FinTelegram’s latest Revolut Rail Atlas review of 1Go Casino shows how a player-facing offshore casino cashier can route deposits through a multi-layered payment stack before reaching a regulated open-banking interface. In the tested Revolut flow, the user journey moved from 1Go Casino through BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily Connect UAB, and finally oba.revolut.com, where the user was asked to authorise Yapily Connect UAB. The visible payee was not 1Go Casino or Galaktika N.V., but CAPITOLIO INC. Other 1Go rails showed Domus Payment Solutions and Galaktika N.V. as payees. The case illustrates the structural weakness FinTelegram’s Revolut Rail Atlas is documenting: a casino deposit can be transformed through several routing layers into an open-banking payment where the regulated chokepoint appears only at the final authorisation stage.

Key Findings

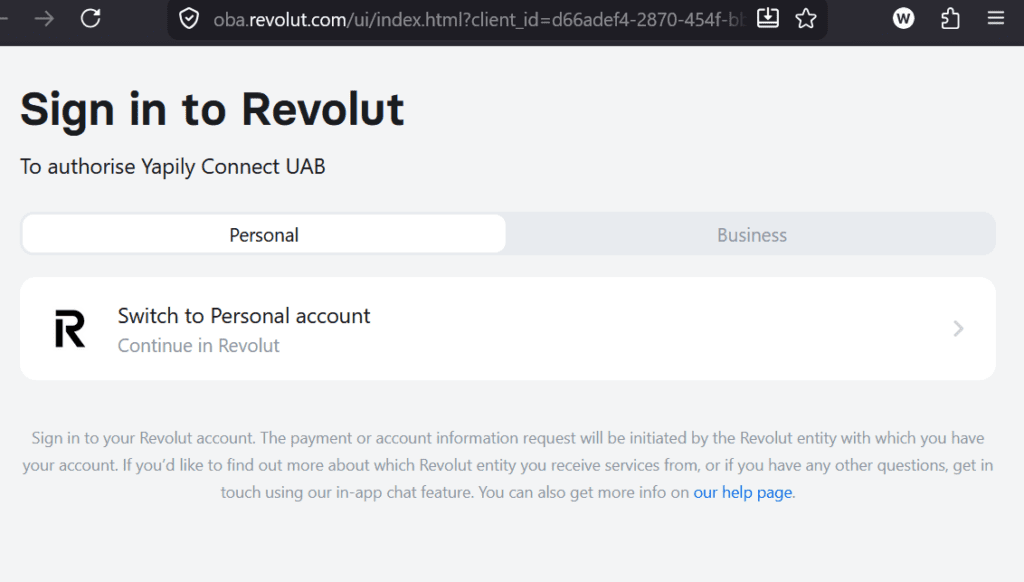

- 1Go Casino offered a dedicated Revolut deposit rail. The tested flow led to oba.revolut.com, where the user was asked to sign in to Revolut to authorise Yapily Connect UAB.

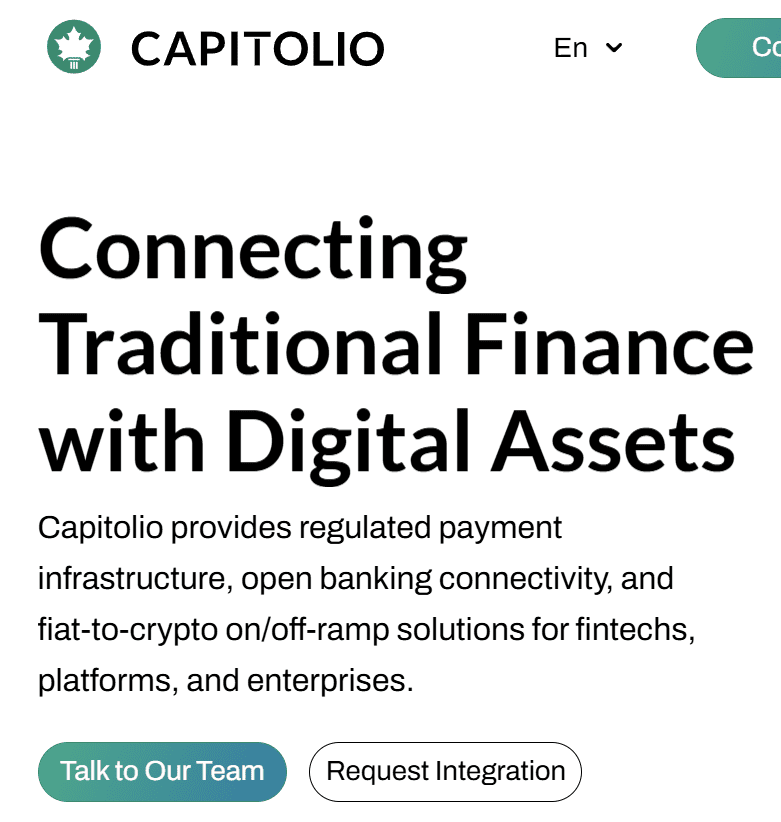

- The Revolut rail showed CAPITOLIO INC. as payee. In the payment-review screen, the beneficiary for the €25 Revolut payment was CAPITOLIO INC., not 1Go Casino and not Galaktika N.V.

- The observed Revolut gateway chain was multi-layered. The tested sequence included

pay.billblend.com/checkout,tx.segopay.com/payment,tryzto.com/ct/check,checkout.instantbankpayment.com, and finallyoba.revolut.com. - Yapily Connect UAB appeared at the regulated open-banking layer. At the final stage, the Revolut page stated that the user was signing in to Revolut “to authorise Yapily Connect UAB.”

- BillBlend and SegoPay appeared as upstream routing layers. BillBlend was the first visible payment gateway in the Revolut sequence, followed by SegoPay and then additional routing pages.

- InstantBankPayment was used in more than one rail. The same

checkout.instantbankpayment.cominfrastructure appeared both in the Revolut flow and in a separate Pay by Bank route with bank selection. - Different payment rails produced different payees. The screenshots show CAPITOLIO INC. in the Revolut/Yapily rail, Domus Payment Solutions in one Pay by Bank route, and Galaktika N.V. in the MiFinity route.

- The cashier also offered MiFinity, ByBit, direct crypto, and two Pay by Bank options. This indicates a resilient multi-rail deposit architecture rather than a single transparent payment setup.

Evidence Reviewed

FinTelegram reviewed the following screenshots and payment-flow evidence from the May 5, 2026 test:

- 1Go Casino cashier screenshot showing deposit options for MiFinity, Crypto Currency, ByBit, Revolut, and two Pay by Bank rails.

- ByBit gateway screenshot hosted under

nczds3g4.fxcamyjxts.com/132882/, showing a QR-code/app-based payment page for $29.23 and instructions to pay via the ByBit app. - InstantBankPayment / Wise review screen showing a €25 payment from Wise to Domus Payment Solutions.

- MiFinity payment screen showing a €25 deposit to Galaktika N.V.

- Direct IBAN Pay by Bank screen requiring the user to enter an IBAN/account number. During FinTelegram’s review, this payment route did not work.

- InstantBankPayment bank-selection screen listing available banks in Italy, including Wise, Revolut, N26, PostePay, ING, UniCredit, Intesa Sanpaolo, and others.

- InstantBankPayment Revolut transition screen instructing the user to go to Revolut to complete the payment.

- Revolut/Yapily payment-review screen showing a €25 payment from Revolut to CAPITOLIO INC.

- Revolut OBA authorisation screen at

oba.revolut.com, stating: “Sign in to Revolut — To authorise Yapily Connect UAB.”

The 1Go Casino Cashier: A Multi-Rail Deposit Architecture

At the user-interface level, 1Go Casino presents a standard offshore casino cashier: account currency in EUR, deposit tiles, bonus-code input, and minimum/maximum deposit amounts. However, the screenshots reveal much more than a simple payment menu.

The cashier functions as a payment rail selector. Each deposit method routes the user into a different operational and legal environment. This is typical of high-risk offshore casino payment architecture. If one rail fails, is blocked, or becomes unavailable for a specific user, jurisdiction, or bank, the cashier can offer alternatives. From a compliance perspective, the risk is not only the existence of multiple payment methods. The risk is that each rail may show a different payee and may conceal the actual economic purpose of the transaction behind intermediary processors.

Condensed Rail View

| Rail | Observed Path | Visible Payee / Beneficiary | Main Risk Signal |

|---|---|---|---|

| Revolut / Yapily rail | 1Go → BillBlend → SegoPay → Tryzto → InstantBankPayment → Yapily Connect UAB → Revolut OBA | CAPITOLIO INC. | Casino deposit transformed into open-banking payment with non-casino payee. |

| Pay by Bank / Wise rail | 1Go → InstantBankPayment → bank-selection screen → Wise | Domus Payment Solutions | Casino deposit routed to corporate payee not visibly identified as the casino. |

| MiFinity rail | 1Go → MiFinity | Galaktika N.V. | Wallet rail shows operator-linked payee, unlike the other bank rails. |

| ByBit / crypto rail | 1Go → ByBit-branded QR/payment page → crypto app flow | Not confirmed from screenshot | Crypto/app rail may shift casino funding outside standard bank/card monitoring. |

| Direct IBAN Pay by Bank rail | 1Go → IBAN/account-number input form | Not confirmed | Route failed during review; still indicates additional fallback payment architecture. |

The Revolut Rail: Casino Deposit Becomes Open-Banking Authorisation

The most important finding for the Revolut Rail Atlas is the tested Revolut flow. The sequence observed by FinTelegram was:

1Go Casino cashier

→ pay.billblend.com/checkout

→ tx.segopay.com/payment

→ tryzto.com/ct/check

→ checkout.instantbankpayment.com

→ oba.revolut.com

→ Yapily Connect UAB authorisation

At the final stage, the Revolut page did not simply show a casino payment. It displayed the message: “Sign in to Revolut — To authorise Yapily Connect UAB.”

This confirms that the Revolut payment was being initiated through an open-banking layer involving Yapily Connect UAB. In other words, 1Go’s Revolut cashier button ultimately led to a regulated payment-initiation authorisation flow.

The issue is not merely that 1Go Casino offers Revolut as a payment option. The issue is that a player-facing casino deposit is transformed through several routing layers into an open-banking payment where the regulated provider appears only at the final authorisation stage. That is precisely the structural weakness FinTelegram’s Rail Atlas is documenting.

The Payee Problem: CAPITOLIO Instead of the Casino Brand

The Revolut/Yapily payment-review screen did not show 1Go Casino, Galaktika N.V., BillBlend, SegoPay, or InstantBankPayment as the beneficiary. It showed CAPITOLIO INC. as the payee. This is not a minor technical detail. In the tested transaction flow, Capitolio appeared as the entity designated to receive player funds originating from the 1Go Casino cashier.

CAPITOLIO presents itself as a Canadian-incorporated payment and digital-asset infrastructure provider registered with FINTRAC as a Money Services Business under registration number M24928320.

Capitolio’s website describes services including open-banking payments, account-to-account transactions, fiat-to-crypto on/off-ramp solutions, payout infrastructure, and digital-asset infrastructure. It also lists “Gaming & Digital Economy” among the sectors it serves. This makes its appearance as the visible payee in the 1Go Casino Revolut/Yapily flow especially relevant: the user begins in a casino cashier, but the open-banking payment-review screen shows a Canadian MSB/payment-infrastructure entity rather than the casino brand or the apparent Curaçao operator.

That makes Capitolio an apparent collection/payee entity within the casino payment rail. Whether Capitolio acted as merchant of record, payment agent, settlement intermediary, crypto on/off-ramp provider, or payment processor for another party requires further clarification. However, the payment screen indicates that Capitolio was the visible recipient of the funds at the bank/open-banking layer. As such, Capitolio’s role is central to the compliance analysis.

The key question is therefore not merely whether 1Go Casino offered a Revolut rail. The question is why a player deposit initiated inside an offshore casino cashier resulted in an open-banking payment to CAPITOLIO INC., a non-casino-branded entity.

BillBlend, SegoPay and the High-Risk Routing Layer

The first visible payment gateway in the Revolut sequence was: pay.billblend.com/checkout.

BillBlend appears as an upstream payment gateway in the tested 1Go Revolut flow. FinTelegram notes that BillBlend presents itself as a payment operator serving high-risk and online-gaming merchants. This makes its appearance in the 1Go payment sequence relevant for compliance analysis.

The next visible stage was: tx.segopay.com/payment

FinTelegram has previously identified SegoPay in connection with high-risk casino payment flows. SegoPay is currently rated “black” on RatEx42.

In the 1Go case, the relevant point is not simply the presence of BillBlend or SegoPay as individual entities. The relevant point is their role in the routing chain. They appear before the payment flow reaches additional gateway layers and finally the regulated open-banking interface.

That creates a layered structure in which the original casino context may be diluted before the transaction reaches the bank-facing authorisation screen.

Opaque Gateway Layer & Domus Payment Solutions

After BillBlend and SegoPay, the tested Revolut flow passed through: tryzto.com/ct/check and then checkout.instantbankpayment.com

FinTelegram treats these as opaque or unbranded gateway layers in the tested user journey. The screenshots do not show a clear consumer-facing disclosure at those stages explaining the full merchant chain, the responsible acquiring/payment entity, or the relationship between the casino, the displayed payee, and the payment-initiation provider.

InstantBankPayment was particularly important because it appeared in more than one 1Go rail.

In the tested InstantBankPayment/Wise Pay by Bank route, the payment-review screen showed Domus Payment Solutions as the beneficiary of a payment initiated from the 1Go Casino cashier. Public information links Domus Payment Solutions LTD to the DomusPay financial platform in Canada, with wallet/account services, payment processing, currency exchange, and fiat/crypto functionality. Notably, a FINTRAC-related 2023 notice listed Domus Payment Solutions Ltd. and MSB registration number M22067268 among registrations revoked during the 2022–2023 Q4 period.

This makes Domus’s appearance as the payee in a casino deposit flow a relevant compliance question for InstantBankPayment, Wise, and the upstream casino-payment gateways.

MiFinity Rail: Galaktika N.V. Appears as Payee

The MiFinity route produced a different payee result: Galaktika N.V. This is notable because Galaktika N.V. appears to be the operator associated with 1Go Casino in public casino-review listings. In other words, the MiFinity rail at least displayed a payee that appears directly connected to the casino operation.

The contrast matters. In the tested 1Go cashier:

- the MiFinity rail showed Galaktika N.V.;

- the Pay by Bank / Wise rail showed Domus Payment Solutions;

- the Revolut / Yapily rail showed CAPITOLIO INC.

This is a strong indicator of a multi-payee casino deposit structure. It raises the question of which entity is the true merchant of record for each rail, who performed the merchant due diligence, and whether the payment purpose was disclosed consistently to banks and regulated payment providers.

Compliance Analysis

1. Merchant Opacity

The most important issue is merchant opacity. The same casino cashier produced at least three different visible payees:

- CAPITOLIO INC. in the Revolut/Yapily rail;

- Domus Payment Solutions in the InstantBankPayment/Wise rail;

- Galaktika N.V. in the MiFinity rail.

This makes it difficult for a user, bank, regulator, or payment-initiation provider to understand who is actually receiving the money and whether the payment is properly classified as a casino deposit.

2. Payment-Purpose Dilution

The original economic purpose is clear at the beginning of the journey: the user is depositing money into a casino account. But by the time the user reaches the bank/open-banking interface, the visible payee may be a different company. This creates payment-purpose dilution.

The central question is whether the regulated institutions in the chain saw the payment as a gambling transaction or merely as a transfer to a corporate beneficiary.

3. Open-Banking Misuse Risk

Open banking was designed to enable efficient, user-authorised bank-account payments. In high-risk environments, however, it can become a chargeback-resistant casino deposit rail.

Unlike card payments, account-to-account open-banking payments may offer fewer recovery options for consumers. If such payments are routed through intermediary merchants or opaque gateways, the consumer may struggle to understand whom they actually paid and on what legal basis.

4. Regulated Chokepoints

The final Revolut screen shows Yapily Connect UAB as the authorised payment-initiation provider. Revolut appears as the user’s bank/open-banking interface. These are regulated chokepoints.

This does not prove that Revolut or Yapily knowingly facilitated unlawful gambling. But it does mean that regulated entities appeared at the end of a payment chain that began inside an offshore casino cashier and passed through several intermediate gateways.

That is precisely why regulators should examine whether existing merchant-monitoring, transaction-monitoring, and payment-purpose controls are sufficient.

5. Multi-Rail Resilience

1Go Casino appears to operate a resilient cashier architecture with multiple fallback rails: MiFinity, crypto, ByBit, Revolut, Pay by Bank with bank selection, and direct IBAN-based Pay by Bank.

This is a common feature of offshore casino payment infrastructure. The cashier does not depend on one regulated acquiring channel. It can shift users between wallets, bank-account payments, crypto rails, and app-based payment flows.

Conclusion

The 1Go Casino review is not just another entry in FinTelegram’s Revolut Rail Atlas. It is a textbook example of how offshore casino payment infrastructure can turn a simple player deposit into a multi-layered, multi-payee, open-banking transaction that obscures the true economic purpose of the payment.

The issue is not merely that 1Go Casino offers Revolut as a payment option. The issue is that a player-facing casino deposit is routed through a chain of gateways — BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily Connect UAB, and Revolut OBA — before landing on a payment-review screen where the visible beneficiary is not the casino brand, not the apparent Curaçao operator Galaktika N.V., but CAPITOLIO INC.

This matters. Publicly available information indicates that CAPITOLIO INC. presents itself as a Canadian MSB and payment/digital-asset infrastructure provider. In the tested Revolut/Yapily flow, however, Capitolio appeared as the visible recipient of player funds originating from the 1Go Casino cashier. That makes Capitolio an apparent collection/payee entity in the casino deposit rail. Whether Capitolio acted as merchant of record, payment agent, settlement intermediary, crypto on/off-ramp provider, or processor for another upstream party requires clarification — but its appearance as the beneficiary is not a neutral technical detail. It is central to the compliance analysis.

The same applies to Domus Payment Solutions, which appeared as the payee in the tested InstantBankPayment/Wise Pay by Bank route. Public information links Domus Payment Solutions to a Canadian payment and wallet platform, while FINTRAC-related notices indicate that its MSB registration was revoked in 2023. If a player starts inside the 1Go Casino cashier and ends up paying Domus Payment Solutions through a Pay by Bank flow, regulators should ask who onboarded Domus, who controls the merchant relationship, and whether the transaction was monitored as a gambling deposit or merely as an ordinary corporate transfer.

This is the structural risk: by the time the transaction reaches the regulated banking interface, the visible payee may no longer be the casino brand. The bank may see CAPITOLIO INC. or Domus Payment Solutions. The player, however, knows the money was deposited into 1Go Casino.

For regulators, banks, open-banking providers, and payment institutions, the question is no longer theoretical:

Can their systems detect that these are casino deposits when the transaction has been laundered through gateway layers and re-labelled under non-casino payee names?

If the answer is no, then open banking is being used not merely as a payment innovation, but as a high-risk offshore casino funding rail. FinTelegram will continue mapping these rails, identifying the regulated chokepoints, and exposing the payment agents, processors, gateways, and beneficiary entities that en

Whistleblower Call

FinTelegram invites players, former employees, payment insiders, compliance officers, PSP staff, and open-banking specialists to provide further information about:

1Go Casino, Galaktika N.V., CAPITOLIO INC., Domus Payment Solutions, BillBlend, Fin&Pay Partners OÜ, SegoPay, Tryzto, InstantBankPayment, Yapily Connect UAB, Revolut OBA, MiFinity, ByBit, and related casino payment flows.

Relevant evidence includes screenshots, payment confirmations, URLs, gateway redirects, merchant descriptors, bank statements, GDPR responses, KYC files, onboarding documents, and internal compliance correspondence.

Information can be submitted confidentially via Whistle42.

{kind=link}