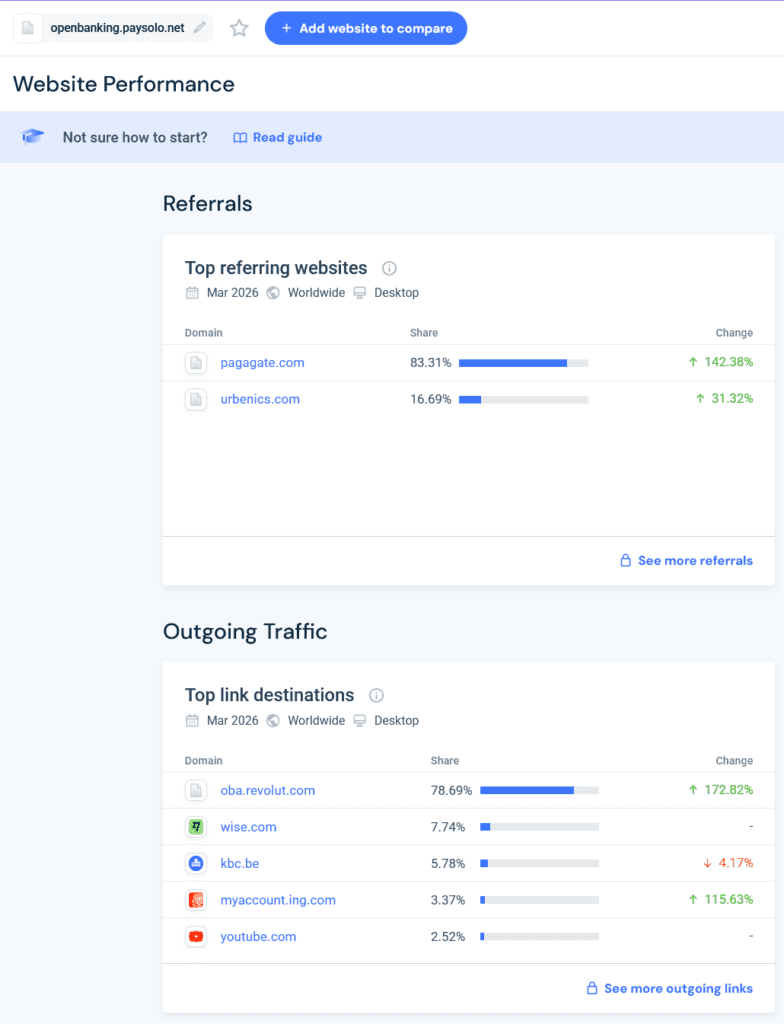

FinTelegram’s first Revolut Rail Atlas follow-up zooms in on openbanking.paysolo.net, a payment gateway that appears to sit between anonymous casino-facing gateways and Revolut’s Open Banking API. SimilarWeb screenshots indicate that all referring traffic to openbanking.paysolo.net came from the anonymous payment gateways Pagagate and Urbenics in March 2026, while more than 78% of outgoing traffic reportedly went to oba.revolut.com. The working hypothesis: Paysolo may represent a crypto/open-banking bridge inside a layered casino-payment architecture.

Key Findings

- Paysolo’s public corporate site identifies Paysolo O.O.D. as a Bulgarian company with registration number 207268330, registered as a provider of virtual/fiat exchange services in Bulgaria’s National Revenue Agency VASP register.

- Paysolo markets itself as a EUR-to-crypto bridge and virtual IBAN provider, offering SEPA/SWIFT-based fiat-to-crypto services.

- The open-banking gateway

openbanking.paysolo.netis live and publicly returns a minimal version page, supporting its operational existence. - SimilarWeb screenshots show a suspicious traffic funnel: Pagagate and Urbenics as the only visible referring domains to

openbanking.paysolo.net, andoba.revolut.comas the dominant outgoing destination. - Pagagate and Urbenics appear in FinTelegram’s casino-rail observations, suggesting the Paysolo gateway may sit inside an offshore iGaming payment chain. This remains a working hypothesis pending payment-test evidence, registry/DNS linkage, and merchant documentation.

- The relationship between

paysolo.ioandpaysolo.netis plausible but should be framed carefully.paysolo.iois the corporate/marketing site;paysolo.netpresents as “PaySolo – Your payment partner” and references “Newtech Mobile,” so the precise legal/operator linkage requires further verification.

Revolut Rail Map: The Paysolo Corridor

The observed traffic pattern suggests the following payment architecture:

Casino-facing gateway → Pagagate / Urbenics → openbanking.paysolo.net → Revolut Open Banking API → Revolut account

This is exactly the type of multi-layered open-banking rail FinTelegram identified in the Revolut Rail Atlas opener. The key issue is not merely that Revolut appears as a bank destination.

The issue is that Revolut appears downstream of gateways that, based on traffic intelligence, are connected to casino environments.

Read our initial Revolut Rail Map report here.

Paysolo: Crypto Bridge, Virtual IBAN Provider, Or Casino-Rail Middleware?

Paysolo’s own materials describe a platform offering virtual IBAN services, crypto-asset exchange, payment processing, SEPA, and fiat-to-crypto conversion. Its website says users can send EUR via SEPA or SWIFT to a Paysolo virtual IBAN, convert EUR to crypto, and withdraw crypto to external wallets.

That profile is highly relevant in the casino-payment context. Offshore casino operators increasingly need rails that can move user money from bank accounts into crypto or quasi-crypto settlement environments. A VASP-style bridge with open-banking intake, virtual IBANs, and crypto withdrawal functionality may therefore become a critical conversion layer.

FinTelegram does not state at this stage that Paysolo knowingly services illegal casinos. The more precise finding is that openbanking.paysolo.net appears, based on the supplied traffic screenshots, to receive traffic from casino-facing gateways and to send substantial outgoing traffic to Revolut’s Open Banking endpoint.

Read all Revolut Rail Atlas reports here.

The SimilarWeb Evidence

The uploaded SimilarWeb screenshots indicate the following March 2026 pattern:

| Domain analysed | Finding | Compliance interpretation |

|---|---|---|

openbanking.paysolo.net | Referrals: Pagagate.com 83.31%, Urbenics.com 16.69%; Outgoing traffic: openbanking.paysolo.net 80.40% | 100% visible referral traffic from two gateway domains; Revolut appears to be the dominant downstream bank/API destination |

pagagate.com | Outgoing traffic: openbanking.paysolo.net 46.83%, aphrodite1.casino 19.31% | Pagagate appears connected to both Paysolo and a casino domain |

urbenics.com | Referrals include Boomerang Bet, Casinoly, Posido, Vegasino, Skyhills; Outgoing traffic: openbanking.paysolo.net 80.40% | Urbenics appears casino-facing; Paysolo appears as the dominant downstream endpoint |

FinTelegram understands that openbanking.paysolo.net recorded more than 309,000 visits in March 2026. This is not a fringe technical endpoint. It is a meaningful traffic node.

Why This Matters For Revolut

In the Revolut Rail Atlas opener, FinTelegram identified a broader pattern: offshore casino sites often route payments through anonymous gateways and open-banking intermediaries before landing at bank APIs, including Revolut’s oba.revolut.com.

The Paysolo case gives that model a sharper structure:

Urbenics / Pagagate → Paysolo open-banking gateway → Revolut Open Banking

This raises several questions:

- Does Revolut see only the final open-banking payment instruction, or can it detect the upstream casino/gateway context?

- Does Revolut monitor repeat traffic from high-risk open-banking intermediaries?

- Does Revolut classify flows from Paysolo as crypto, open banking, virtual IBAN, merchant payment, or customer-authorised account transfer?

- Does the gateway chain obscure whether the underlying transaction relates to gambling, crypto conversion, or both?

The compliance concern is the possible blending of three high-risk categories: offshore gambling, open banking, and fiat-to-crypto conversion.

Corporate & Regulatory Footprint

Paysolo’s public website identifies Paysolo O.O.D., Bulgaria, company registration number 207268330, as the relevant legal entity and states that it is registered in Bulgaria’s National Revenue Agency VASP register.

Its terms define the platform as including paysolo.io, app.paysolo.io, associated mobile applications, virtual IBAN services, crypto-asset exchange, and payment processing.

This matters because VASP registration is not a licence to process illegal gambling flows. A VASP handling fiat-to-crypto conversion must still manage AML, source-of-funds, transaction-monitoring, sanctions, fraud, and high-risk merchant exposure. If casino-originated flows are entering the system via Pagagate or Urbenics, the compliance question becomes unavoidable.

Evidence & Confidence Table

| Entity / Rail Element | Observed Role | Evidence Type | Jurisdiction | Confidence Grade |

|---|---|---|---|---|

| Paysolo O.O.D. | Public corporate entity behind Paysolo.io | Website disclosure | Bulgaria | Confirmed |

paysolo.io | Corporate / product site | Public website | Bulgaria | Confirmed |

paysolo.net | “PaySolo – Your payment partner” gateway site | Public web page | Unclear | Indicated |

openbanking.paysolo.net | Open-banking gateway | Live endpoint + SimilarWeb data | Unclear | Corroborated |

| Pagagate.com | Referrer into Paysolo gateway | SimilarWeb screenshot | Unknown | Corroborated |

| Urbenics.com | Casino-facing gateway and Paysolo feeder | SimilarWeb screenshot | Unknown | Corroborated |

oba.revolut.com | Dominant outgoing destination from Paysolo gateway | SimilarWeb screenshot | UK / EEA | Corroborated |

| Offshore casino domains | Source environment | SimilarWeb screenshots / FinTelegram observations | Offshore | Corroborated |

Compliance Analysis

1. The Paysolo Setup Looks Like A Conversion Layer

Paysolo’s public model — virtual IBANs, SEPA/SWIFT intake, fiat-to-crypto conversion, external wallet withdrawals — is exactly the kind of infrastructure that can be legitimate in ordinary crypto use, but highly sensitive when connected to gambling traffic.

2. Pagagate And Urbenics Create The Casino-Rail Context

The uploaded screenshots show that Pagagate and Urbenics are not random referrers. Urbenics’ referring domains include multiple casino-style brands, and Pagagate’s outgoing traffic includes both openbanking.paysolo.net and aphrodite1.casino. That pattern suggests gateway-to-casino proximity.

3. Revolut Appears As The Downstream Bank API

The most important technical signal is that oba.revolut.com reportedly accounts for 78.69% of outgoing traffic from openbanking.paysolo.net. That makes Revolut not merely one bank among many, but apparently the dominant outgoing destination in the observed SimilarWeb sample.

4. Open Banking May Weaken Merchant Transparency

Traditional card acquiring has MCC codes, merchant descriptors, acquirer monitoring, chargeback patterns, and gambling-blocking logic. Open-banking chains can be more opaque if the bank sees a customer-authorised transfer but not the full upstream commercial context.

That is why the Paysolo case is important: it shows how an offshore casino user journey may be transformed into an open-banking or fiat-to-crypto transaction before hitting the bank layer.

Open Questions To Paysolo

- Is Paysolo O.O.D. the legal operator of

paysolo.netandopenbanking.paysolo.net? - What is the relationship between Paysolo O.O.D., Paysolo Ltd., Newtech Mobile, and any PaySolo-branded gateway domains?

- Does Paysolo provide services to Pagagate.com or Urbenics.com?

- Does Paysolo onboard or process flows for online casinos, betting sites, affiliate networks, or gambling-related gateways?

- Does Paysolo classify Pagagate and Urbenics as high-risk merchants or technical partners?

- Does Paysolo screen upstream domains before processing open-banking or vIBAN transactions?

- How many transactions in March 2026 originated from Pagagate and Urbenics?

- Does Paysolo pass merchant-origin information to Revolut or other downstream banks?

- Are fiat-to-crypto conversions allowed when the source transaction originates from gambling-related activity?

- Has Paysolo filed suspicious-activity reports or blocked transactions connected to casino gateways?

Open Questions To Revolut

- Does Revolut monitor

openbanking.paysolo.netas a high-risk open-banking counterparty? - Does Revolut receive upstream origin data showing whether payments originate from Pagagate, Urbenics, or casino domains?

- Does Revolut classify Paysolo-related flows as crypto, open banking, gambling, merchant payment, or account-to-account transfer?

- Has Revolut restricted, reviewed, or reported any flows involving Paysolo, Pagagate, or Urbenics?

- Does Revolut’s gambling-blocking logic cover open-banking payments routed through VASP or vIBAN intermediaries?

Conclusion

The Paysolo case provides the first concrete follow-up node in FinTelegram’s Revolut Rail Atlas.

The apparent structure is simple but powerful: anonymous casino-facing gateways feed into openbanking.paysolo.net; Paysolo’s gateway then sends most visible outgoing traffic to Revolut’s Open Banking API.

This does not prove that Paysolo or Revolut knowingly facilitate illegal gambling. But it demonstrates the precise compliance risk FinTelegram has warned about: multi-layered open-banking rails can transform casino-originated money flows into bank/API traffic that may appear cleaner than the underlying transaction reality.

For regulators, the issue is clear: open banking must not become the new blind spot for illegal gambling and crypto conversion rails.

Whistle42 Call

FinTelegram invites payment insiders, Paysolo users, Revolut compliance staff, casino operators, open-banking providers, gateway developers, and affected players to submit information confidentially via Whistle42. We are especially interested in API logs, merchant contracts, settlement records, payment descriptors, screenshots, VASP onboarding files, Revolut transaction records, and internal risk alerts involving Paysolo, Pagagate, Urbenics, or casino-linked open-banking flows.

{kind=link}