FinTelegram’s deposit-flow tests at PlatinCasino (platincasino.com) show a deliberately confusing payments stack: “bank transfers” that actually buy stablecoins and push them to wallets, plus “Sofort”/open-banking flows that route users through EU-regulated fintech rails. The result: an offshore casino can collect player funds across Europe while keeping onboarding friction—and KYC prompts—remarkably low.

Key Points

- PlatinCasino is presented as a Curaçao-licensed operator (Latiform B.V.) but is accessible across multiple EU/UK jurisdictions (Source: cert.gcb.cw).

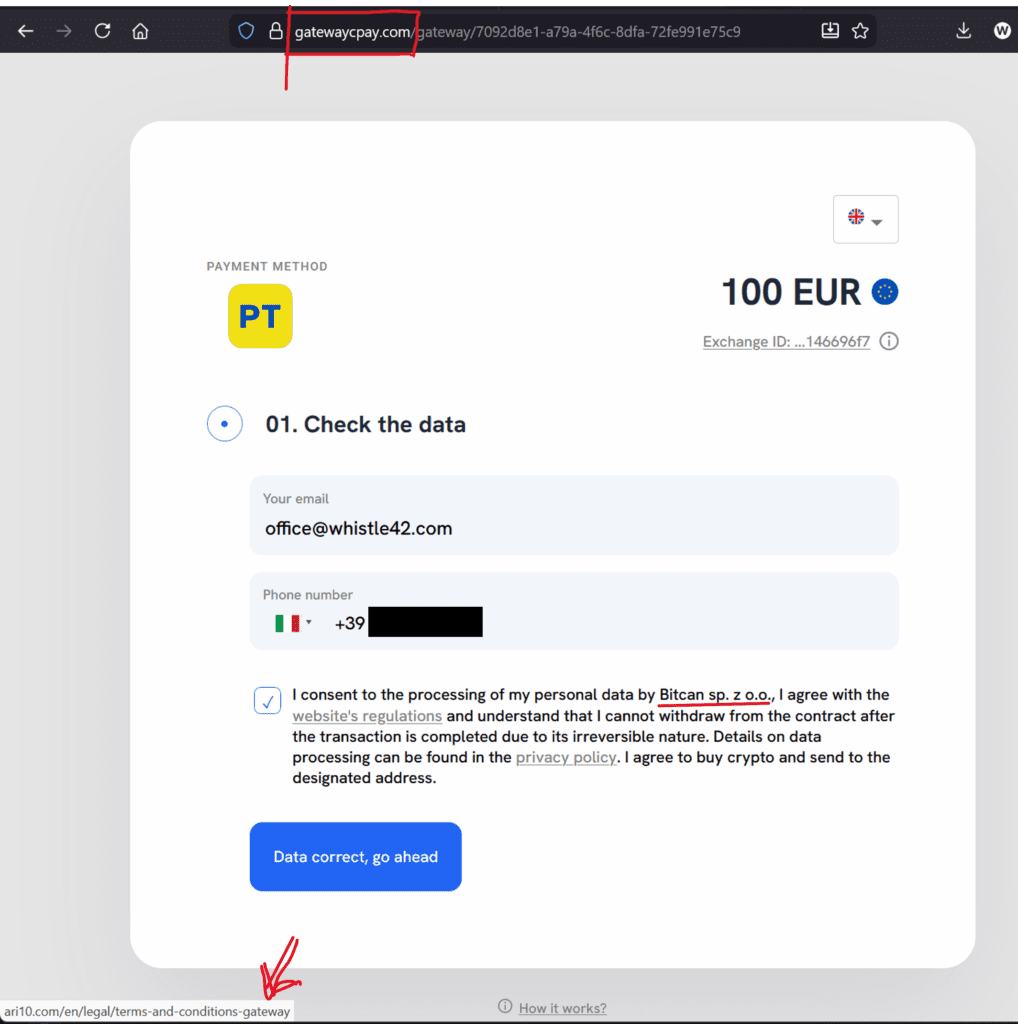

- “Bank Transfer” triggers a fiat→crypto purchase flow referencing Bitcan sp. z o.o. and ARI10, with small-print explicitly describing crypto purchase + wallet delivery.

- The checkout UI discloses stablecoin settlement (USDC/USDT) to specific EVM wallet addresses (per screenshots), undermining the “bank transfer” framing.

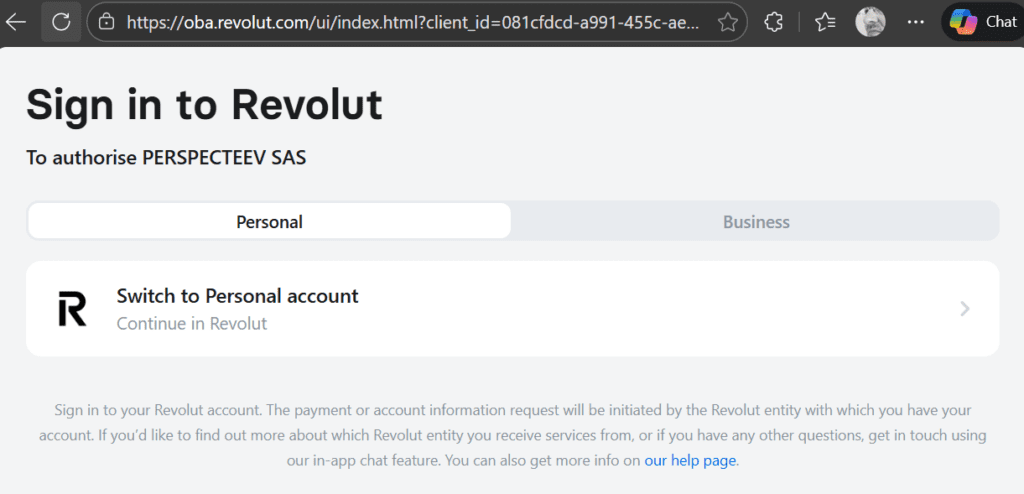

- “Sofort” is implemented as an open-banking initiation journey (secure.bankgate.io → bank selection → Revolut OBA), requesting consent to authorize PERSPECTEEV SAS (Bridge) (Source: bridgeapi).

- SALTEDGE branding appears on a bankgate.io 404 screen during the hop—suggesting a white-label/open-banking infrastructure layer.

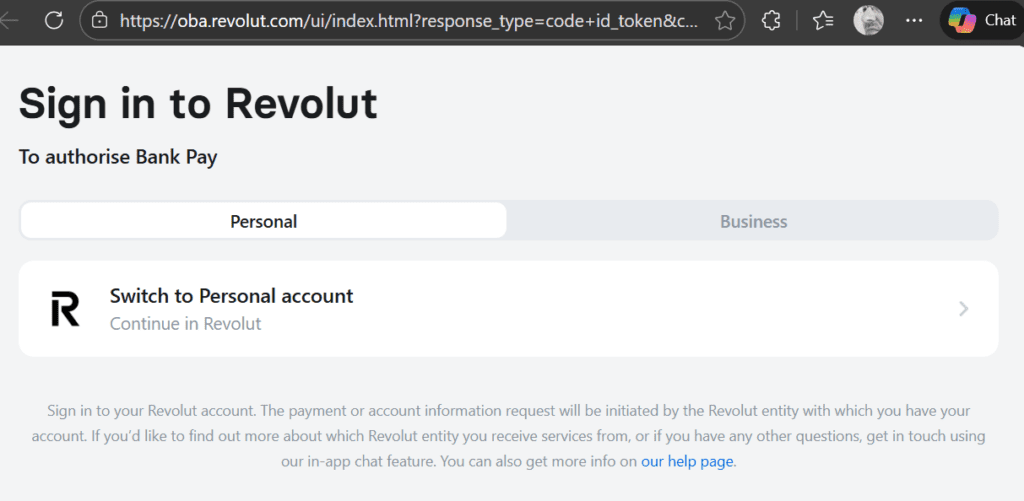

- Another “anonymous” open-banking gateway appears via checkout.transactgrid.com, leading to Revolut consent to authorize “Bank Pay” (operator unclear).

Short Narrative

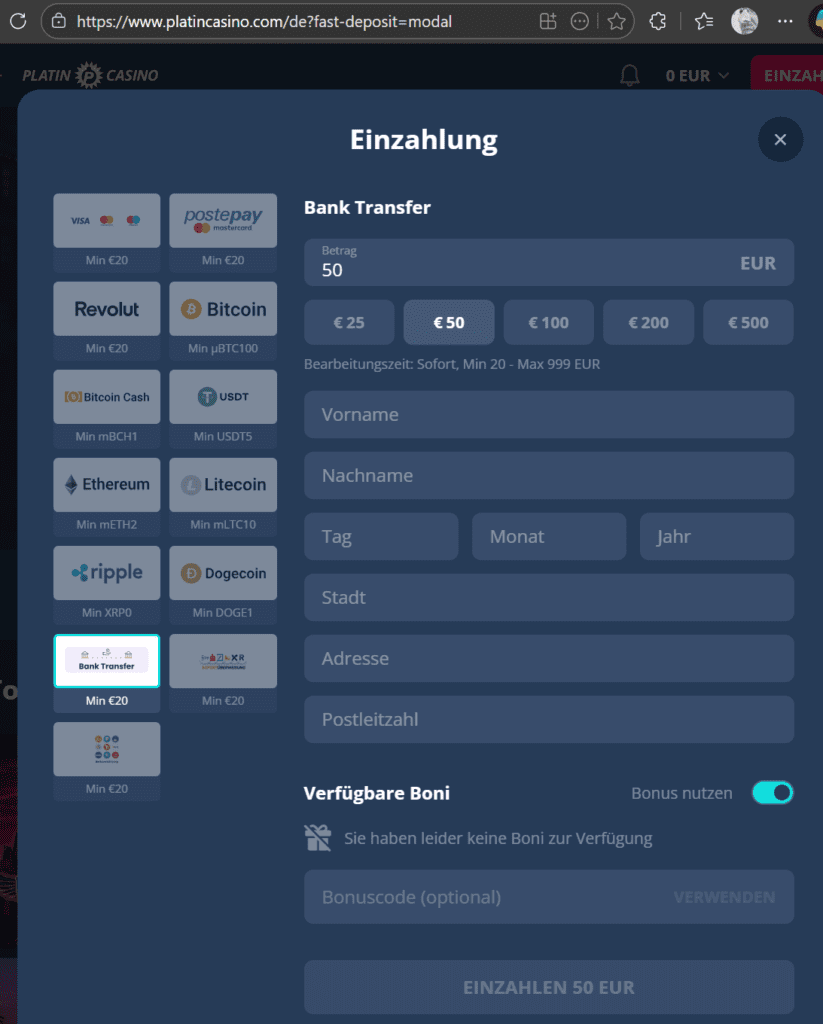

In the PlatinCasino cashier, “Bank Transfer” does not behave like a conventional pay-by-bank deposit. Instead, the user is routed to gatewaycpay.com, asked to confirm personal data, and required to accept terms referencing Bitcan sp. z o.o.

The screen copy states the user is buying crypto and sending it to a designated address (irreversible transaction).

Extended Analysis

1) The operator + regulatory setting

PlatinCasino is operated by Latiform B.V. (Curaçao) under a Curaçao Gaming Control Board license shown in the regulator’s certificate portal (Source: cert.gcb.cw).

In practice, this offshore setup routinely collides with EU national gambling regimes—yet the payments layer (below) helps the casino access EU rails anyway.

In our reviews, we had no problem registering with PlatinCasino as residents of various EU jurisdictions and the UK and making deposits via crypto or FIAT without KYC. The payment facilitators involved should also have no problem with PlatinCasino illegally targeting players in these jurisdictions.

In parallel, PlatinCasino’s “Sofort” option—normally associated by consumers with mainstream pay-by-bank—runs as a multi-hop open-banking consent flow: secure.bankgate.io presents bank selection; choosing Revolut redirects to Revolut’s OBA login where the user is asked to authorize PERSPECTEEV SAS.

2) Chokepoint #1 — “Bank transfer” that is actually a stablecoin purchase

Your screenshots show the decisive tell: the user is told they buy USDC for EUR and that funds will be transferred to specific 0x… wallet addresses. This looks like a fiat-to-crypto on-ramp gateway embedded inside a casino “deposit” journey—i.e., a deposit disguised as a bank transfer, executed as a crypto purchase.

The entities surfaced in-flow align with ARI10’s own positioning as a crypto payment gateway / on-ramp/off-ramp provider (Source: ari10.com)

ARI10’s legal notes also list Bitcan Sp. z o.o. and indicate inclusion in Poland’s Register of Virtual Currency Activities (RDWW-227) (Source: ari10.com).

Important compliance nuance: Poland’s VASP register is a registration regime and does not equal prudential supervision—a point the Polish government itself flags in public guidance about the register (Source: Gov.pl).

Compliance trigger: consumer deception risk (misleading payment method labeling), plus AML/KYC gap risk when “bank transfer” UX masks an on-ramp and stablecoin settlement layer.

3) Chokepoint #2 — “Sofort” as open banking authorization (Bridge / Perspecteev)

The Revolut consent screen in your evidence explicitly requests authorization for PERSPECTEEV SAS. Bridge’s legal disclosures identify Perspecteev SAS as the entity behind Bridge and describe its regulatory framework (PSD2-context service structure) (Source: bridgeapi).

This matters because it demonstrates how an offshore casino can still present users with a familiar EU fintech trust surface (bank selection → Revolut login → consent screen), even where the underlying merchant is an offshore gambling operator.

4) Chokepoint #3 — transactgrid + “Bank Pay” (unattributed)

A second open-banking gateway appears at checkout.transactgrid.com, which we could not reliably attribute via public records at the time of writing. The downstream Revolut OBA consent requesting authorization for “Bank Pay” suggests a separate TPP/merchant descriptor. One possible lead is Paybank2bank, which publicly describes itself as operated by Intense Technologies SRL (Romania)—but we cannot confirm it is the same “Bank Pay” shown in your Revolut screen (Source: PayBank2Bank).

Why this matters: unattributed gateways are classic chokepoints—they are the points where regulated financial rails meet opaque merchant networks.

Rail Map Mini

- Distribution: PlatinCasino front-end (platincasino.com) [Confirmed – observed]

- Collection layer A (disguised on-ramp): gatewaycpay.com → Bitcan/ARI10 terms → aripayments.com redirect [Confirmed – observed]

- Conversion/Settlement: EUR → USDC/USDT purchase; stablecoins routed to EVM wallets [Confirmed – observed]

- Collection layer B (open banking): secure.bankgate.io → Revolut OBA → authorize Perspecteev (Bridge) [Confirmed – observed / Corroborated – entity] (Source: bridgeapi.io).

- Collection layer C (open banking, unattributed): checkout.transactgrid.com → Revolut OBA → authorize “Bank Pay” [Confirmed – observed / Operator Unknown]

Actionable Insight

For regulators, banks, and open-banking providers: PlatinCasino’s flow illustrates a repeatable pattern—merchant risk is shifted away from the casino UI and into payment “hops” (gateway domains, white-label connectors, and stablecoin settlement). The compliance question is not only who processes the payment, but who performs merchant due diligence on the gambling counterparty at each hop—and whether consumer-facing labels (“Bank Transfer”, “Sofort”) are materially misleading.

Summarizing Tables

Entity & jurisdiction transparency

| Brand / Component | Role in the deposit flow | Domains / endpoints observed | Legal entity (as evidenced) | Jurisdiction | Related individuals (public-facing) | Notes / transparency flags |

|---|---|---|---|---|---|---|

| PlatinCasino | Offshore casino (merchant / deposit origin) | platincasino.com | Latiform B.V. (imprint/ownership presented) | Curaçao | Not disclosed on the casino imprint (as observed) | Accessible across EU/UK jurisdictions in testing; deposits possible with minimal friction and no meaningful KYC prompts (observed). |

| “Bank Transfer” rail (disguised crypto purchase) | Misleading method label: user selects “Bank Transfer” but flow states crypto purchase + wallet transfer |

gatewaycpay.com/gateway/…aripayments.com/t/…Terms/Privacy links route to ari10.com

| Bitcan sp. z o.o. (named in consent on checkout screen); legal links routed via ARI10 pages | Poland (per in-flow entity naming) | Not consistently disclosed in the player UX | Checkout copy indicates stablecoin settlement and a destination wallet. Consumer-facing “bank transfer” framing is contradicted by the crypto purchase wording (observed). |

| ARI10 | Crypto gateway ecosystem / legal-document host referenced by the flow | ari10.com | ARI10 sp. z o.o. (as presented on company site / legal pages) | Poland | Leadership listed on company materials (e.g., Mateusz Kara; Izabela Mazur; Artur Pszczółkowski) | Brand/entity layering: user consents to Bitcan wording but is routed to ARI10-hosted legal documents (observed). |

| Bitcan | Entity named in consent (“processing of my personal data by Bitcan…”) and transaction framing | Named inside the gatewaycpay.com checkout UI; legal links to ari10.com | Bitcan sp. z o.o. (named in-flow) | Poland | Not reliably disclosed inside the casino journey beyond the consent line | Consent language + “irreversible” warning are consistent with a crypto purchase / on-chain transfer rather than a normal bank transfer deposit (observed). |

| gatewaycpay | Hosted checkout UI for the disguised “Bank Transfer” rail | gatewaycpay.com/gateway/… | Not clearly disclosed on the domain itself (in-flow references point to Bitcan/ARI10) | Unknown (in-flow context indicates Polish entities) | n/a | Key “chokepoint” domain: handles bank selection, data check, consent, and crypto purchase disclosures (observed). |

| ARIPayments | Redirect / handoff layer after consent | aripayments.com/t/… | Not clearly disclosed in the redirect URL itself | Unknown (in-flow context indicates Polish ecosystem) | n/a | Translation prompt indicated Polish page language during redirect; additional hop increases opacity for users and investigators (observed). |

| “Sofort” rail (open banking PIS) | Brand misdirection: “Sofort” label triggers open-banking authorisation journey | secure.bankgate.io/payments/connect/… → oba.revolut.com/… | In-flow operator not clearly disclosed; Salt Edge branding appears on related bankgate endpoint screens | Unknown (gateway) / UK (Salt Edge context) | n/a | UX behaves as open banking payment initiation, not a classic Klarna Sofort checkout (observed). |

| bankgate.io (open banking gateway) | Open banking bank-selection / routing UI | secure.bankgate.io | Not clearly disclosed in-flow; Salt Edge branding observed on error page | Unknown (gateway) / UK (Salt Edge context) | n/a | Salt Edge logo appears on a secure.bankgate.io 404 screen (observed), suggesting infrastructure involvement. |

| SALTEDGE | Open banking infrastructure / gateway tooling (as suggested by branding) | saltedge.com (brand shown on bankgate-related screen) | Salt Edge (corporate structure varies by jurisdiction; UK presence publicly described) | UK (public-facing positioning) | n/a | Branding suggests Salt Edge technology in the chain; direct contracting party for this merchant flow is not confirmed from the screenshots alone. |

| Bridge / Perspecteev SAS | TPP/PISP being authorised by the user (open banking) |

Authorisation shown at oba.revolut.com (“To authorise PERSPECTEEV SAS”)Legal presence: bridgeapi.io

| Perspecteev SAS d/b/a Bridge | France | Public-facing leadership exists on company materials (not always shown in the authorisation screen) | Critical chokepoint: a regulated EU fintech entity is the explicit authorisation counterparty within an offshore casino deposit journey (observed). |

| Revolut (example bank tested) | User bank login and authorisation endpoint | oba.revolut.com/ui/index.html?… | Revolut entity depends on the customer/account (not determinable from screenshots alone) | Multi-jurisdictional (group) | n/a | User is prompted to authorise a third party (e.g., Perspecteev SAS; “Bank Pay”) enabling the deposit via open banking (observed). |

| TransactGrid | Additional open banking gateway UI (operator unclear) | checkout.transactgrid.com/… | Unknown (no clear imprint/attribution identified in this review) | Unknown | n/a | Second chokepoint: bank-selection gateway with unclear operator, licensing, and complaint channel. |

| “Bank Pay” / “PayBank” (authorisation label) | TPP label shown to the user during open banking authorisation | Appears within oba.revolut.com authorisation (“To authorise Bank Pay/PayBank”) | Unknown (label only; no confirmed corporate mapping) | Unknown | n/a | Attribution gap: the authorisation name is shown, but the underlying legal entity is not transparently disclosed to the user within the casino deposit journey (observed). |

Rail Map Mini

| Step | “Bank Transfer” (disguised crypto purchase) | “Sofort” (open banking via bankgate → Revolut → Perspecteev SAS) | Other open banking option (TransactGrid → Revolut → “Bank Pay”) |

|---|---|---|---|

| 1 | platincasino.com deposit modal → user selects Bank Transfer (observed) | platincasino.com deposit modal → user selects Sofort (observed) | platincasino.com deposit modal → user selects an open banking method (observed) |

| 2 | Pop-up at gatewaycpay.com/gateway/<id>/select → country/bank selection (observed) | Pop-up at secure.bankgate.io/payments/connect/<id> → bank selection (observed) | Pop-up at checkout.transactgrid.com/… → bank selection (observed) |

| 3 |

gatewaycpay.com/gateway/<id> “Check the data” → consent checkbox includes:“I consent to the processing of my personal data by Bitcan sp. z o.o. …” Terms/Privacy links route to ari10.com (observed)

|

Redirect to oba.revolut.com/ui/index.html?… → “Sign in to Revolut”“To authorise PERSPECTEEV SAS” (observed) |

Redirect to oba.revolut.com/ui/index.html?… → “Sign in to Revolut”“To authorise Bank Pay / PayBank” (observed) |

| 4 |

Same screen discloses crypto purchase/transfer logic: user buys USDC/USDT for EUR and funds are transferred to a specified wallet address (observed) | User authorises Perspecteev SAS in Revolut OBA; payment initiation proceeds (return URL not captured) (observed) | User authorises “Bank Pay/PayBank” in Revolut OBA; payment initiation proceeds (return URL not captured) (observed) |

| 5 | aripayments.com/t/<id> appears (“Redirecting to payment page…”, Polish UI prompt) (observed) | During gateway probing, a secure.bankgate.io screen shows Salt Edge branding with a 404 error (observed) | Operator attribution remains unclear for transactgrid.com (gap) |

| 6 | Handoff continues to the selected bank flow; outcome described as crypto purchase + on-chain transfer to wallet (as stated on checkout) (observed) | Net effect: offshore casino deposit executed via regulated open banking rails (TPP shown to user = Perspecteev SAS) (observed) | Net effect: offshore casino deposit executed via open banking rails with unattributed/unclear TPP identity behind the “Bank Pay/PayBank” label (observed) |

Call for Information

Are you a player affected by these deposit flows, or an insider at any of the involved gateways/TPPs (ARI10/Bitcan, bankgate, transactgrid, Bridge/Perspecteev, or banking partners)? FinTelegram is building a rail pack on PlatinCasino’s payment stack. Submit information securely via Whistle42.com (screenshots, bank descriptors, wallet destinations, email receipts, chargeback/freeze experiences).

{kind=link}