FinTelegram’s Rail Atlas reviews show a recurring pattern in offshore casino payment flows: the player starts a deposit at an online casino, but the bank-facing payment screen names a payment processor — such as CAPITOLIO INC. or Domus Payment Solutions — as the payee. In card payments, players may at least have chargeback routes. In Pay-by-Bank and open-banking account-to-account rails, those protections are materially weaker. This architecture creates a serious compliance and consumer-protection problem: if the casino operator disappears from the payment screen, how can players enforce refund claims against illegally or unauthorised gambling operators?

2-Minutes Briefing

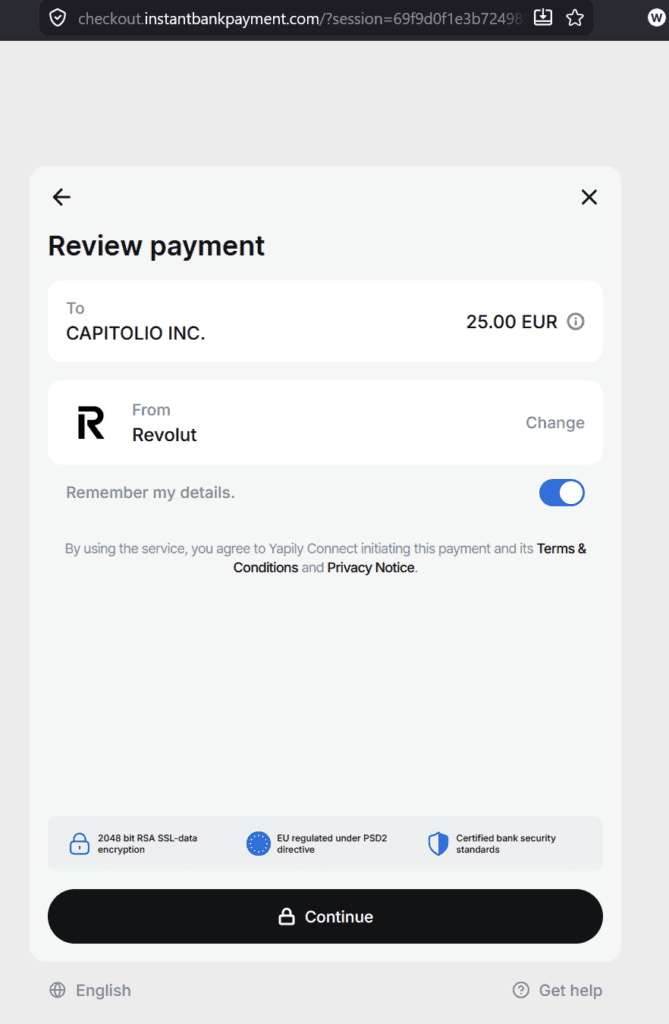

FinTelegram’s recent Payment Rail Atlas reviews of offshore casino cashiers, including 1Go Casino and Winnita, have identified a recurring payment architecture: the player initiates what is economically a casino deposit, but the bank-facing payment screen names a payment processor or infrastructure company as the payee rather than the casino operator.

In the 1Go Casino review, CAPITOLIO INC. appeared as payee in a Revolut/Yapily open-banking rail, while Domus Payment Solutions appeared as payee in a separate Pay-by-Bank rail.

In the Winnita review, FinTelegram again found Domus Payment Solutions as named payee in a Pay-by-Bank flow involving InstantBankPayment, Token GmbH/Token.io, and Revolut.

Read our Winnita payment rail review here.

This is not merely a technical detail. In card payments, consumers may have card-scheme chargeback routes. Open-banking payments are different. They are account-to-account transfers initiated from the customer’s bank account, and industry sources describe them as bypassing card-network rails with no card-scheme chargeback mechanism; disputes depend on merchant refund policies and any protections offered by the payment-initiation provider.

The timing matters. In Case C-440/23, the Court of Justice of the European Union held that EU law does not prevent a Member State from prohibiting online gambling services even where the operator holds a licence in another Member State, and the case expressly concerned recovery of lost stakes and abuse-of-law arguments. In Case C-77/24 Wunner, the CJEU addressed cross-border claims linked to unlicensed online gambling and confirmed the relevance of the player’s country of participation/residence for determining where the damage occurred.

Against that legal backdrop, processor-as-payee architectures become especially problematic. If the player cannot clearly identify the actual casino operator or ultimate gambling beneficiary from the payment flow, recovery claims may become practically difficult, even where national law gives the player a right to reclaim deposits or losses from an unauthorised gambling operator.

Key Findings

- FinTelegram has observed processor-as-payee structures in several casino rails. In 1Go Casino, CAPITOLIO INC. and Domus Payment Solutions appeared in different rails; in Winnita, Domus Payment Solutions appeared as payee in a Pay-by-Bank rail.

- The casino operator may disappear from the bank-facing payment flow. The player sees the casino cashier at the start, but the bank or open-banking authorisation screen may show a processor, MSB, wallet platform, or collection entity.

- Processor-as-payee is not automatically unlawful. A processor may lawfully appear as merchant of record, payment facilitator, collection agent, or technical payee. But in gambling-origin payments, this is only defensible if the underlying merchant, payment purpose, processor role, refund route, and licensing status are clearly disclosed and properly monitored.

- The risk is payment-purpose dilution. The payment starts as a casino deposit but may arrive at the bank layer as an ordinary account-to-account transfer to a payment infrastructure company.

- Open-banking rails weaken card-style recovery options. PXP’s open-banking explainer states that open-banking payments bypass card networks and have no card-scheme chargeback mechanism; disputes fall to merchant refund policies and any PISP protections.

- CJEU case law increases the importance of payment transparency. Case C-440/23 confirms that EU law does not automatically shield cross-border operators from national gambling restrictions and restitution consequences; Case C-77/24 Wunner strengthens the relevance of the player’s country for claims linked to unlicensed online gambling.

- Opaque payment architecture can impair player protection. If the bank statement shows CAPITOLIO INC. or Domus Payment Solutions rather than the casino operator, the player may face practical obstacles in proving the link between deposits and the illegal or unauthorised gambling service.

The Observed Architecture

Typical Processor-as-Payee Casino Flow

| Layer | What the Player Sees | What FinTelegram Observed | Compliance Concern |

|---|---|---|---|

| 1 | Casino cashier | 1Go Casino / Winnita deposit page | Gambling purpose is clear at the start. |

| 2 | Gateway | InstantBankPayment, BillBlend, SegoPay, Tryzto, Token.io or similar | The casino brand begins to disappear behind intermediaries. |

| 3 | Open-banking / PISP layer | Yapily, Token.io, Bridge/SaltEdge or similar | A regulated or semi-regulated chokepoint initiates/supports the A2A payment. |

| 4 | Bank authentication | Revolut, Wise or another bank | Player authenticates a push payment. |

| 5 | Payee screen | CAPITOLIO INC. or Domus Payment Solutions | Non-casino payee appears instead of the operator. |

| 6 | Economic destination | Casino account / player balance credited | Ultimate gambling beneficiary may not be transparent. |

The central issue is not that processors exist. Payment processors are normal in digital commerce. The issue is merchant substitution at the visibility layer: the consumer-facing merchant is an offshore casino, while the bank-facing payee is a processor.

Is It Allowed To Show a Processor Instead of the Casino Operator?

The Compliance Answer

A processor may be shown as payee in a lawful merchant-of-record, payment facilitator, collection-agent, or technical on-ramp model. But where the player is not clearly informed that the processor receives funds for, or on behalf of, the casino — and where the bank-facing transaction no longer identifies the gambling merchant or the gambling purpose — the structure creates serious transparency, AML, payment-compliance, and consumer-protection risk.

In other words: processor-as-payee is lawful in principle, but high-risk in practice when used for casino-origin deposits.

A compliant model would need to answer the basic questions:

- Who is the actual gambling operator?

- Is the operator licensed in the player’s jurisdiction?

- Is the processor collecting funds for that operator?

- Does the player understand whom they are paying?

- Does the bank or PISP receive the gambling context?

- Does the player have a clear refund or complaint route?

- Is the payment purpose preserved through the rail?

If those questions cannot be answered, the model becomes a transparency problem.

Why It May Breach Consumer Protection Principles

EU consumer law is built around clear, timely and understandable information. Consumers must know the identity of the trader and the essential characteristics of the service before making a transactional decision. The Unfair Commercial Practices Directive treats omissions of material information as potentially misleading where the average consumer needs that information to make an informed decision.

In a casino deposit context, the identity of the casino operator and the fact that the payment funds gambling activity are material. If the consumer-facing casino disappears from the payment screen and is replaced by a processor name, the player may not know:

- who actually operates the gambling service;

- who receives or controls the funds;

- who is responsible for refunds;

- where to direct a restitution claim;

- whether the transaction is classified as gambling or as an ordinary transfer.

That does not automatically prove a legal breach in every case. But it creates a strong misleading-omission and transparency risk, especially where the casino is not authorised in the player’s jurisdiction.

Payment Compliance Analysis

1. Payee vs. Ultimate Merchant

Under payment law, the payee shown in an A2A payment may be the entity designated to receive funds. In platform models, that entity may be a processor or collection agent. But from a compliance perspective, the ultimate merchant and economic purpose cannot disappear.

In gambling, this is critical. Banks, PISPs, PSPs and MSBs must know whether they are facilitating gambling-related transactions, particularly where the underlying operator targets jurisdictions requiring local authorisation.

If CAPITOLIO INC., Domus Payment Solutions, or similar entities appear as payees for casino-origin deposits, their role should be transparent: Are they merchant of record, agent, processor, settlement provider, on-ramp provider, or simply a technical collection account?

2. AML/KYB Risk

Casino-origin payments are high-risk because gambling is a regulated sector and can involve fraud, chargeback abuse, money-laundering typologies, affordability concerns, and consumer-harm issues. If a processor receives funds from players, its KYB file should show:

- the upstream casino operator;

- the contractual counterparty;

- the target jurisdictions;

- licensing analysis;

- merchant-category classification;

- transaction-monitoring logic;

- complaint and refund handling;

- whether funds are settled onward to the casino, affiliate, wallet, crypto rail, or another processor.

Without those controls, the processor-as-payee model becomes a collection layer for unauthorised gambling.

3. Payment-Purpose Dilution

FinTelegram uses the term payment-purpose dilution for the process by which a transaction that starts as a casino deposit appears downstream as an ordinary transfer to a payment processor.

That is the key danger. Banks and PISPs may screen the visible payee and payment reference but not the upstream gambling context. In that case, the risk model sees a processor; the economic reality is an offshore casino deposit.

Consumer and Player Protection Impact

No Card Chargeback Layer

Card payments are embedded in card-scheme dispute and chargeback frameworks. Pay-by-Bank and open-banking payments are account-to-account push payments authenticated by the payer. They do not use card networks, and PXP describes the absence of card-scheme chargebacks as one of the key differences and risk trade-offs of open banking.

For a casino player, this creates a harsh combination:

- the payment is difficult to reverse;

- the bank statement may show a processor, not the casino;

- the casino operator may be offshore and difficult to sue;

- the processor may deny responsibility as “technical infrastructure”;

- the bank may argue that the customer authorised the transfer.

This weakens practical enforcement of player rights.

Refund Claims After Recent CJEU Case Law

The CJEU’s recent gambling jurisprudence makes this problem more important.

In C-440/23 European Lotto and Betting and Deutsche Lotto- und Sportwetten, the Court’s judgment concerned national authorisation requirements for online games of chance, overriding reasons in the public interest, online slot machines, secondary lotteries, recovery of lost stakes, and abuse of law. The Court’s press release summarises the outcome as recognising that a consumer may bring a claim for restitution of lost stakes against operators established in another Member State, and that EU law does not prevent Member States from maintaining authorisation requirements in the public interest.

This should be stated precisely: the CJEU did not create a blanket EU-wide automatic refund right for every player in every case. Rather, it confirmed that EU law does not prevent Member States from attaching civil-law consequences — including nullity and restitution claims — to online gambling offered without the required national authorisation.

In C-77/24 Wunner, the Court addressed cross-border liability claims linked to unlicensed online gambling and the country where damage occurs. The case listing describes the issue as the country from which the player participates, and legal commentary summarises the judgment as confirming that players may generally rely on the law of their habitual-residence Member State when pursuing claims linked to foreign operators lacking the required local licence.

Together, these cases make payment transparency crucial. If national law gives the player a restitution route, the payment evidence must allow the player to prove who received funds, for whose benefit, and for which gambling operator. Processor-as-payee rails can obstruct that proof.

The Practical Enforcement Problem

The player’s legal position may be strong on paper but weak in practice.

| Player Needs To Prove | What Processor-as-Payee Rails May Show |

|---|---|

| The payment funded an illegal or unauthorised casino deposit | Bank screen shows a transfer to CAPITOLIO INC. or Domus Payment Solutions. |

| The casino operator received the funds | Operator is not shown as payee. |

| The casino lacked required local authorisation | Payment record does not identify the gambling operator. |

| The claim should be directed to the operator | The visible payee may say it was only a processor or on-ramp. |

| The bank should treat it as gambling-related | Bank may classify it as ordinary A2A transfer to a corporate payee. |

| The transaction can be disputed | No card-scheme chargeback layer exists. |

This is the consumer-protection conflict:

The law may give the player a refund claim.

The payment architecture may make that claim difficult to enforce.

Compliance Classification

| Risk Area | Assessment |

|---|---|

| Payment transparency | High risk if the casino operator and gambling purpose are not clearly disclosed. |

| Consumer protection | High risk where players cannot identify the trader/operator or enforce refund claims. |

| AML/KYB | High risk where processors collect funds for offshore gambling merchants. |

| Gambling compliance | High risk where casinos target jurisdictions without local authorisation. |

| Bank monitoring | Impaired if the visible beneficiary is a processor rather than the gambling operator. |

| Chargeback / dispute rights | Weaker than card rails because A2A payments lack universal card-style chargebacks. |

| Litigation / restitution | Player claims may be obstructed by lack of clear payment evidence linking deposits to the casino operator. |

| Regulatory reporting | Weak if processors and PISPs do not preserve upstream merchant and payment-purpose data. |

FinTelegram Position

Processor-as-payee architecture is not automatically illegal. But in offshore casino rails it is a major red flag.

A compliant model would require at least:

- clear disclosure of the casino operator;

- clear disclosure that the processor receives funds for or on behalf of the casino;

- clear payment purpose shown to the player and, where possible, to the bank/PISP;

- documented merchant onboarding and KYB;

- evidence that the casino is authorised in the target jurisdiction;

- effective blocking of jurisdictions where the casino is not licensed;

- refund and complaint routes identifying the actual merchant and responsible processor;

- transaction monitoring that preserves the upstream gambling context;

- audit trails showing how funds move from processor payee to ultimate casino beneficiary.

Without these safeguards, the architecture may amount to practical concealment of the true merchant and payment purpose.

Questions for Processors, PISPs and Banks

FinTelegram believes the following questions should be asked whenever a processor appears as payee in a casino-origin open-banking rail:

- Who is the actual gambling operator behind the deposit?

- Does the processor receive funds for or on behalf of that operator?

- Is the operator licensed in the player’s jurisdiction?

- What merchant category and risk classification is used?

- What does the payer’s bank see — processor only, or casino context?

- What does the PISP see — processor only, or upstream merchant context?

- Is the player told that the processor is collecting funds for the casino?

- Who handles refund and restitution claims?

- Can the processor provide an audit trail from player deposit to casino settlement?

- Are unauthorised gambling jurisdictions blocked?

If the answer to these questions is unclear, the rail should be treated as high-risk.

Conclusion

The processor-as-payee model observed in 1Go Casino and Winnita shows a serious weakness in modern open-banking casino payments.

The player thinks he is depositing into a casino. The bank-facing screen may show a payment processor. The card chargeback layer is absent. The underlying casino operator may be offshore, opaque, or not locally licensed. Yet recent CJEU case law confirms that EU law does not prevent Member States from attaching civil-law consequences, including restitution claims, to gambling services offered without required national authorisation.

That creates the core consumer-protection conflict:

The law may give the player a refund claim.

The payment architecture may make that claim difficult to enforce.

For payment processors, PISPs, banks, and gambling regulators, this is no longer theoretical. If processors such as CAPITOLIO INC. or Domus Payment Solutions appear as named payees in casino-origin Pay-by-Bank or open-banking rails, they should be expected to explain exactly whose funds they collect, for which merchant, under which licence, in which jurisdiction, and with what disclosure to the player.

Open banking is a payment innovation. It must not become an opacity layer for unauthorised offshore gambling.

FinTelegram will continue to document these rails because payment transparency is now central to player protection.

Call for Information

FinTelegram invites casino players, payment insiders, PSP employees, compliance officers, banking staff, and former employees of offshore gambling operators to provide information about processor-as-payee casino rails.

We are particularly interested in payment confirmations, bank screenshots, open-banking consent screens, payee names, merchant descriptors, refund correspondence, casino KYC files, PSP onboarding documents, settlement records, and internal compliance communications involving CAPITOLIO INC., Domus Payment Solutions, InstantBankPayment, Token GmbH/Token.io, Yapily, SaltEdge/Bridge, Revolut, and related casino payment flows.

Information can be submitted confidentially via Whistle42.

{kind=link}