OSL Pay, the Milan‑based payments arm of Hong Kong–listed OSL Group, is positioning itself as a MiCAR‑regulated crypto on‑ramp in the EU while at the same time providing core card and wallet rails to offshore exchanges MEXC and WEEX that target EU clients without MiCAR authorization and have attracted regulatory warnings. This dual role creates a structural “on‑ramp paradox”: an Italian VASP under MiCAR’s transitional regime effectively front‑ends unregulated trading venues for European customers.

Key Findings

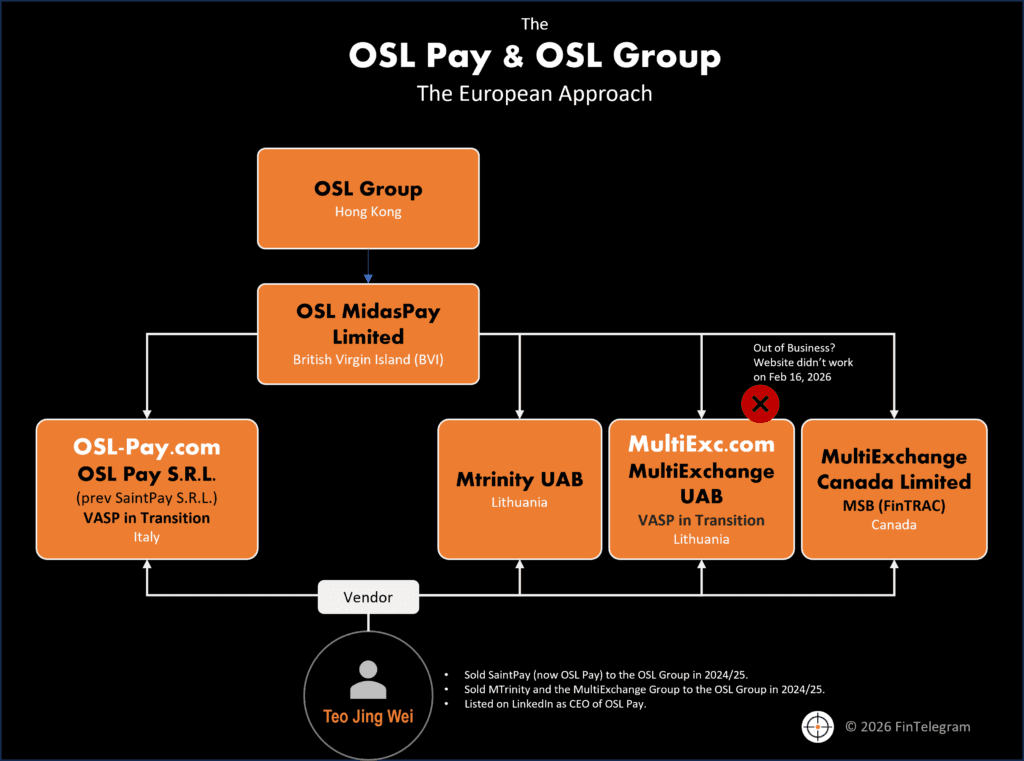

- OSL Pay S.R.L. (formerly Saintpay S.R.L.) is an Italian VASP founded by Teo Jing Wei and indirect wholly owned subsidiary of Hong Kong–listed OSL Group Limited, acquired via OSL MidasPay Limited (BVI).

- OSL Pay operates from Milan under MiCAR’s transitional regime and is in the process of obtaining full CASP authorization in Italy.

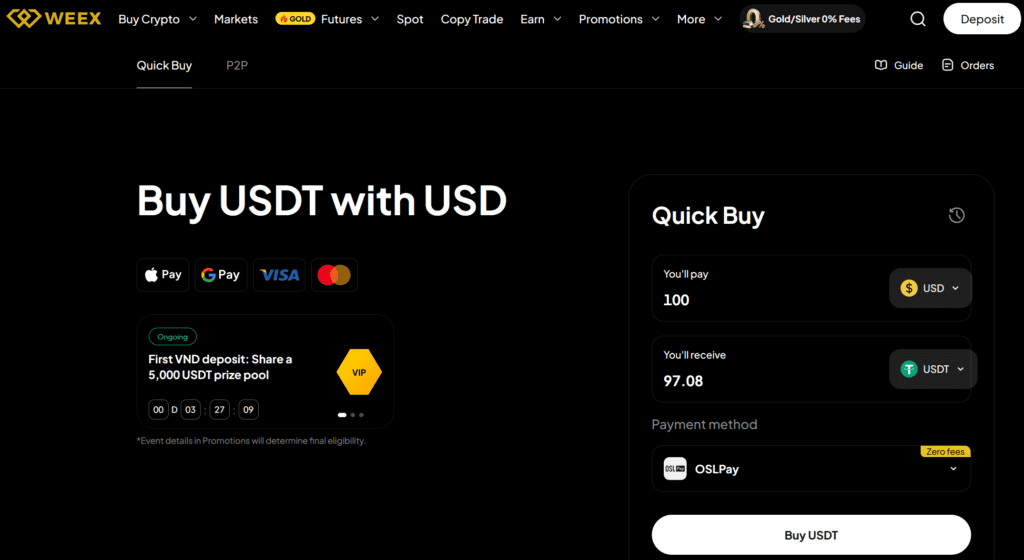

- In July 2025 OSL Pay and MEXC launched card‑based fiat on‑ramp services for MEXC; in September 2025 the partnership expanded to Apple Pay and Google Pay integrations in MEXC’s Quick Buy flow.

- WEEX publicly confirms integrating the “OSL Payment Channel” for its Quick Buy feature, with users redirected to OSL Pay to pay via Visa, Mastercard, Apple Pay or Google Pay.

- The MEXC and WEEX Quick Buy screens, payment options and “How to buy crypto” instructions are nearly identical, indicating a shared technical and UX stack centered on OSL Pay’s infrastructure.

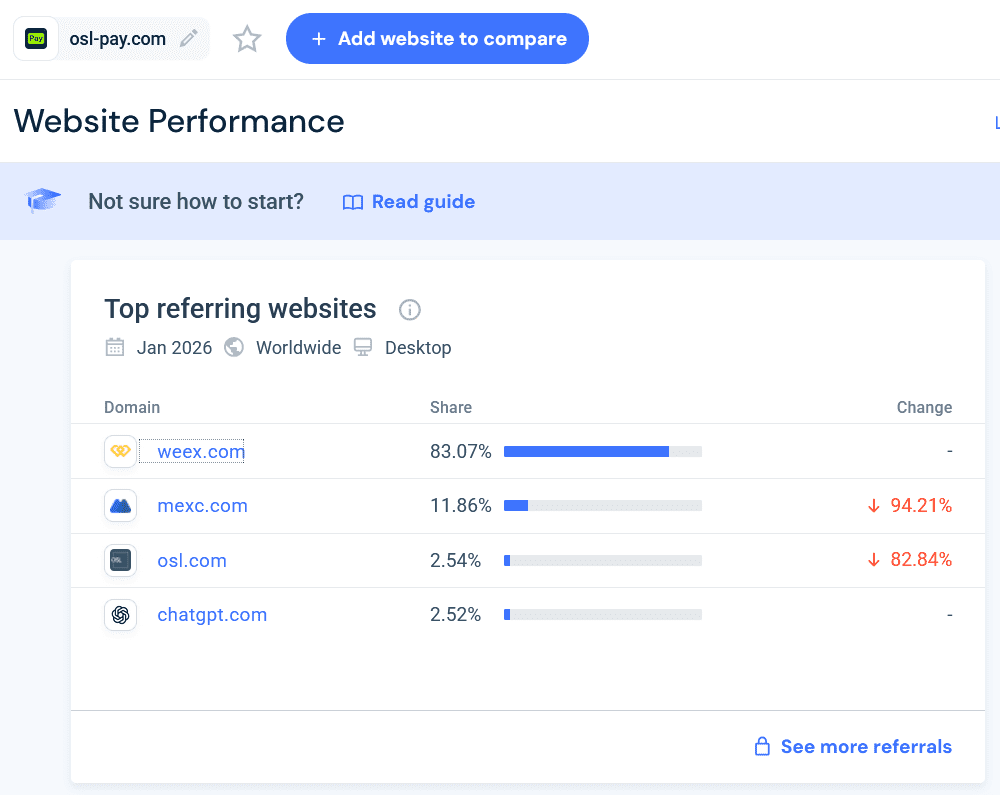

- Traffic analytics show that in January 2026 about 83% of osl-pay.com’s referral traffic came from weex.com and roughly 12% from mexc.com, meaning around 95% of visible referrals originate from these two exchanges.

- Neither MEXC nor WEEX is publicly listed as a MiCAR‑authorized CASP in the EU, yet both actively market trading services, including derivatives, to EU users while relying on OSL Pay’s “local” payment rails.

- European regulators have issued warnings against MEXC and WEEX or related domains for operating without necessary local authorization, though OSL Pay is not named in these warnings.

- In early 2024 BGX Group invested about HK$710 million (≈ US$90m) into OSL Group, taking an approximately 30% stake and strengthening the group’s capital base before its European payments expansion.

- Taken together, these facts create an “on‑ramp paradox” in which an Italian MiCAR‑aspirant VASP (OSL Pay) functions as the primary fiat gateway for two offshore, non‑MiCAR exchanges, raising material questions about group‑level risk appetite, oversight and regulatory coverage in the EU.

Short Narrative

Our review of MEXC and WEEX payment flows reveals a shared gateway: OSL Pay. Screenshots show that:

- MEXC advertises purchases via “OSL Pay, Google Pay or Apple Pay.”

- WEEX lists OSLPay as the recommended card payment method.

- Both exchanges present nearly identical “Quick Buy” layouts—right down to the step-by-step instructional wording and UI structure.

- The checkout interface and payment selector modules appear operationally aligned.

The overlap is not cosmetic—it is infrastructural. Further analysis of osl-pay.com’s referral traffic indicates that roughly 95% of inbound desktop referral traffic comes from weex.com and mexc.com, suggesting that OSL Pay functions predominantly as a dedicated on-ramp rail for these two exchanges.

Go to the OSL Pay compliance listing on RatEx42

OSL Pay: Corporate background and MiCAR ambitions

OSL Pay S.R.L. originates from the Italian company Saintpay S.R.L., incorporated in March 2023 and described in HKEX documents as the “Italian Target Company” to be acquired by OSL MidasPay Limited, a BVI vehicle wholly owned by OSL Group Limited (HKEX: 0863). After completion of the acquisition, Saintpay/OSL Pay becomes an indirect wholly owned subsidiary of OSL Group. Italian fintech media report that OSL Pay opened a Milan office and appointed former Bitpanda and Circle executive Orlando Merone as General Manager for Europe.

Recent Italian coverage confirms that OSL Pay is operating in Italy under MiCAR’s transitional regime and is in the process of obtaining full CASP authorization from the Bank of Italy and CONSOB. These articles frame OSL Pay as a bridge between traditional payment methods (cards, Apple Pay/Google Pay) and digital assets, stressing regulatory compliance and local hiring. At the same time, they provide no detail on OSL Pay’s exposure to high‑risk offshore trading platforms such as MEXC and WEEX.

The Lithuanian OSL Branch

Filings with the Hong Kong Stock Exchange confirm that between late 2024 and early 2025, the OSL Group acquired a portfolio of regulated entities from vendor Teo Jing Wei. This acquisition included the Italian entity Open Pay S.R.L. (formerly known as SaintPay), which is registered as a Virtual Asset Service Provider (VASP) in Italy. Additionally, the transaction encompassed the acquisition of MultiExchange UAB (operating as MultiExchange or MultiEx) in Lithuania, which also holds VASP status.

As part of this strategic expansion into North America, Teo Jing Wei further divested MultiExchange Canada Limited to the OSL Group; this entity is registered as a Money Services Business (MSB) with the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). In our review on February 16, 2026, the MultiExc.com website was not functioning. It was not possible to purchase cryptocurrencies, and the LinkedIn icon was linked to the OSL Pay account.

Compliance Analyst Notes

- Entity Names: The filings (specifically the Europe SPA dated December 9, 2024, and subsequent amendments in January 2025) identify the target companies. While “MultiEx” is the trading name, the corporate registry name in Lithuania often appears as “MultiExchange UAB.”

- Regulatory Status: The definitive value of these acquisitions for OSL Group was the pre-existing regulatory statuses (VASP in Italy/Lithuania and MSB in Canada), which allows OSL to bypass the lengthy application periods for new licenses.

- Timeline: The initial agreement was struck in December 2024, with amendments and completions extending into Q1 2025, making “2024/25” the correct temporal designator.

Deep integration with MEXC and WEEX

In July 2025, OSL Pay and MEXC announced a partnership to launch credit and debit card fiat on‑ramp services for MEXC users, allowing Visa and Mastercard purchases of crypto via OSL infrastructure. In September 2025 this partnership was expanded: OSL Pay and MEXC jointly announced the integration of Apple Pay and Google Pay for crypto purchases, embedded into MEXC’s Quick Buy flow. Current MEXC promotional pages explicitly advertise campaigns such as “Buy XAUT or PAXG via OSL Pay, Google Pay or Apple Pay,” evidencing that OSL Pay remains at the heart of MEXC’s card and wallet on‑ramp stack.

WEEX has implemented an almost identical user journey. In a November 2025 article, WEEX explains that its Quick Buy feature integrates the “OSL Payment Channel,” describing OSL Pay as part of OSL Group and registered as a VASP in Italy. The article details that WEEX users select “OSL Pay” as payment method, are redirected to OSL’s environment, and can then pay via Visa, Mastercard, Apple Pay or Google Pay—mirroring the MEXC flow and marketing language almost one‑to‑one.

Traffic analytics for osl-pay.com further underline this dependency: in January 2026, an estimated 83% of referral traffic originated from weex.com and about 12% from mexc.com, meaning that roughly 95% of visible referrals come from these two offshore exchanges. This concentration suggests that, in practice, OSL Pay’s European business is dominated by providing card and wallet rails to MEXC and WEEX rather than servicing a diversified portfolio of regulated EU platforms.

Regulatory Red Flags and The “On‑Ramp Paradox”

Neither MEXC nor WEEX appears as a MiCAR‑authorized CASP in available public registries, and both operate from offshore jurisdictions (MEXC from Seychelles, WEEX as an offshore derivatives venue) while actively marketing to EU users in multiple languages.

MEXC Estonia OÜ is registered in Estonia with Yichen Peng listed in the commercial register as its manager and beneficial owner, but this entity is not disclosed as the operating company on the main MEXC trading websites (mexc.com and mexc.co). An Estonian registration obtained before the MiCAR framework does not in itself grant passporting rights or authorization to offer crypto‑asset services across other EU or non‑EU jurisdictions, meaning MEXC would still require appropriate local or MiCAR‑compliant approvals to lawfully target those markets.

Various European regulators and warning lists have flagged MEXC and WEEX or their associated domains for operating without local authorization and offering high‑risk derivatives to retail clients (read the Dutch AFM warning here). While these warnings do not directly name OSL Pay, they make clear that the underlying venues are outside the supervised perimeter.

Against this backdrop, OSL Pay’s MiCAR‑driven positioning as a compliant Italian “gateway” creates a structural conflict. On the one hand, the company seeks EU‑level authorization as a CASP and promotes its role in building regulated digital‑asset rails in Europe.

On the other, its main practical activity appears to be the provision of card, Apple Pay and Google Pay on‑ramps to two offshore exchanges that lack MiCAR authorization, face regulatory warnings, and offer leveraged trading products to EU clients. This effectively allows MEXC and WEEX to advertise “local” and “fully compliant” payment methods while leaving trading and custody activities outside EU prudential and investor‑protection regimes.

The situation is further framed by OSL Group’s strategic funding: in early 2024 BGX Group agreed to invest around HK$710 million (about US$90 million) into OSL Group, taking a stake of roughly 30%. Shortly thereafter, OSL structured its European subsidiaries (including OSL Pay) and ramped up its EU presence. The timing suggests that BGX‑backed capital has financed an aggressive European expansion built around servicing offshore exchanges, raising questions about group‑level risk appetite and governance.

Key actors and roles around OSL Pay

| Item | Name / Entity | Jurisdiction | Regulatory status (public) | Role in network |

|---|---|---|---|---|

| On‑ramper | OSL Pay S.R.L. (ex‑Saintpay S.R.L.) dba OSL Pay www.osl-pay.com | Italy | VASP in Italy, MiCAR CASP under transitional regime; indirect subsidiary of OSL Group | Provides card, Apple Pay and Google Pay fiat on‑ramps for MEXC and WEEX; core payment gateway into EU. |

| On-ramper | MultiExchange UAB dba MultiEx www.multiex.com | Lithuania | VASP in Líthuania | On-ramper and payment facilitator |

| Parent group | OSL Group Limited (prev BT Technology Group Limited) (HKEX: 0863) | Hong Kong | HK‑listed digital asset group | Owns OSL MidasPay Limited (BVI) which acquires OSL Pay; overall strategic controller of EU on‑ramp structure. |

| Investor | BGX Group Holding Limited | Hong Kong | Private crypto group; investor in OSL Group | Invests ≈ US$90m in OSL Group in 2024, taking ~30% stake and enabling capital‑intensive expansion including EU payments build‑out. |

| Exchange | MEXC MEXC Estonia OÜ | Seychelles / offshore Estonia | Not MiCAR‑authorized in EU; subject to multiple EU regulatory warnings | Uses OSL Pay for Visa/Mastercard and Apple/Google Pay Quick Buy flows addressing EU clients. |

| Exchange | WEEX | Offshore | Not MiCAR‑authorized in EU; also subject to regulatory warnings | Integrates OSL Payment Channel (OSL Pay) as Quick Buy gateway, with identical UX and “How to buy crypto” flow to MEXC. |

| Executives | Orlando Merone (LinkedIn) Teo Jing Wei (LinkedIn) | Italy | General Manager CEO | Wei is the founder of SaintPay and sold the company to OSL Group |

Call for Whistleblowers

FinTelegram views OSL Pay’s dual positioning—as a MiCAR‑aspirant Italian VASP and as the dominant fiat on‑ramp for unregulated offshore exchanges with EU customer reach—as a material compliance and investor‑protection concern. The concentration of osl-pay.com referral traffic from WEEX and MEXC, combined with deep technical integration and mirrored user journeys, underscores the need for closer supervisory scrutiny of this “on‑ramp paradox.”

{kind=link}