JPMorgan Chase, a financial powerhouse in the U.S., and ING Group, a dominant banking institution in the Netherlands, have both ventured into the acquisition of FinTech companies to expand their digital capabilities. However, these acquisitions’ strategies and subsequent management have diverged significantly, reflecting differences in corporate governance, regulatory environments, and responses to crises. Here is our comparative analysis.

The Cases

The takeover of fintech companies by established financial institutions is generally an enormous challenge that should not be underestimated. This is also shown by the two cases where the due diligence and risk management apparently failed. This comparative analysis examines JPMorgan‘s acquisition of Charlie Javice‘s startup Frank and ING‘s acquisition of Payvision, highlighting how each bank’s approach has led to different outcomes, particularly in managing the fallout from these acquisitions gone wrong.

Case Study 1: JPMorgan and the Acquisition of Frank

Background and Acquisition Strategy: In 2021, JPMorgan Chase acquired Frank, a FinTech startup specializing in student loan financing, for $175 million. The acquisition was part of JPMorgan‘s broader strategy to enhance its digital offerings and appeal to younger, tech-savvy consumers.

However, the deal quickly turned sour when it was revealed that Frank‘s founder, Charlie Javice, allegedly inflated the company’s customer base from less than 300,000 to over 4 million. This misrepresentation led JPMorgan to file a lawsuit accusing Javice of fraud, falsifying records, and hiring a data scientist to create fake accounts. Javice, in turn, countered that JPMorgan was trying to deflect from its due diligence failures.

Background information: Charlie Javice has denied the allegations and countered that JPMorgan is trying to shift the blame for a failed acquisition onto her. She argued that the bank could not have been misled about Frank’s value given the due diligence materials and publicly available information. Additionally, Javice was arrested on charges of conspiracy, wire, and bank fraud related to these allegations. She was released on a $2 million bond on April 4, 2023. As part of her release conditions, she surrendered her passports and agreed to travel restrictions between New York City and southern Florida. Her trial is set to take place in October 2024.

Regulatory and Legal Response: JPMorgan responded swiftly to the discovery of alleged fraud by initiating legal action against Javice and cooperating with federal authorities, which led to her arrest on charges of conspiracy, wire fraud, and bank fraud. JPMorgan CEO Jamie Dimon publicly labeled the acquisition a “big mistake,” signaling transparency and accountability to shareholders and the public. The bank’s proactive legal measures and public acknowledgment of the failure reflect a strategy to minimize reputational damage and demonstrate a commitment to corporate governance.

Case Study 2: ING and the Acquisition of Payvision

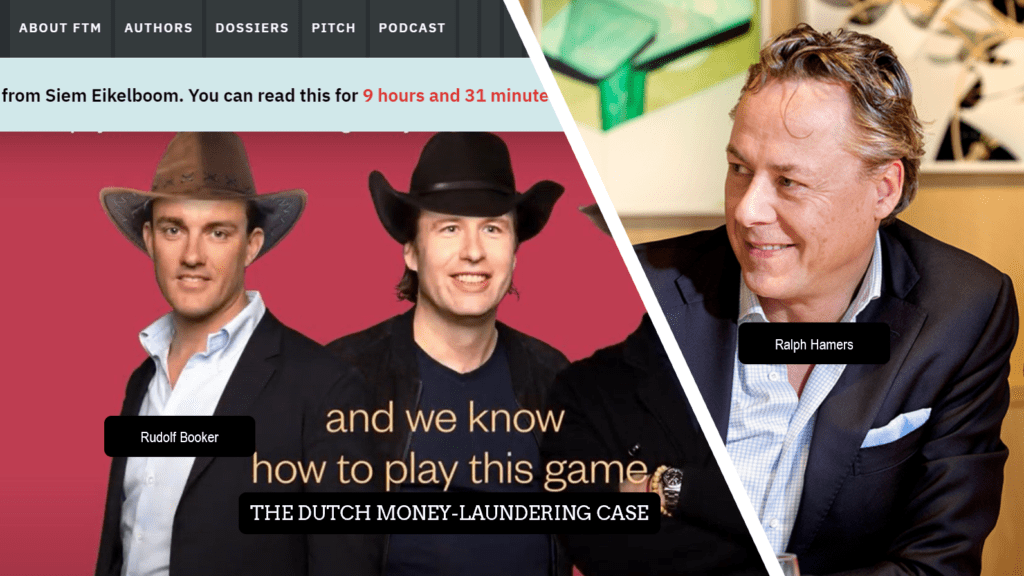

Background and Acquisition Strategy: In 2018, ING acquired a 75% stake in Payvision, a high-risk payment processor, for €360 million. The fintech was founded in 2002 by Rudolf Booker together with Gijs op de Weegh (COO) and Cheng Liem Li (CCO). The acquisition was intended to strengthen ING‘s position in omnichannel payments and expand its services in the growing e-commerce sector. However, Payvision‘s involvement in processing payments for controversial industries, including gambling, adult content, and investment fraud, soon surfaced. Even worse, it turned out that Payvision was heavily involved in facilitating cybercrime organizations with their payment services.

In 2020, the Dutch regulator DNB investigated Payvision and discovered systematic violations of financial laws and anti-money laundering regulations. DNB subsequently filed a criminal complaint with the authorities. Investigations were carried out, and fines were imposed on some of the former board of directors. The Payvision founders consequently stepped down in April 2020. ING announced in October 2021 that it would close Payvision.

Operating expenses declined 9.1% to €2,926 million from €3,218 million in 2020. Expenses in 2021

included a €44 million impairment on Payvision, while 2020 included a €260 million goodwill

impairment and €124 million of restructuring provisions and impairments (ING Group Annual Report 2021).

ING is said to have lost between €450 and 500 million for the failed Payvision takeover. These issues attracted negative media attention and led to significant reputational damage for ING.

Background information: At the beginning of 2019, the masterminds of two internationally active cybercrime organizations were arrested: the German Uwe Lenhoff and the Israeli Gal Barak. Both organizations were customers of Payvision and laundered hundreds of millions in stolen funds through them. Lenhoff died in prison in the summer of 2020 (cause of death unknown) and Barak was sentenced to several years in prison in September 2020 for investment fraud and money laundering. The criminal files show in detail the incredible extent of the money laundering and the deep involvement of Payvision.

Like Frank, Payvision‘s transaction volume was heavily inflated by money laundering transactions with fraudulent customers. Today, victims of former Payvision customers are still suing Payvision and ING for their role as cybercrime facilitators.

Regulatory and Legal Response: Unlike JPMorgan, ING‘s response to the problems at Payvision was less transparent and lacked the same level of decisive action. Although ING eventually decided to shut down Payvision in 2021, the bank did not pursue legal action against Payvision‘s founders, nor did it make any public claims for damages.

This inaction has raised concerns about ING‘s approach to risk management and accountability. Despite the substantial financial loss, ING‘s leadership, including former CEO Ralph Hamers and his successor Steven van Rijswijk, remained largely silent on the matter, failing to adequately address shareholder concerns or publicly acknowledge the acquisition’s failure.

Comparative Analysis

Jurisdictional and Regulatory Differences: The differing responses by JPMorgan and ING can partly be attributed to the regulatory environments in the U.S. and the Netherlands. The U.S. legal system allows for more aggressive litigation, which JPMorgan utilized to mitigate the impact of the Frank acquisition. In contrast, the Dutch legal system and ING‘s more reserved corporate culture may have contributed to ING‘s less confrontational approach. However, these jurisdictional differences do not fully explain the stark contrast in how the two banks handled the fallout from their acquisitions.

Corporate Governance and Risk Management: JPMorgan‘s approach reflects a more robust corporate governance structure, where swift legal action and public transparency are used to protect the bank’s interests and reassure shareholders. ING, on the other hand, appears to have taken a more cautious and less transparent route, which has led to questions about its commitment to shareholder value and effective risk management.

Impact on Shareholders and Public Perception: JPMorgan‘s proactive stance, including legal action and public acknowledgment of the failed acquisition, likely helped to contain the damage to its reputation and maintain shareholder confidence. In contrast, ING‘s reluctance to take similar steps in the Payvision case may have exacerbated shareholder losses and damaged its public image, particularly given the ethical concerns surrounding Payvision‘s business practices.

Conclusion

The contrasting approaches of JPMorgan and ING to FinTech acquisitions highlight the importance of corporate governance, regulatory compliance, and transparency in managing complex transactions. While both banks faced significant challenges, JPMorgan‘s more aggressive legal and public relations strategy appears to have better protected its interests and those of its shareholders.

In contrast, ING‘s handling of the Payvision acquisition raises concerns about its commitment to transparency and accountability, particularly in the face of substantial financial and reputational risks. As financial institutions continue to navigate the rapidly evolving FinTech landscape, these case studies offer important lessons on the critical role of due diligence, risk management, and corporate governance in ensuring successful acquisitions.

{kind=link}