FinTelegram has released a new Compliance Intelligence Satellite Report examining the role of French electronic money institution OuiTrust/Heuro inside the post-MiCA MEXC ecosystem. The report maps the company’s appearance in documented MEXC-related EUR deposit flows, its Hong Kong ownership layer, its crypto-facing business model and its separate position as an issuer within the MiCA Title IV e-money-token framework.

The Core Finding

FinTelegram’s new OuiTrust / Heuro Satellite Report focuses on one of the most consequential institutions appearing in the wider MEXC payment architecture: Heuro SAS, formerly Harmoniie SAS and before that Unirpay, trading as OuiTrust.

Heuro (website) is not an unregulated payment facilitator.

It is a French electronic money institution authorised by the ACPR, with e-money and payment-services capabilities and a substantial crypto-facing strategy. At the same time, FinTelegram’s documented testing placed OuiTrust/Heuro infrastructure inside a post-MiCA MEXC-related EUR deposit journey for a newly onboarded EU user.

That combination is the central issue. The question is not whether Heuro is authorised as an EMI. It is. The question is:

How does a French-regulated EMI appear at a critical fiat-entry point inside a user journey connected to an offshore exchange for which FinTelegram identified no disclosed MiCA CASP authorisation serving EU clients?

Where Heuro Appears in the MEXC Ecosystem

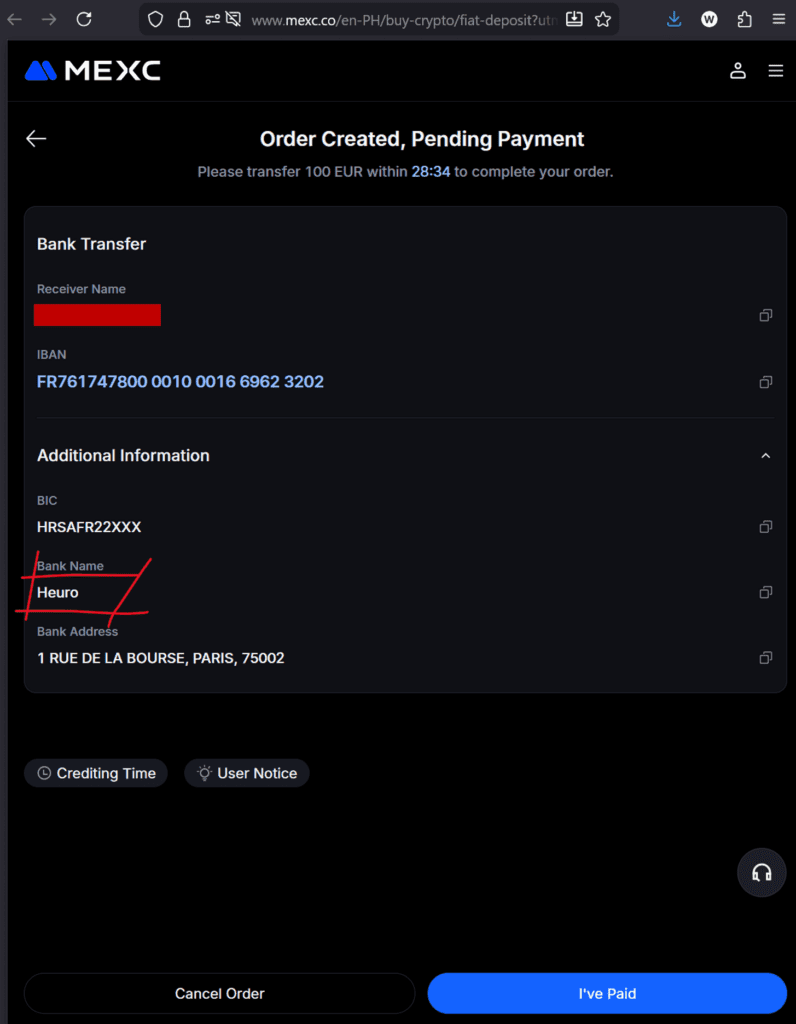

The Satellite Report builds on FinTelegram’s broader MEXC After MiCA Day One Compliance Intelligence Report. In post-deadline testing, FinTelegram documented a newly registered and fully KYC-verified EU retail user entering the MEXC environment and proceeding into a EUR bank-transfer journey. The tested flow included:

- a consent layer referring to MEXC and Harmoniie SAS dba OuiTrust;

- legal-material links connected to OuiTrust and Finetix;

- generation of an executable EUR 100 payment instruction;

- a French IBAN;

- Heuro banking details;

- BIC HRSAFR22XXX.

FinTelegram does not claim that this test independently proved the full end-to-end settlement chain or final crediting into MEXC.

That evidentiary limit matters.

But the documented appearance of a French EMI’s rails inside the funding journey of a newly onboarded EU user remains highly significant. The issue is therefore not abstract accessibility. It is the practical architecture of market access.

The Finetix Connection

The report also examines the recurring appearance of Finetix Limited S.R.L., a Romanian company that publicly describes itself as a crypto exchange and fiat-payment gateway provider. FinTelegram previously documented Finetix-related legal materials and MEXC-associated payment indicators in relevant flows. In the Heuro context, the central unresolved question is whether Finetix acts as:

- a contractual client;

- a principal;

- a payment-orchestration layer;

- a gateway;

- a payee;

- or another intermediary.

The report does not state that Heuro and Finetix are under common ownership. It does state that the precise relationship matters because customer attribution, AML/CFT responsibility, safeguarding and downstream counterparty understanding depend on it.

The Hong Kong Ownership and Group-Control Layer

The Satellite Report also examines the ownership and control architecture behind Heuro/OuiTrust. According to the French corporate records reviewed by FinTelegram, the immediate sole shareholder of Heuro SAS is EasyEuro Technology Limited, a Hong Kong company. This is an established fact at the immediate shareholder level.

The Hong Kong layer, however, is not limited to the French EMI.

UK corporate records show that EasyEuro Technology Limited also controls 75% or more of Kitakami Limited, a British company authorised by the UK Financial Conduct Authority (FCA) as an Electronic Money Institution. The result is a cross-border EasyEuro structure connecting a Hong Kong holding layer with regulated electronic-money institutions in both France and the United Kingdom.

This broader structure materially changes the ownership analysis. The relevant picture is not simply:

Hong Kong shareholder → French EMI

but rather:

EasyEuro Technology Limited (Hong Kong) → regulated UK and French financial-services entities operating within the wider OuiTrust/EasyEuro ecosystem.

The corporate records also reveal a significant personnel-continuity dimension involving Dingsheng Xue. French corporate documents reviewed by FinTelegram identify Dingsheng Xue in connection with EasyEuro Technology Limited and the shareholder governance of the French Heuro/Harmoniie entity. A 2024 filing records Xue Dingsheng as acting in the capacity of legal representative of EasyEuro Technology Limited, while the same documentation identifies the Hong Kong company as the sole shareholder of Harmoniie SAS. Separate corporate documents also record Dingsheng Xue in the sole-shareholder context of the French entity.

More recent Heuro constitutional documents continue to associate Dingsheng Xue with EasyEuro Technology Ltd in the shareholder context.

Dingsheng Xue is also an active director of the UK group company Kitakami Limited. Taken together, the public records indicate that he is not merely a peripheral director of an unrelated British subsidiary. Rather, he appears to represent a long-standing point of personnel continuity across the EasyEuro group’s Hong Kong ownership layer and its regulated European entities.

FinTelegram does not state that Dingsheng Xue is the ultimate beneficial owner of EasyEuro Technology Limited, personally controls Heuro or Kitakami, or has engaged in any misconduct. Those conclusions are not established by the public record. The compliance significance lies elsewhere. A cross-border financial-services group comprising:

- a Hong Kong controlling shareholder;

- an FCA-authorised UK EMI;

- an ACPR-authorised French EMI;

- a MiCA Title IV EMT-issuer position;

- and documented personnel continuity involving a Chinese national resident in France

creates legitimate questions about:

- ultimate beneficial ownership;

- group governance and control;

- the allocation of strategic decision-making;

- intra-group risk management;

- crypto-counterparty strategy;

- and the relationship between the Hong Kong ownership layer and the regulated European entities.

The public-source record does not fully resolve the ultimate beneficial ownership of EasyEuro Technology Limited. Heuro has reportedly stated elsewhere that its UBOs are French-resident natural persons and are duly registered within the relevant French beneficial-ownership framework. That position may be compatible with the documented Hong Kong intermediate holding structure. But the newly identified role of Dingsheng Xue makes the ownership and governance picture materially more significant than a simple offshore-shareholder disclosure.

The core question is therefore no longer only who formally owns Heuro SAS.

It is:

Who ultimately controls the EasyEuro group, how is decision-making allocated across Hong Kong, the UK and France, and what role does Dingsheng Xue play within that architecture?

These questions become particularly relevant in light of the group’s regulated payment activities, HEURO’s MiCA Title IV EMT position and FinTelegram’s documented MEXC-related payment-flow evidence.

Heuro Is Also a Token Issuer

The second major reason why the case matters is Heuro’s own position inside the crypto economy.

HEURO SAS is not only an EMI.

It is also positioned within the MiCA Title IV framework for e-money-token issuers, with HEURO connected to the company’s regulated e-money-token activity. This distinction is essential.

A MiCA EMT issuer is not the same as a MiCA CASP.

HEURO’s Title IV position does not authorise MEXC.

It does not transfer CASP rights to a third-party exchange.

And it does not cure or substitute for the MiCA authorisation status of another platform.

But it changes the supervisory significance of the case.

This is not a situation in which an obscure payment processor happens to touch a crypto flow.

It involves a French-regulated EMI that is itself embedded in the EU’s post-MiCA token framework and whose declared strategy is connected to web3 payments, fiat on/off-ramping and exchange-related settlement.

Why the HEURO Token Matters

The report also examines the HEURO token. Heuro has positioned HEURO as a euro-denominated e-money token and as part of a broader exchange and settlement strategy. That creates an additional line of inquiry.

Where a regulated EMT issuer promotes settlement relationships with major crypto-market participants, the quality of its:

- source-of-funds controls;

- exchange-counterparty due diligence;

- reserve-integrity processes;

- transaction monitoring;

- and segregation between different payment and settlement channels

becomes highly relevant.

FinTelegram does not state that MEXC-related funds entered HEURO reserves. No such finding is made. The question is narrower:

How does a regulated EMT issuer ensure that exchange-facing settlement activity remains segregated from high-risk flows connected to platforms without disclosed EU CASP authorisation?

That is a legitimate compliance and supervisory question.

The MEXC Link Raises the Stakes

The relevance of Heuro’s appearance cannot be separated from MEXC’s broader regulatory record. The MEXC master report documents:

- post-deadline EU onboarding;

- no disclosed MEXC MiCA CASP authorisation for EU clients;

- multiple public regulatory warnings;

- and the Seychelles FSA’s identification of the MEXC operator in an unlicensed-operations context.

Against that background, the appearance of regulated European infrastructure becomes particularly important.

For a bank, EMI, PSP, CASP or acquirer, the central questions include:

- Was MEXC’s authorisation status assessed?

- Was its regulatory history reviewed?

- Was Finetix risk-rated?

- Who is the legal customer?

- Who receives the funds?

- Who controls downstream settlement?

- Which institution owns the AML/CFT responsibility at each step?

These are not theoretical questions.

They determine whether the post-MiCA perimeter works in practice.

The Paytend Lesson

The Satellite Report also places the Heuro findings in the historical context of changing MEXC-related payment rails.

Earlier FinTelegram investigations documented other regulated intermediaries around MEXC-linked flows, including Paytend Europe UAB, whose Lithuanian EMI licence was later revoked following serious AML/CFT, monitoring and governance findings by the Bank of Lithuania.

FinTelegram does not claim that MEXC was the unnamed high-risk customer referenced in that enforcement case. No causal link between MEXC-related flows and Paytend’s licence revocation is established. The relevance is structural:

regulated payment institutions can face severe consequences where their understanding, monitoring and governance of high-risk flows are found inadequate.

FinTelegram Assessment

The OuiTrust/Heuro case is analytically significant precisely because the institution is regulated. Its stronger regulatory standing does not make the MEXC-related evidence irrelevant. It makes the questions more important. FinTelegram’s assessment is deliberately narrow but firm:

The documented appearance of OuiTrust/Heuro infrastructure inside MEXC-related EU payment journeys warrants enhanced regulatory and counterparty scrutiny. The significance of the case is increased — not reduced — by Heuro’s status as an ACPR-authorised EMI and by HEURO SAS’s position within the MiCA Title IV EMT framework.

This is not an allegation of criminal conduct. It is a compliance question about where a regulated French financial institution sits inside a high-risk offshore-exchange ecosystem. And it is a question that can be answered with documents.

Download the Satellite Report

FinTelegram is making the full OuiTrust / Heuro Satellite Report available for download.

The report contains:

- legal and regulatory identity;

- ownership structure;

- key persons;

- MEXC-related payment evidence;

- Finetix connections;

- HEURO token analysis;

- MiCA Title IV perimeter analysis;

- risk assessment;

- right-of-reply framework;

- and detailed questions to management and supervisors.

Download the OurTrust / Heuro Satellite Report here.

Whistleblower Call

FinTelegram invites current and former employees, compliance officers, MLROs, contractors, banking partners, PSPs, CASPs, acquirers, users and counterparties with information about. Help us map the infrastructure behind the market.

FinTelegram’s risk assessments are editorial compliance classifications and not findings by a court or regulator. The report does not allege criminal conduct by any named entity or person. All named parties are invited to provide corrections, documents and statements for incorporation into future versions.

{kind=link}