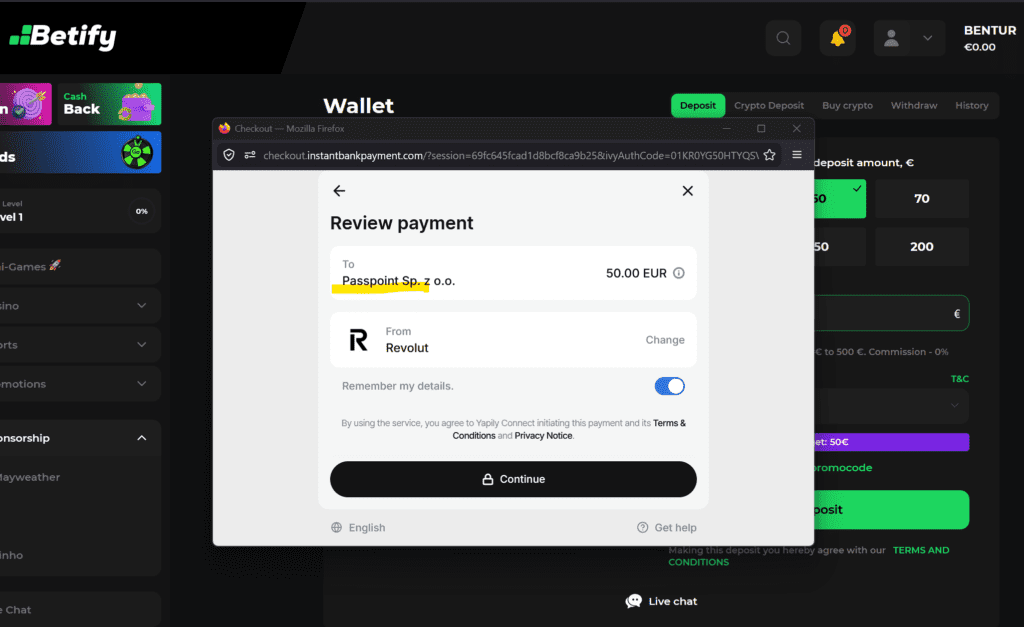

Passpoint markets itself as a financial orchestration platform for Africa, Europe, and G20 payment corridors. But FinTelegram’s Betify review found something far more problematic: Passpoint Sp. z o.o., its Polish entity, appeared as the named payee in an open-banking/bank-transfer rail used to fund Betify, an offshore casino accessible from EU jurisdictions. This is not a passive API footprint. A payee is the payment-facing recipient. Unless Passpoint can show a proper regulated basis, the arrangement raises serious concerns of unlicensed payment agency, merchant masking, and transaction-laundering risk.

Executive Summary

Passpoint operates under the domain mypasspoint.com and presents itself as a financial orchestration platform connecting businesses to payment, compliance, FX, liquidity, and settlement infrastructure across Africa, Europe, and G20 markets. Its own website says Passpoint is “not a payments company” but an orchestration layer between businesses and global finance, while its terms describe Passpoint Technologies Inc. as a global payment infrastructure provider connecting businesses to multiple pay-in and payout methods through a single API.

That positioning must now be assessed against the facts found in FinTelegram’s May 2026 Betify review. In the reviewed bank-transfer/open-banking flow, the payment route was:

Betify Cashier → InstantBankPayment → Yapily Connect UAB → Revolut / Wise → Passpoint Sp. z o.o.

Read our latest Betify review here.

The critical point is that Passpoint Sp. z o.o. appeared as the payee. That is not a minor technical trace. In an account-to-account or open-banking payment, the payee is the entity presented to the payer and the banking/payment chain as the recipient of funds. If Passpoint is the payee in a casino deposit flow, then Passpoint is not merely “somewhere in the stack.” It is the payment-facing entity in the transaction.

The Polish entity is not a remote or unrelated company. Public Polish company data identifies Passpoint Sp. z o.o. under KRS 0001139121, NIP 8762513363, and REGON 540221384. Public registry data links the entity to Kelechi Chidiebube Uchegbulem, Adejuwon Samuel Oyebanjo, and Chinedu Bendeict Ojiteli.

Passpoint’s own public narrative emphasizes compliance, governance, and control. In a May 2026 TechCabal publication, CEO Kelechi Uchegbulem stated that the payment-infrastructure challenge is not merely moving money, but “governing it,” including routing, compliance across jurisdictions, FX exposure, and predictable settlement.

Key Findings

- Passpoint appeared as the payee in Betify’s EU-facing payment rail. In FinTelegram’s May 2026 Betify review, Passpoint Sp. z o.o. was shown as the payee in the bank-transfer/open-banking flow. This makes Passpoint payment-facing in the transaction, not a passive infrastructure vendor.

- The reviewed rail connected Betify to regulated open-banking infrastructure. The flow ran through InstantBankPayment, presented Yapily Connect terms, routed toward Revolut/Wise-style bank access, and then showed Passpoint Sp. z o.o. as payee.

- A payee role implies onboarding and settlement relevance. If Passpoint is the payee, it must have been introduced into the payment chain, must have a contractual or operational role, and must be able to explain who onboarded the underlying merchant, who controls settlement, and who receives the funds after Passpoint.

- Passpoint Sp. z o.o. is not a licensed EU payment institution. Publicly available company records identify it as a Polish limited liability company with financial-services-related business classification and minimal share capital. That is not the same as authorization to act as a payment institution, acquiring entity, payment agent, or merchant-of-record layer for third-party gambling operators.

- The Polish entity is controlled by the Passpoint team. Public Polish company data links the entity to Kelechi Uchegbulem, Adejuwon Oyebanjo, and Chinedu Ojiteli, with registry data showing Oyebanjo and Uchegbulem as shareholders and Uchegbulem/Ojiteli as representatives.

- Passpoint’s public positioning increases, not reduces, its compliance responsibility. Passpoint markets itself as a financial orchestration layer that unifies payments, compliance, liquidity, and settlement across Africa, Europe, and G20 markets.

- Passpoint’s disclaimer does not solve the issue. Its terms say it does not assume liability for the legality or quality of goods or services paid for using its infrastructure. That may be a platform disclaimer, but it does not neutralize AML, merchant-screening, licensing, payment-purpose, or gambling-risk obligations where Passpoint appears as the payment-facing payee.

- The Betify finding suggests merchant masking. The player is funding Betify, but the payee shown in the payment rail is Passpoint Sp. z o.o. That mismatch is a central red flag in payment-rail investigations.

- The compliance risk is very high. Unless Passpoint can demonstrate a lawful regulated basis, transparent merchant-of-record structure, and proper gambling-merchant onboarding, the arrangement raises concerns of unlicensed payment intermediation, merchant masking, and transaction-laundering risk.

Key Data Table: Passpoint

| Field | Data |

|---|---|

| Brand | Passpoint |

| Main domain | mypasspoint.com |

| Social Media | |

| Public positioning | Financial orchestration layer for Africa, Europe, and G20 markets |

| Named contracting entity in terms | Passpoint Technologies Inc. |

| Claimed function | Unified API for pay-ins, payouts, compliance, FX, liquidity, and settlement |

| Delaware entity referenced by profile | Passpoint Technologies Inc., Delaware / United States |

| Polish entity | Passpoint Sp. z o.o. (registered Nov 2024) |

| Polish KRS / NIP / REGON | 0001139121 / 8762513363 /540221384 |

| Registry-linked persons | Adejuwon Oyebanjo (LinkedIn) and Kelechi Uchegbulem (LinkedIn) |

| Observed casino rail | Betify → InstantBankPayment → Yapily Connect UAB → Revolut / Wise → Passpoint Sp. z o.o. |

| Observed role in Betify rail | Named payee |

| License issue | No evidence identified that Passpoint Sp. z o.o. is authorized as an EU payment institution or payment agent for third-party casino collection |

Compliance Analysis

1. Passpoint’s payee role is active, not incidental

The decisive fact is simple: Passpoint Sp. z o.o. appeared as payee.

That changes the legal and compliance assessment. A payee in a bank-transfer or open-banking flow is not a background vendor, analytics provider, or invisible API component. The payee is the entity presented to the payer and the payment chain as the recipient.

Therefore, the question is not merely whether Passpoint had technical exposure to Betify. The question is:

Why was Passpoint Sp. z o.o. presented as the payee for a Betify casino deposit?

That role strongly indicates that Passpoint’s Polish entity was being used as a payment-facing entity, payment agent, merchant-of-record proxy, or settlement intermediary.

2. The licensing issue is central

Passpoint Sp. z o.o. is a Polish limited liability company. Public records show a recent registration, minimal share capital, and financial-services-related activity classification. Public records do not establish that the company is licensed as a payment institution, electronic money institution, acquiring institution, or authorized payment agent.

If Passpoint collects or appears to collect funds for third-party merchants, especially high-risk merchants such as offshore casinos, it must have a lawful regulatory basis. If it does not, the arrangement may amount to unlicensed payment intermediation.

In a gambling context, the issue becomes more serious. Payment providers cannot simply insert a corporate payee between the player and the gambling operator and claim to be a neutral orchestration layer. The onboarding, licensing, merchant-risk, and settlement responsibilities do not disappear because the flow is routed through an API.

3. Merchant masking and transaction-laundering risk

In the Betify flow, the economic purpose was funding a casino account. But the visible payee was Passpoint Sp. z o.o., not Betify, not Fortuna Games N.V., and not Deltaprime Limited.

That mismatch is a classic Rail Atlas red flag. It can obscure the true merchant from the player’s bank, the open-banking provider, the payer, and potentially downstream monitoring systems.

In plain terms: if the customer is funding Betify but the bank sees Passpoint, the transaction chain is masking the gambling merchant.

This is exactly the sort of structure that regulators, banks, and payment institutions should examine for transaction-laundering risk.

4. Passpoint’s own claims create a higher standard

Passpoint does not describe itself as a minor local reseller. It describes itself as a financial orchestration layer that unifies payments, compliance, liquidity, and settlement. Its public website says it provides access to pay-ins, payouts, acquiring, unified APIs, and compliance infrastructure. Its TechCabal announcement emphasizes governance, routing, compliance, FX exposure, and settlement control.

That makes the Betify finding more damaging, not less.

A platform that claims to govern cross-border payment flows cannot plausibly treat the identity of the underlying merchant and the legality of the payment purpose as irrelevant. If Passpoint’s Polish entity is the named payee, then Passpoint must explain the onboarding file, merchant category, settlement chain, and risk assessment.

5. Disclaimers do not override payment obligations

Passpoint’s terms include a disclaimer that it does not control or assume liability for the legality or quality of goods or services paid for through its infrastructure.

That clause may protect Passpoint in ordinary contractual disputes, but it does not answer the compliance question. A payment infrastructure provider that facilitates pay-ins and payouts cannot contract out of AML screening, sanctions controls, merchant due diligence, licensing analysis, or high-risk vertical monitoring.

For gambling-related flows, the obligation is even clearer: processors and payment facilitators must know whether they are servicing an authorized gambling merchant, an unauthorized offshore casino, or an intermediary disguising the true gambling beneficiary.

The Betify Rail: Why It Matters

FinTelegram’s May 2026 Betify review identified the following bank-transfer/open-banking rail:

Betify Cashier → InstantBankPayment → Yapily Connect UAB → Revolut / Wise → Passpoint Sp. z o.o.

This rail creates at least five compliance questions:

- Who onboarded Betify or the Betify-related merchant?

- Who decided that Passpoint Sp. z o.o. would appear as payee?

- What legal basis allows Passpoint Sp. z o.o. to act as the payment-facing recipient?

- Who receives the funds after Passpoint?

- Did Yapily, Revolut, Wise, or any banking partner know the payment purpose was offshore casino funding?

Until these questions are answered, Passpoint should be treated as a high-risk payment-rail entity.

Conclusion

Passpoint’s appearance in the Betify payment rail is not a harmless technical artifact. It is a serious compliance finding.

If Passpoint Sp. z o.o. is shown as payee, then Passpoint is the payment-facing recipient in a casino deposit transaction. That creates an immediate duty to explain the legal basis, licensing status, merchant onboarding, settlement path, and risk controls.

The central issue is no longer whether Passpoint is an African fintech with a Delaware parent and a Polish subsidiary. The issue is whether its Polish company is being used to collect or route EU player funds for an offshore casino without the necessary payment authorization and without transparent merchant disclosure.

Until Passpoint provides a convincing explanation, FinTelegram classifies Passpoint as a Very High Risk Rail Atlas Watchlist entity.

Whistleblower Request

FinTelegram invites players, bank employees, PSP insiders, open-banking professionals, former Passpoint staff, casino-payment insiders, and compliance officers to provide information about:

Passpoint Technologies Inc., Passpoint Sp. z o.o., Kelechi Uchegbulem, Adejuwon Oyebanjo, Chinedu Bendeict Ojiteli, Betify, Fortuna Games N.V., Deltaprime Limited, InstantBankPayment, Yapily Connect UAB, Revolut, Wise, and related settlement accounts, merchant agreements, wallet addresses, and onboarding files.

Information can be submitted confidentially through Whistle42.

{kind=link}