OpenPayd wants Nasdaq to buy the unicorn story. FinTelegram sees the scam-rail problem. The Ozan Özerk-founded fintech plans to go public through Titan Acquisition Corp. at a proposed $1.145 billion valuation while victim files reviewed by FinTelegram show OpenPayd infrastructure inside alleged investment-fraud payment paths involving Klickl Europe, fake trading apps, and vIBAN-based victim-fund flows.

2-Minute Briefing

OpenPayd wants Nasdaq to buy the unicorn story. FinTelegram sees the scam-rail problem. The Ozan Özerk-founded fintech has announced a business combination with Titan Acquisition Corp., a Nasdaq-listed SPAC. If completed, OpenPayd says it will list on Nasdaq under the ticker OP at a proposed pro-forma equity value of $1.145 billion. The company markets the transaction as a milestone for programmable money, stablecoins, fiat rails, blockchain networks and global payment orchestration.

That is the pitch.

The risk story is harder.

FinTelegram victim files show OpenPayd infrastructure inside alleged scam payment paths in Europe. In the OpenPayd–Klickl Europe cases, victim deposits entered OpenPayd Malta vIBAN / CFTEMTM1 infrastructure and were swept to Klickl Europe Sp. z o.o., a Polish VASP controlled by Chinese interests, with recurring references such as “Sweep to Primary Account.” FinTelegram has also reviewed victim-organized material showing multiple fake investment app frontends feeding the same OpenPayd–Klickl rail.

That is not a theoretical compliance issue. It is the core public-market question.

OpenPayd sells the exact infrastructure that becomes dangerous when abused: virtual IBANs, pooled accounts, open banking, fiat-to-crypto on/off ramps, stablecoin rails, digital-asset payments and iGaming payment infrastructure. A company seeking a Nasdaq listing at unicorn valuation must explain not only its growth metrics, but also how its rails were used in scam contexts.

There is also the founder risk. OCCRP and other media have reported Turkish investigations involving companies owned by Ozan Özerk in connection with alleged money laundering and illegal betting proceeds. OpenPayd is now asking U.S. public-market investors to trust the Özerk fintech ecosystem at scale.

The filing question is blunt: will OpenPayd and Titan disclose the scam-rail reality — or will investors receive only the unicorn brochure?

Key Findings

- OpenPayd is selling a Nasdaq growth story.

The company says the Titan transaction would bring OpenPayd to Nasdaq under ticker OP at a proposed $1.145 billion pro-forma equity valuation. - The business model is high-risk by design.

OpenPayd markets virtual IBANs, pooled accounts, open banking, digital-asset infrastructure, on/off ramps, stablecoins, forex and iGaming payments. These products require hard AML controls. - FinTelegram files place OpenPayd infrastructure inside scam rails.

The OpenPayd–Klickl Europe evidence shows victim funds entering OpenPayd vIBAN infrastructure and being swept to Klickl Europe. - Klickl Europe is not a harmless payment detail.

It appears repeatedly in victim files as the recipient of funds swept from OpenPayd vIBANs. FinTelegram has flagged Klickl as a Chinese-controlled Polish crypto gateway with DAREX D / Red risk treatment. - The fake app layer shows scale.

Victim material identifies dozens of victim-app entries and numerous fake investment apps, including Peelhuntaicore, KXTRA, PHFINCORE, FinTechX, BMEBEX, MirrorTrd, SSGM Pro and YHT. - Ozan Özerk’s wider ecosystem is a material disclosure issue.

Turkish investigations involving Özerk-linked companies and alleged illegal betting proceeds belong in any serious investor-risk review. - The SEC filings will test OpenPayd’s transparency.

The filings should explain the fraud complaints, high-risk customers, vIBAN controls, Klickl exposure, SAR/STR handling, regulatory inquiries and remediation steps.

The SEC Filing: Titan, PubCo, Shareholders — And Ozan Özerk At The Center

The SEC filing confirms that the OpenPayd–Titan transaction is not a simple IPO. It is a SPAC-driven restructuring built around a new Cayman Islands public holding company: OpenPayd Global Holdings Limited (“PubCo”).

Under the Business Combination Agreement dated 1 June 2026, Titan Acquisition Corp. will merge into PubCo. Titan will cease to exist as a separate company, and its shareholders and warrantholders will receive substantially equivalent PubCo securities. PubCo will then acquire all shares of OpenPayd Holdings Limited, the English company operating the OpenPayd business, in exchange for PubCo ordinary shares issued to OpenPayd’s beneficial owners. After the transaction, OpenPayd Holdings Limited will become a direct wholly owned subsidiary of PubCo.

This structure matters. OpenPayd is not simply “listing.” The transaction moves the group into a Cayman-listed public-company wrapper, with the operating OpenPayd business held below it.

Transaction Structure

| Element | SEC Filing Description | FinTelegram Interpretation |

|---|---|---|

| Purchaser / SPAC | Titan Acquisition Corp., Cayman Islands SPAC | Nasdaq vehicle used to bring OpenPayd to market |

| Public company after closing | OpenPayd Global Holdings Limited, Cayman Islands | New PubCo wrapper for the listed group |

| Operating company | OpenPayd Holdings Limited, England & Wales | Existing OpenPayd operating holding company |

| Transaction mechanics | Titan merges into PubCo; PubCo acquires OpenPayd Holdings Limited | De-SPAC plus share acquisition |

| Company consideration | PubCo shares with aggregate value of $800 million, less advisor transaction-fee shares | Core equity consideration for OpenPayd shareholders |

| Minimum proceeds condition | Aggregate transaction proceeds must be at least $130 million, subject to adjustments | Closing depends on available financing / non-redemptions / PIPE support |

| SEC process | PubCo must file a Form F-4 registration statement including Titan proxy/prospectus | The real risk-factor disclosure will come in the F-4 |

| Nasdaq condition | PubCo ordinary shares and warrants must be approved for Nasdaq listing | Listing approval is a closing condition |

| Long-stop date | Transaction may be terminated if conditions are not satisfied or waived by 31 December 2026 | Timeline pressure for Titan, OpenPayd and advisers |

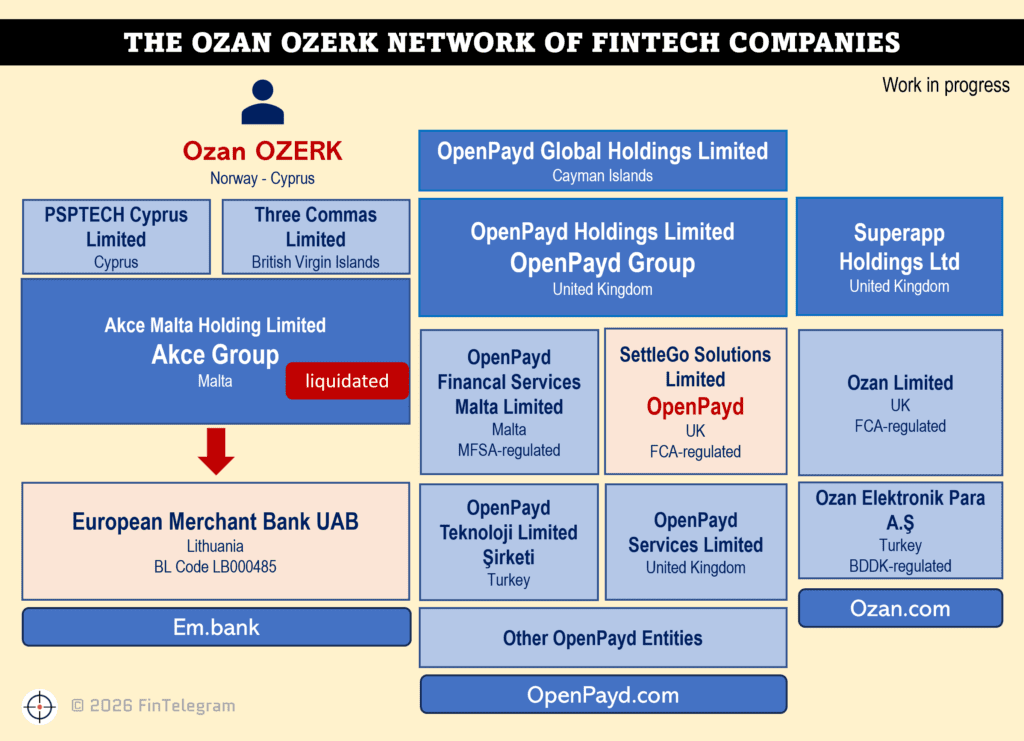

Shareholder Structure: Ozan Özerk Is The Dominant Shareholder

The filing identifies Ozan Özerk, a Cypriot citizen, as the Key Company Shareholder. He directly owns 1,000,000 OpenPayd Holdings Limited shares, representing approximately 82.72% of the company. The remaining 208,953 shares, or approximately 17.28%, are legally held by Zedra Trust Company (Guernsey) Limited as nominee for the relevant beneficial owners.

That means the pre-transaction shareholder structure is not dispersed. It is founder-dominated.

| Shareholder / Holder | Shares | Percentage | Role |

|---|---|---|---|

| Ozan Özerk | 1,000,000 | 82.72% | Direct owner; Key Company Shareholder |

| Zedra Trust Company (Guernsey) Limited | 208,953 | 17.28% | Nominee legal holder for relevant beneficial owners |

| Total | 1,208,953 | 100% | OpenPayd Holdings Limited pre-transaction equity |

The SEC filing also states that PubCo was newly incorporated and, as of signing, was owned entirely by Özerk. That is important: before the SPAC mechanics take effect, the future listed Cayman holding company is initially an Özerk-controlled vehicle.

Ozan Özerk’s Role: More Than Founder Branding

The filing does not treat Özerk as a passive founder. It places him at the center of the transaction. Özerk appears in multiple roles:

- Founder of OpenPayd, presented in the investor materials;

- Key Company Shareholder, holding approximately 82.72% of OpenPayd Holdings Limited directly;

- Company Shareholders Representative, empowered to act for OpenPayd shareholders and beneficial owners in transaction matters;

- sole shareholder of PubCo prior to the transaction mechanics;

- party to a Key Company Shareholder Support Agreement, under which he agrees to support and vote in favor of the transaction;

- party to a Non-Competition Agreement effective at closing;

- recipient of additional SPAC sponsor economics: 1,035,000 PubCo ordinary shares and 1,216,508 PubCo private warrants transferred from the Sponsor in connection with the termination of the Company Shareholders’ Agreement.

This is the core governance point: Özerk is not just the face of OpenPayd. He is the controlling shareholder and transaction control figure.

Why This Matters For The Risk Story

The filing describes OpenPayd’s business as a global, rail-agnostic banking-as-a-service and payments platform enabling fiat and crypto interoperability. It specifically references named virtual IBANs, multi-currency fiat and crypto payment accounts, international and domestic payments, real-time settlements, fiat-to-fiat and crypto-to-fiat-to-crypto conversions, digital wallets, stablecoin minting and burning, on-chain payments, digital-asset trading and blockchain access through a single API infrastructure.

That description is critical for FinTelegram’s analysis. It confirms that the very products at the center of OpenPayd’s growth story — named vIBANs, fiat-to-crypto infrastructure, stablecoin rails, digital wallets and crypto conversion capabilities — are not peripheral services. They are the business model.

This is also why the OpenPayd–Klickl Europe files are material. FinTelegram victim files show OpenPayd vIBAN infrastructure inside alleged scam payment paths, including funds swept to Klickl Europe with references such as “Sweep to Primary Account.” If OpenPayd wants Nasdaq investors to buy a unicorn infrastructure story, the SEC filings must disclose the fraud-rail exposure clearly.

FinTelegram Takeaway

The SEC filing confirms the structure:

Titan SPAC → Cayman PubCo → OpenPayd Holdings Limited → Ozan Özerk-dominated shareholder base → Nasdaq listing attempt.

It also confirms the disclosure battleground. The Form F-4 proxy/prospectus will be the real test. OpenPayd and Titan must decide whether to disclose the difficult facts: OpenPayd vIBAN abuse allegations, Klickl Europe victim flows, fake investment-app rail exposure, high-risk merchant sectors, SAR/STR handling, Turkish investigations involving Özerk-linked firms, and the governance risk of a founder-controlled fintech entering U.S. public markets.

OpenPayd wants to sell Nasdaq the infrastructure story.

The SEC filing shows who controls that story.

FinTelegram will watch what they disclose.

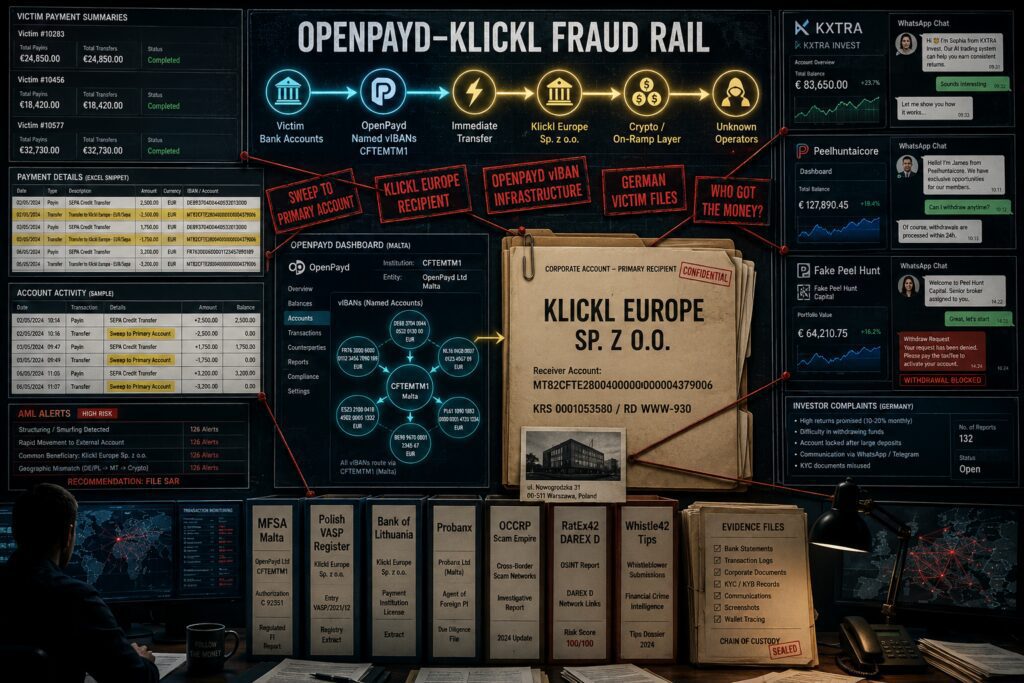

The OpenPayd–Klickl Europe vIBAN Scam Files

The most sensitive issue for OpenPayd’s Nasdaq ambitions is not the marketing story around programmable money, stablecoins, or global payment infrastructure. It is the hard evidence from Europe: victim files reviewed by FinTelegram show OpenPayd infrastructure inside alleged investment-fraud payment rails, with funds repeatedly routed to Klickl Europe Sp. z o.o., a Polish virtual-asset service provider.

Klickl Europe is part of a Chinese-controlled crypto scheme around Michael (Xu) Zhao. SEC filings for Crypto 1 Acquisition Corp identify Zhao as founder, CEO and director. The filing states that he began investing in crypto in 2016, served as founder/executive chairman of International Digital Currency Markets (IDCM), and founded/led VGPay, a crypto-payment business serving crypto exchanges and their clients.

Read our report on “Who is behind Klickl” here.

The pattern is no longer anecdotal. FinTelegram has reviewed GDPR/DSAR responses and OpenPayd “Summary of payments” files received by victims. These files show a recurring structure: victims made deposits into OpenPayd named vIBANs / OpenPayd Malta IBANs using BIC CFTEMTM1. The funds were then transferred onward to Klickl Europe with references such as “Transfer to Klickl Europe – EUR/Sepa” and “Sweep to Primary Account.”

This is the rail map:

Victim bank account → OpenPayd named vIBAN / CFTEMTM1 → Payin → immediate Transfer → “Sweep to Primary Account” → Klickl Europe Sp. z o.o. → crypto/on-ramp or settlement layer → unknown operators

OpenPayd’s own GDPR response in one victim case confirmed the core architecture. The victim was not OpenPayd’s client. OpenPayd’s corporate client was Klickl Europe. The IBAN assigned to the victim was not a normal personal bank account, but a named virtual IBAN linked to Klickl Europe’s payment account. OpenPayd further stated that funds credited through that vIBAN became the property of Klickl Europe.

That point is critical. It means the victim-facing IBAN created the appearance of a personalized payment route, while the economic recipient was Klickl Europe. The victims did not hold real OpenPayd accounts. They were given OpenPayd-generated deposit identifiers that routed money into Klickl Europe’s corporate payment structure.

Read our reports on Klickl Europe-facilited scams here.

FinTelegram has also reviewed victim-organized material showing that the fraud was not limited to one fake investment platform. KXTRA and fake Peel Hunt / Peelhuntaicore appear to be only two frontends in a much wider app layer. Victim material identifies dozens of app-front entries and numerous fake investment apps allegedly feeding the same OpenPayd–Klickl rail, including Peelhuntaicore, KXTRA, PHFINCORE, FinTechX, BMEBEX, MirrorTrd, SSGM Pro, YHT, KKRDE, KzipPro, FD MIN, Quantanils, Phantom, Voya and others.

This points to a repeatable fraud architecture:

Disposable investment apps → WhatsApp / Telegram grooming → OpenPayd vIBAN infrastructure → Klickl Europe recipient account → crypto conversion / settlement → hidden operators

For OpenPayd, the issue is direct. OpenPayd was not a random bank name appearing once in a victim transfer. Its vIBAN infrastructure appears as the fiat-entry rail in multiple victim files. If OpenPayd issued or serviced named vIBANs for Klickl Europe, it should have records showing how many vIBANs were created, how many retail investors paid into them, how many complaints were received, when transaction monitoring triggered alerts, whether SARs or STRs were filed, and when the relationship with Klickl Europe was reviewed, restricted, or terminated.

For Klickl Europe, the issue is even sharper. If the funds were swept into its account, Klickl must know what happened next. It should have customer data, merchant files, transaction records, wallet addresses, conversion records, settlement partners, ledger entries, and compliance alerts. If Klickl was merely used as an on-ramp by fraud operators, it should identify those operators. If it cannot or will not, the suspicion deepens.

The public-market question is therefore unavoidable: how will OpenPayd disclose this in its SEC filings?

OpenPayd’s business model is built around precisely the type of infrastructure that requires hard controls: virtual IBANs, pooled accounts, fiat rails, digital-asset infrastructure, crypto on/off ramps, stablecoin payments and high-risk merchant sectors. The OpenPayd–Klickl files show why those controls matter. Named vIBANs can become powerful tools for fraud operators when they create a personal-account illusion while routing victim money into a corporate crypto/on-ramp account.

This is not a soft compliance footnote. It is a material disclosure issue.

Titan, its advisers, OpenPayd’s lawyers, auditors and ultimately the SEC should ask the obvious questions:

- How many OpenPayd vIBANs were issued for Klickl Europe?

- How much money flowed through the OpenPayd–Klickl rail?

- How many victims complained?

- How many fake investment apps were connected to the rail?

- Were suspicious activity reports filed?

- Was Klickl Europe terminated or restricted?

- Did OpenPayd disclose these facts to Titan and its transaction advisers?

- Will the Form F-4 / proxy materials include a specific risk factor on vIBAN abuse, fraud-rail exposure and high-risk crypto intermediaries?

OpenPayd wants investors to see scalable global payment infrastructure. FinTelegram’s victim files show the other side of that scale: when vIBAN infrastructure is used by fraud networks, the same technology can become a victim-fund collection machine. That is why the OpenPayd–Klickl Europe files belong in the Nasdaq disclosure discussion.

The OCCRP Findings

The Organized Crime and Corruption Reporting Project (OCCRP) reported that Turkish authorities launched a money-laundering investigation targeting companies in the corporate network of Cypriot-Norwegian fintech entrepreneur Ozan Özerk, OpenPayd’s founder and controlling figure. According to OCCRP, the Turkish probe concerns Ozan Elektronik Para A.Ş., an electronic-money institution allegedly used to introduce criminal assets — primarily from illegal betting — into the financial system, and Aveon Global Sigorta A.Ş., another Özerk-majority-owned company allegedly used to inject criminal proceeds disguised as insurance premiums.

OCCRP further noted that its earlier Scam Empire investigation found fraud payments running through dozens of companies, including OpenPayd and European Merchant Bank, both owned by Özerk; OCCRP stressed that there was no evidence those companies knew the funds were fraud-derived. For FinTelegram’s OpenPayd–Titan analysis, the point is clear: OpenPayd’s Nasdaq ambitions sit against a wider Özerk ecosystem already linked by investigative reporting and Turkish authorities to money-laundering, illegal-betting and scam-payment questions.

Conclusion

OpenPayd wants the market to see a unicorn.

FinTelegram sees the rail map.

Victims paid into OpenPayd infrastructure. Funds were swept to high-risk crypto intermediaries. Fake app frontends multiplied. Turkish investigations around Özerk-linked companies remain part of the risk landscape.

Nasdaq investors should not receive a unicorn brochure while victims hold the payment files.

OpenPayd’s listing is a disclosure test.

If the company wants public-market trust, it must disclose the fraud-rail reality.

Summary Table — OpenPayd Nasdaq Pitch vs. Scam-Rail Reality

The following table contrasts OpenPayd’s Nasdaq pitch with the FinTelegram risk file. The transaction is not only a capital-markets event; it is a disclosure test for OpenPayd, Titan, their advisers, and ultimately the SEC.

| Category | Key Data / Entity | What OpenPayd / Titan Present | FinTelegram Risk Context |

|---|---|---|---|

| Transaction | OpenPayd business combination with Titan Acquisition Corp. | OpenPayd plans to go public through a SPAC merger with Titan. Upon closing, OpenPayd expects to list on Nasdaq under ticker OP. | The transaction turns OpenPayd’s risk profile into a public-market disclosure issue. |

| Proposed valuation | $1.145 billion pro-forma equity value | OpenPayd markets the transaction as a unicorn-valuation milestone. | The valuation must be tested against unresolved AML, fraud-rail, high-risk merchant and founder-risk exposure. |

| Potential proceeds | Up to $276 million from Titan’s trust account, assuming no redemptions | OpenPayd presents this as growth capital for its next phase. | Investor redemptions and SEC scrutiny may increase if risk disclosures are weak or incomplete. |

| Titan Acquisition Corp. | Nasdaq SPAC, ticker TACHU / Class A shares TACH / warrants TACHW | Titan raised $276 million in its April 2025 IPO and is positioned as a SPAC seeking a business combination. | Titan’s due diligence must address OpenPayd’s high-risk payment exposure, not only growth metrics. |

| Titan leadership | Chairman & CEO Frank Mastrangelo | Titan publicly praises OpenPayd as a high-growth financial infrastructure platform. | Titan and its advisers become gatekeepers for SEC disclosure of OpenPayd’s risk profile. |

| OpenPayd positioning | Global financial infrastructure for fiat rails, blockchain networks and stablecoins | OpenPayd claims to operate at the intersection of traditional finance and digital assets. | This is precisely the risk zone where scam operators exploit fiat-to-crypto rails. |

| OpenPayd metrics | More than 1,100 customers, over $240 billion annualized transaction volume, over $85 million ARR as of March 2026 | OpenPayd uses these figures to support the unicorn narrative. | Large volume increases AML burden. Scale makes scam-rail exposure more material, not less. |

| Core OpenPayd infrastructure | vIBANs, pooled accounts, fiat payments, stablecoin/on-off ramps, digital-asset infrastructure | Marketed as programmable money movement and embedded financial infrastructure. | FinTelegram files show OpenPayd vIBAN infrastructure appearing in alleged investment-fraud payment paths. |

| OpenPayd Malta rail | OpenPayd Malta IBAN / CFTEMTM1 | Not part of the investor pitch. | FinTelegram victim files identify OpenPayd Malta / CFTEMTM1 as the fiat-entry infrastructure in multiple scam contexts. |

| Klickl Europe | Klickl Europe Sp. z o.o., Polish VASP, RD WWW-930 | Not addressed in OpenPayd’s Nasdaq announcement. | FinTelegram victim files show funds routed through OpenPayd vIBANs and swept to Klickl Europe with references such as “Sweep to Primary Account.” |

| Klickl risk profile | Chinese-controlled Polish crypto/on-ramp structure | Not part of OpenPayd’s public SPAC pitch. | Klickl Europe appears as the EU-facing recipient node in the OpenPayd scam-rail files. RatEx42 flagged Klickl Red / DAREX D. |

| App-front layer | KXTRA, fake Peel Hunt / Peelhuntaicore, PHFINCORE, FinTechX, BMEBEX, MirrorTrd, SSGM Pro, YHT and others | Not addressed in OpenPayd’s Nasdaq narrative. | Victim material indicates numerous fake investment apps fed funds into the OpenPayd–Klickl rail. |

| Founder / ecosystem risk | OpenPayd founder Ozan Özerk | OpenPayd presents a fintech growth story. | OCCRP and other media reported Turkish investigations involving Özerk-linked companies and allegations concerning money laundering and illegal betting proceeds. |

| Regulatory issue | SEC filings / Form 8-K / proxy or registration documents | OpenPayd says additional transaction documents will be filed with the SEC. | The filings should disclose scam complaints, Klickl exposure, vIBAN abuse, high-risk merchants, SAR/STR handling, and Özerk-linked investigation risk. |

| Core FinTelegram question | Disclosure test | OpenPayd wants Nasdaq investors to buy the unicorn story. | Will investors receive the full scam-rail risk picture — or a polished fintech growth brochure? |

The issue is not whether OpenPayd has scale. The issue is whether a company built on vIBANs, pooled accounts, fiat-to-crypto rails and high-risk payment infrastructure will fully disclose how often its rails appeared in scam payment paths.

Whistleblower Call

FinTelegram calls on victims, insiders, former employees, compliance officers, payment specialists, OpenPayd clients, Titan advisers, auditors, lawyers, regulators, and law-enforcement contacts to come forward.

We are looking for documents and information relating to:

- OpenPayd vIBANs / named IBANs, especially OpenPayd Malta / CFTEMTM1;

- scam complaints involving OpenPayd infrastructure;

- OpenPayd–Klickl Europe payment flows;

- GDPR / DSAR responses from OpenPayd;

- “Summary of payments” files showing Payin / Transfer patterns;

- references such as “Sweep to Primary Account”;

- Klickl Europe account statements, wallet data, merchant records, or onboarding files;

- fake investment apps connected to OpenPayd rails;

- internal OpenPayd risk alerts, SAR/STR filings, account freezes, customer exits, or remediation steps;

- communications with Titan Acquisition Corp., auditors, legal advisers, investment banks, or SEC-facing counsel;

- any due-diligence material prepared for the planned Nasdaq transaction;

- information on Ozan Özerk-linked entities, Turkish investigations, illegal gambling exposure, or high-risk merchant relationships.

If OpenPayd wants a Nasdaq listing at unicorn valuation, investors deserve the full risk picture. Victims should not be left with payment files while public-market investors receive a sanitized fintech growth story.

Documents can be submitted securely via Whistle42. FinTelegram will protect sources and redact personal data where necessary.

{kind=link}