At first glance, Payvision may look like an old scandal from the binary-options era. It is not. A newly reviewed EFRI dossier argues that Payvision did not merely sit in the background as a payment processor, but allegedly helped build, adapt, and preserve the payment rails that kept the Lenhoff/Barak fraud factories running. That matters now because the fallout is still alive: EFRI is pursuing claims in Amsterdam, criminal-file materials continue to be re-evaluated. The wider U.S. and T1/Payvision angle shows that similar allegations about European shell structures and high-risk processing also surfaced in U.S. litigation.

Key Findings

- The dossier supports a “knowing facilitation” theory, not just a “missed red flags” theory. It says Payvision’s role went beyond technical processing and extended to merchant setup, MID migration, settlement continuity, and operational stabilization.

- Booker’s own reported statements are central. According to the dossier, he acknowledged knowledge of the real beneficial owners, the binary-options/CFD/crypto environment, extreme chargeback levels, and 273 suspicious transaction reports filed between August 2016 and January 2019.

- The MCC issue is explosive. The dossier says Payvision used MCC 6211 for platforms that allegedly lacked the required MiFID authorization, while also accepting MOTO/CNP flows and shell-merchant structures.

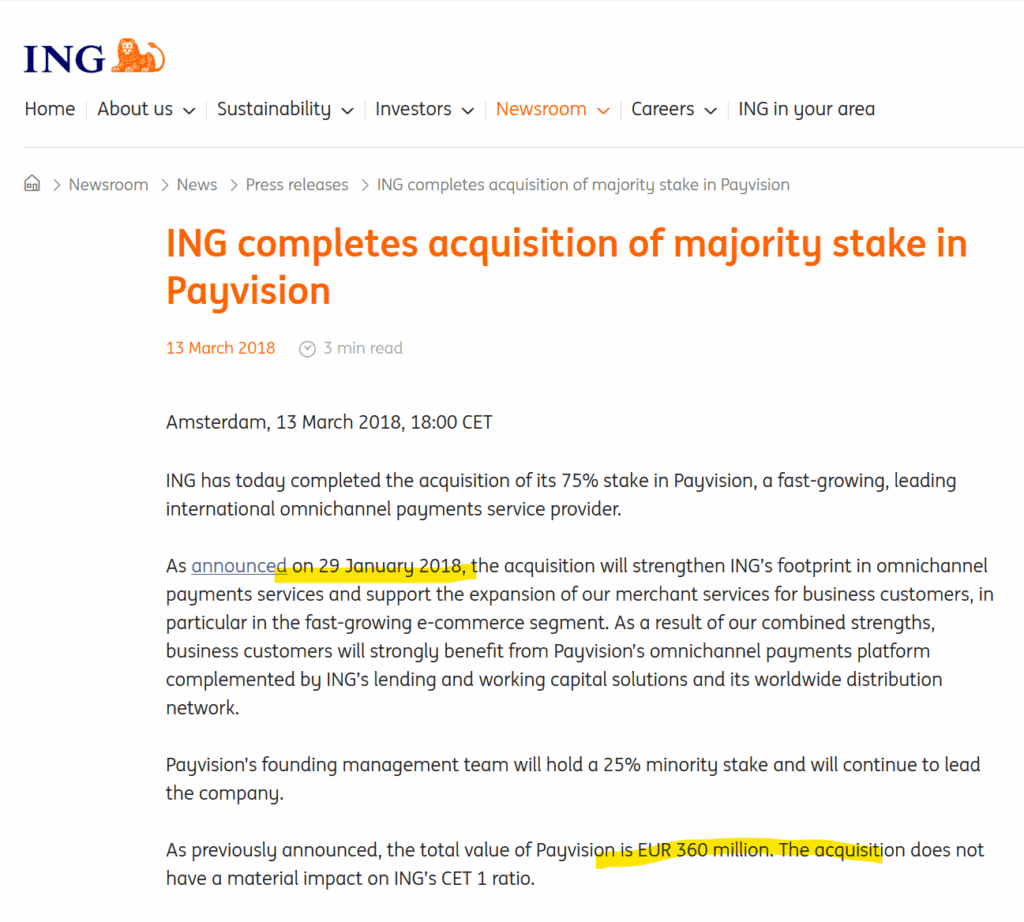

- The commercial-motive argument is plausible. The dossier ties scam-linked volume to fees, cash flow, and growth, and notes ING’s acquisition of 75% of Payvision at a reported €360 million valuation.

- There is external reinforcement for the control-failure narrative. ING has publicly stated that the Dutch criminal investigation into Payvision concerned conduct dating from before ING acquired the company, and ING’s disclosures noted the April 2024 Dutch-authorities decision to resolve that criminal investigation.

- The U.S. angle matters. Public Nevada records show Payvision B.V. was named as a defendant in Ibuumerang v. T1 Payments, alongside T1, Donald Kasdon, Amber Fairchild, and Pixxles.

The Payvision Dossier

There are processors that miss red flags. And then there are processors that, if the record holds up, look like they helped keep the scam machine humming.

The Scam Infrastructure Facilitator

That is the core force of the EFRI dossier. It does not describe Payvision as a passive bystander that got fooled by clever merchants. It describes Payvision as an allegedly active infrastructure partner in the Lenhoff/Barak ecosystem: a company that knew what kind of business it was processing, knew who stood behind the front entities, knew the fraud and chargeback metrics were terrible, and still kept the rails open.

Read our reports on Payvision here.

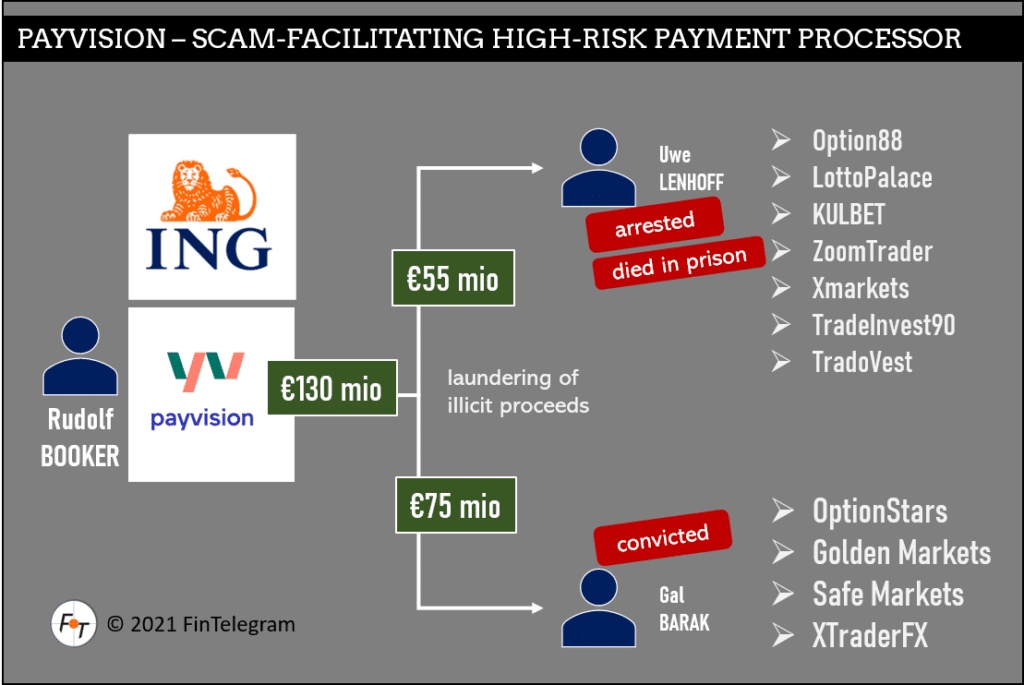

The dossier starts from a large and ugly factual base. It says German and Austrian criminal investigators identified a fraud complex involving platforms such as optionstars/global, xtraderfx, safemarkets, goldenmarkets, option888, xmarkets, tradovest, tradeinvest90, and zoomtrader/global, harming 59,345 European consumers for roughly €340 million between September 2015 and the January 2019 arrests. It identifies Payvision B.V. and its sister Acapture B.V. as the principal payment-service providers for those systems.

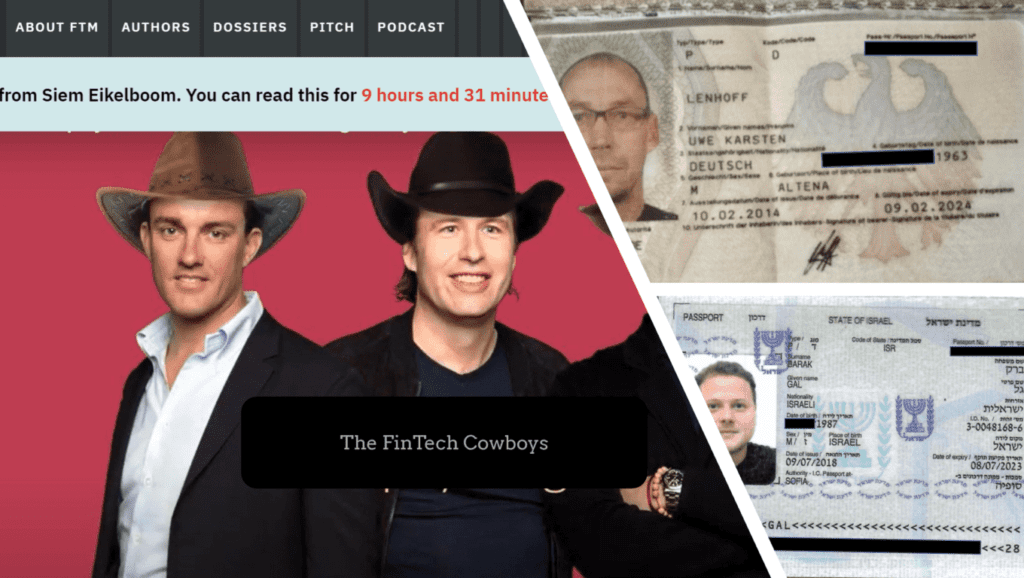

FinTech Cowboys and Co-Conspirators

Then the dossier gets more dangerous for Payvision. It says the company’s role did not stop at taking cards and sending money onward. It says the files document participation in setting up, adjusting, and continuing merchant and settlement structures. That is the difference between “processor” and “operator’s enabler.” If true, Payvision was not just near the fraud. It was allegedly helping preserve its plumbing.

The material on the former Payvision CEO Rudolf Booker is especially damaging. According to the dossier,

- Booker confirmed that Payvision knew the connected platforms were offering binary options, and later CFD/crypto-related products, to retail customers;

- knew Lenhoff and Barak were the real economic actors behind formally different merchants; saw chargeback rates ranging from 2% up to 20% per month; and

- filed 273 FIU reports for possible money laundering or terrorist financing. That is not the profile of an ordinary merchant book. It is the profile of a business relationship screaming for shutdown.

And yet the dossier says the business continued.

The MCC 6211 Issue

The MCC 6211 issue matters much in the Payvision scheme. The dossier says Payvision used a code associated with licensed broker or securities activity even though the connected platforms allegedly lacked the necessary MiFID authorization. It also says Payvision accepted MOTO flows and shell-style merchant structures that distorted the true risk and regulatory profile of the underlying activity. If accurate, that is not just sloppy compliance. It is a processing architecture that allegedly made dirty business look cleaner than it was.

The dossier also offers a motive. It notes that ING bought 75% of Payvision at a reported €360 million valuation in early 2018 and argues that the high-risk volumes tied to Lenhoff/Barak were commercially meaningful. More volume meant more fees, more growth, and a better valuation story. That inference is commercially plausible even where intent remains contested.

The T1 / U.S. Angle

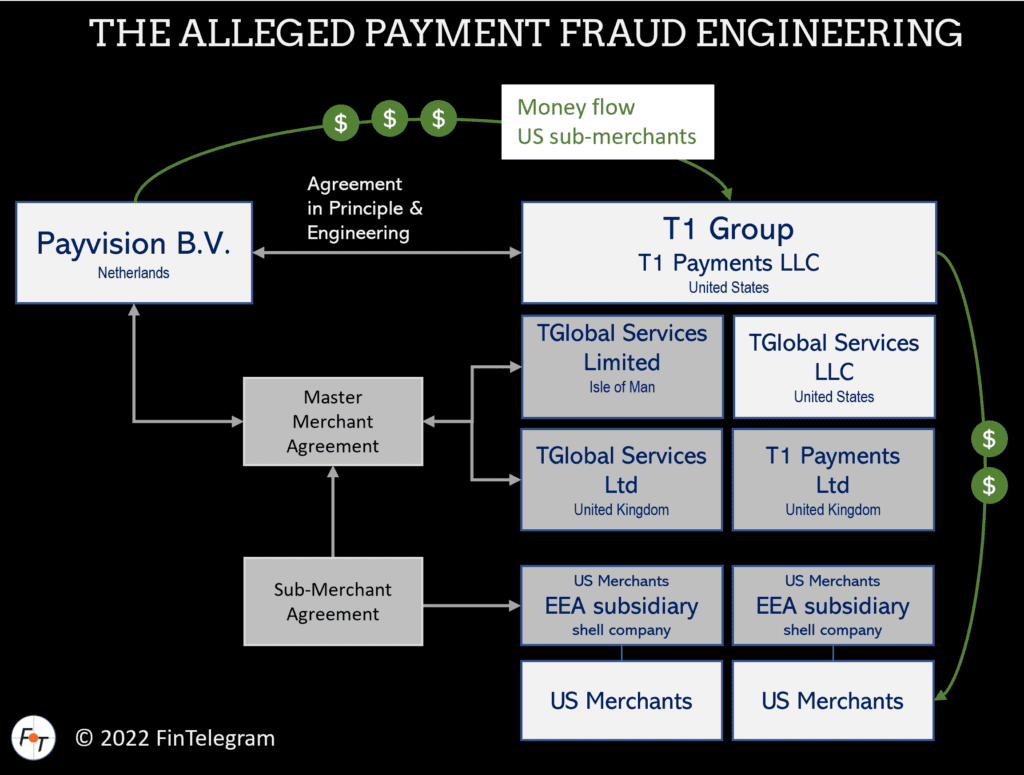

The dossier explicitly says similar allegations surfaced in U.S. cases between 2019 and 2022, including allegations that Payvision helped merchants build European company structures to obtain card-processing access. That matters because it shows the EFRI theory is not some one-off Austrian or German complaint. It echoes a broader pattern.

Public Nevada records support that broader picture. In Ibuumerang, LLC v. T1 Payments LLC et al., Payvision B.V. was named as a defendant alongside T1 Payments LLC, T1 Payments Limited, TGlobal Services Limited, Donald Kasdon, Amber Fairchild, and Pixxles, Ltd.

Public records do not clearly disclose the settlement terms for Payvision or ING in that U.S. case. What it does show is that the case existed, that Payvision was inside the T1 litigation orbit, and that later T1 bankruptcy materials treated the U.S. litigation landscape as part of the wider post-collapse fallout. So it is safe to state: Payvision was sued in the U.S. in the T1 orbit, and the public record supports that this litigation was later resolved or dismissed without publicly visible settlement detail in the materials reviewed.

That is enough to make the editorial point: the allegation that Payvision allegedly helped structure European wrappers for high-risk underlying business was not confined to the Lenhoff/Barak files. It also showed up in U.S. litigation connected to T1 Payments.

FinTelegram Take

The dossier’s real punch is simple.

It does not depict Payvision as a processor that merely failed to act fast enough. It depicts Payvision as a company that allegedly helped industrialize the payment rails of fraud — and kept doing so while the warning lights flashed red.

If that reading of the files is right, then Payvision’s role was not incidental. It was infrastructural.

And that is exactly why this is a hot case again.

Whistle42 CTA

FinTelegram invites whistleblowers, former Payvision staff, merchants, compliance officers, and victims with information on Payvision, Rudolf Booker, ING, T1 Payments, or related merchant structures to contact us via Whistle42. Confidential submissions help expose the payment architecture behind cyberfinance fraud.

{kind=link}