure test for Nexo’s EU-facing model. The regulation introduces a more harmonized authorization regime for crypto-asset service providers, clearer conduct and safeguarding obligations, and more explicit treatment of services involving crypto-asset advice and stablecoin-related activity.

For Nexo, this means the room for regulatory ambiguity is narrowing. Exchange, custody, and certain execution services may transition into a cleaner CASP framework, but yield products, lending constructs, and wealth-style marketing will face closer scrutiny where substance begins to resemble investment, deposit, or advisory business rather than pure crypto intermediation.

Compliance Takeaway

Nexo should not be viewed as a conventional regulated wealth manager in Europe. Based on the currently visible public record, it is more accurately described as a crypto-asset platform with a broad product perimeter, supported by VASP-era registrations and in transition toward MiCA, but carrying material licensing, product-governance, and transparency risk in areas such as Earn, corporate yield, lending, and marketing claims.

That distinction is not semantic. It goes directly to client protection, legal classification, contracting-entity clarity, and the question of whether customers and counterparties are dealing with a regulated crypto intermediary, a shadow banking-style yield platform, or a business model that has long relied on the grey space between the two.

Whistleblower Call

FinTelegram invites current and former employees, counterparties, service providers, onboarding clients, and other informed sources with additional information about Nexo’s internal compliance processes, legal entities, beneficial ownership, product governance, and regulatory interactions to come forward. Confidential submissions can be made through the whistleblower platform Whistle42, which is publicly presented as a secure reporting channel for whistleblower intelligence and forensic compliance analysis.

{kind=link}