Dear Valued Investors,

Buckle up, because MicroStrategy—now rebranded as Strategy (Strategy.com)—has just dropped a bombshell that’s shaking the financial world to its core. In Q1 2025, the company posted a jaw-dropping $4.2 billion loss, driven by a $5.9 billion writedown on its massive Bitcoin (BTC) holdings after a brutal collapse in BTC’s price. Yes, you read that right: $4.2 billion in the red. But hold onto your hats, because Executive Chairman Michael Saylor isn’t backing down. Instead, he’s doubling down, announcing a $21 billion at-the-market equity offering to buy even more Bitcoin.

A Software Company Goes All Bitcoin

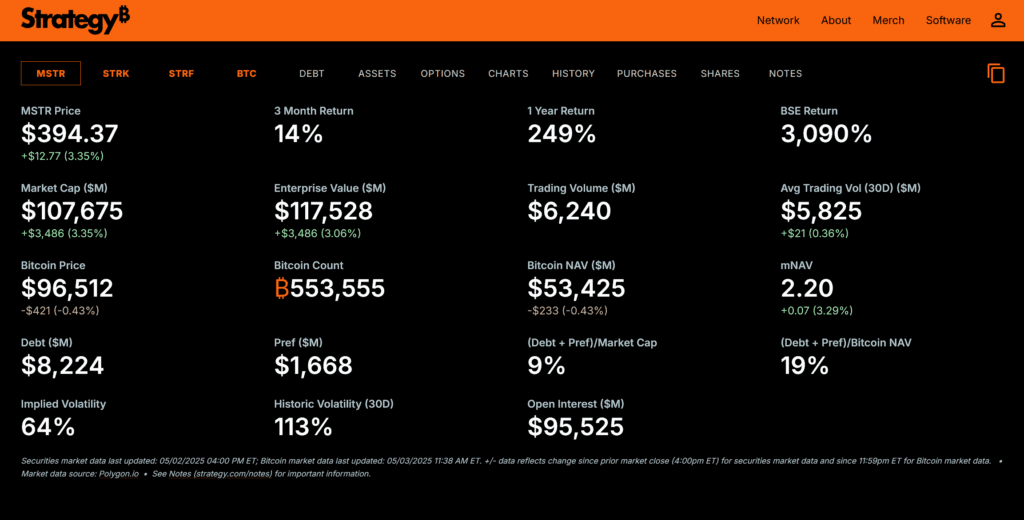

Why is a software company, once known for business intelligence and cloud services, betting the farm on the world’s most volatile asset? Why is Saylor, a self-proclaimed “Bitcoin maximalist,” steering MicroStrategy into uncharted territory as the largest institutional investor in Bitcoin, holding a staggering 553,555 BTC worth roughly $53 billion at current prices?

And why, despite persistent bankruptcy rumors and concerns about financial ruin during BTC bear markets, does Saylor remain unshaken, preaching Bitcoin as the key to “economic immortality”? This investor update dives into the audacious, provocative, and downright polarizing strategy that’s made Strategy a lightning rod for debate—and asks: Is this brilliance or madness?

The Bitcoin Behemoth: MicroStrategy’s High-Stakes Gamble

Let’s rewind. In August 2020, Strategy made headlines when Saylor announced the company would pivot from holding cash to investing in Bitcoin as its primary treasury reserve asset. Since then, Strategy has amassed over 2.5% of all Bitcoin that will ever exist, spending $37.9 billion at an average price of $68,459 per BTC. This isn’t pocket change—it’s a financial juggernaut, funded through a dizzying array of convertible bonds, equity offerings, and debt issuances. The company’s latest move? A fresh $21 billion stock offering to fuel its Bitcoin-buying spree, even after exhausting a previous $21 billion offering.

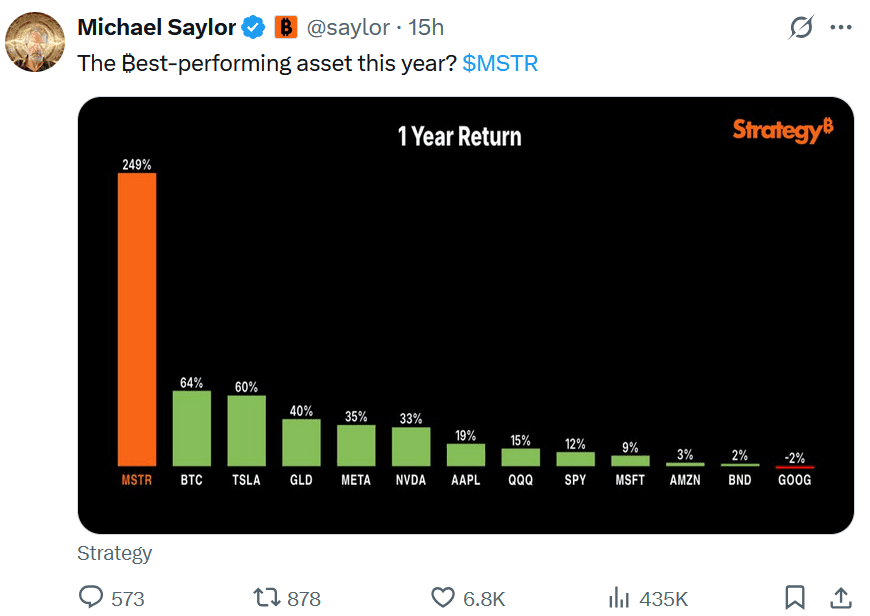

Saylor’s logic is seductive: Bitcoin is “digital gold,” a hedge against inflation, and a transformative asset for the AI-driven future. He envisions BTC soaring to $13 million by 2045, potentially pushing Strategy’s market cap to a mind-boggling $10 trillion. So far, the market has rewarded this boldness. Strategy’s stock has surged 27% year-to-date in 2025, and its market capitalization has skyrocketed, briefly topping $100 billion in late 2024. Since adopting Bitcoin, the company’s shares have climbed nearly eightfold, outpacing BTC’s own gains.

But here’s the kicker: Strategy’s core software business is shrinking. Q1 2025 software revenue fell 3.6% to $111.1 million, a far cry from the billions tied up in BTC. Why is a company built on data analytics and cloud services morphing into a Bitcoin hedge fund? And why are investors cheering a strategy that’s so wildly detached from its original mission?

The Dark Side: Bankruptcy Rumors and Bear Market Nightmares

Don’t get too comfortable. Strategy’s Bitcoin obsession has a dark side, and the Q1 2025 loss is a glaring red flag. The $4.2 billion hit stems from a $5.9 billion impairment charge on its BTC holdings, triggered by a sharp decline in Bitcoin’s price. This isn’t the first time Strategy has bled red ink—previous quarters saw impairment charges like $191.6 million in Q1 2024 and $670.8 million in Q4 2024. New accounting rules effective in Q1 2025 will allow fair value reporting, eliminating these writedowns, but that’s cold comfort when BTC’s volatility can wipe out billions overnight.

The bigger concern? Debt. Strategy’s aggressive Bitcoin purchases are funded by $8.2 billion in outstanding debt, including convertible notes due in 2027 and beyond. While its 553,555 BTC are unencumbered (no collateral pledged), a prolonged bear market could spell disaster. If BTC crashes to, say, $30,000, the value of Strategy’s holdings would plummet to $16.6 billion—barely double its debt. Analysts warn that “spring forward” clauses in its debt agreements could force early repayments if liquidity covenants are breached, potentially pushing the company toward financial distress or bankruptcy.

This isn’t theoretical. In February 2025, Strategy’s stock cratered 55% from its November 2024 peak of $543, trading at $250 as BTC stumbled. Leveraged products tied to MSTR, like MSTX and MSTU, tanked 90% from their highs. Social media has been ablaze with warnings, with X users like

Why Risk It All? Saylor’s Vision vs. Corporate Sanity

So why is Saylor, a former rocket scientist with degrees from MIT, betting MicroStrategy’s future on Bitcoin? His vision is nothing short of apocalyptic: Bitcoin as a $200 trillion asset class, a global settlement layer for AI, and a U.S. Strategic Bitcoin Reserve to cement American dominance. He’s compared his strategy to Manhattan real estate developers, leveraging rising asset values to borrow and build taller. Saylor’s even pitched Bitcoin to Microsoft’s board, urging them to ditch “toxic” bonds for BTC.

But let’s be real: Is this a software company or a crypto casino? Critics like David Krause, emeritus professor at Marquette University, slam Saylor’s approach as “inappropriate,” arguing that corporate treasuries should stick to low-risk, liquid assets like money market instruments. Citron Research’s Andrew Left, once a Strategy bull, now shorts MSTR, warning that its valuation—often three times the value of its Bitcoin holdings—has “completely detached from fundamentals.”

Saylor’s track record doesn’t inspire universal confidence. In 2000, he settled an SEC fraud case for $8.3 million over Strategy’s misreported financials, and in 2024, he paid a $40 million fine for tax fraud. Yet, he’s hailed as a visionary, with Strategy’s inclusion in the Nasdaq-100 and aspirations for the S&P 500 fueling institutional hype. Over 70 public companies have followed Saylor’s lead, adopting Bitcoin as a treasury asset. Is he a prophet leading a financial revolution, or a gambler risking shareholder value on a single, speculative asset?

The Viral Question: Genius or Insanity?

Here’s the million-dollar (or $13 million?) question: Why should investors trust a software company to play hedge fund with their money? Strategy’s market cap has soared, and its “Bitcoin Yield” KPI—a measure of BTC growth relative to diluted shares—hit 11% in Q1 2025. But with $8.2 billion in debt, a shrinking software business, and a $4.2 billion loss tied to BTC’s volatility, the risks are glaring. Bankruptcy rumors have haunted Strategy during every BTC bear market, and Q1 2025’s carnage proves they’re not baseless.

Saylor’s unshakable faith in Bitcoin is either a masterstroke or a recipe for disaster. If BTC skyrockets to $1 million, Strategy could indeed be a $10 trillion titan. But if it crashes, as it did in 2022 and early 2025, the company’s debt-laden balance sheet could implode, leaving shareholders with nothing.

What’s Next?

Strategy shows no signs of slowing down. Saylor’s hosting Bitcoin for Corporations 2025 in Orlando this week, preaching BTC to corporate leaders. He’s raised billions through creative financing—convertible notes, preferred stock, and equity offerings—while keeping Strategy’s BTC unencumbered. But with debt deadlines looming in 2027 and BTC’s volatility ever-present, the clock is ticking.

Investors, you’re at a crossroads. Will you ride Saylor’s Bitcoin rocket to the moon, or brace for a potential crash that could make Enron look tame? Share this update, sound off on X, and let the world know: Is Strategy’s Bitcoin bet the future of finance or a financial fiasco waiting to happen? The stakes couldn’t be higher, and the world is watching.

{kind=link}