New whistleblower evidence reviewed by FinTelegram appears to show a Dutch-facing casino deposit flow moving from Kingdomcasino into openbanking.paysolo.net, where users are offered banks including Revolut, Rabobank, N26, SNS Bank and Wise. The payment page itself states that the user agrees to allow “Pellopay Finance LTD partners Yapily Connect” to initiate the payment. The evidence strengthens FinTelegram’s working hypothesis that anonymous gateways, open-banking providers, fiat/crypto bridge operators and Revolut’s Open Banking API may form a layered casino-payment corridor.

Key Findings

- Video evidence shows a live casino deposit journey. The uploaded video begins on

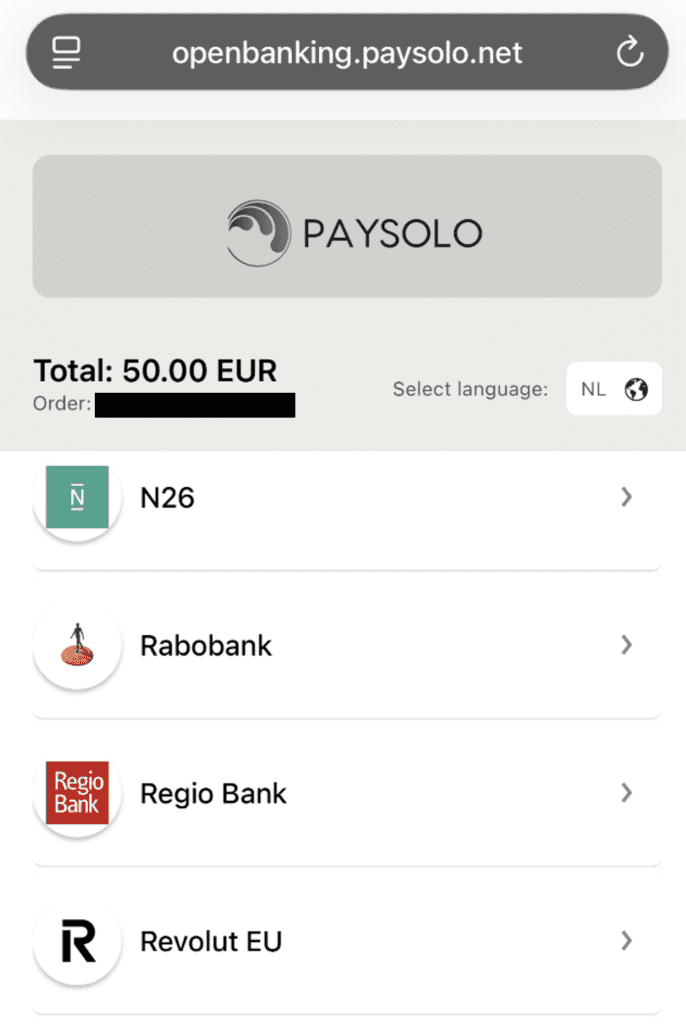

kingdomcasino6.io, showing a €50 deposit page in Dutch with card, iDEAL, instant bank transfer and crypto options. - The user is redirected to Paysolo. The payment flow moves to

openbanking.paysolo.net, displaying the Paysolo logo, order number 2026040239881439, total €50.00, and a Dutch-language bank-selection interface. - Revolut EU is offered as a bank option. The Paysolo page lists N26, Rabobank, Regio Bank, Revolut EU, SNS Bank and Wise.

- Pellopay and Yapily appear in the payment consent text. The footer states that by using the service, the user agrees to allow Pellopay Finance LTD partners Yapily Connect to initiate the payment.

- Yapily publicly markets open-banking infrastructure for payments and lists iGaming as a supported solution category. Yapily’s website says it supports payments and data across consumer and business accounts, and specifically describes open-banking payments “built for iGaming.”

- Open Banking Limited lists Yapily Connect Ltd as an open-banking regulated provider connecting to banks across 19 countries.

- NewTech Mobile SIA appears relevant to Impaya. Public Latvian company data identifies NewTech Mobile SIA, registration number 40103709254, at Skanstes iela 7 k-1, Riga, matching the whistleblower’s stated EU representative information.

- Impaya publicly presents itself as an e-commerce payment-solution provider. Its website describes a “full-package solution” for businesses.

Read our Revolut Rail Atlas reports here.

The Payment Flow Observed

Based on the uploaded video and screenshot evidence, the observed chain appears as follows:

Kingdomcasino6.io → payment interface / possible Impaya-linked URL layer → openbanking.paysolo.net → Pellopay / Yapily Connect consent layer → bank selection → Revolut EU and other banks

This does not yet prove contractual responsibility by every named party. But it does show a live user journey where a casino deposit flow ends at a Paysolo-branded open-banking bank-selection page and references Pellopay, Yapily Connect and Revolut EU as part of the payment environment.

From Kingdom Casino to Revolut: The Multi-Layered Payment Flow

The observed payment flow shows that openbanking.paysolo.net functions as a user-facing open-banking gateway, while Pellopay Finance LTD appears at the payment-consent layer as the payment initiator.

Casino

↓

Pagagate (entry gateway / cashier)

↓

Impaya (processing / routing layer)

↓

Aceiro (intermediate routing / alias layer)

↓

Paysolo (open banking UI gateway)

↓

Pellopay (payment initiator / backend PSP)

↓

Yapily (regulated Open Banking connector)

↓

Bank (Revolut, Rabobank, etc.)

The upstream routing chain — including Pagagate, Impaya and Aceiro — indicates a multi-layered payment orchestration structure in which different entities handle gateway access, routing, and execution separately. This fragmentation may obscure the original merchant context before the payment reaches regulated banking infrastructure.

The Paysolo payment page identifies “Pellopay Finance LTD” in the consent layer. Public materials on Pellopay.com describe Pellopay Finance Ltd as a Canada-registered payment-processing company offering API-based payment integration, payment links, bank transfers, digital wallets and support for methods including Revolut. This supports the assessment that Pellopay acts as a backend payment-processing or orchestration layer in the observed Paysolo open-banking flow, while Yapily Connect appears to provide the regulated open-banking connectivity.

If Impaya or related operators provide the gateway front-end, then the observable payment chain may be broader than Paysolo alone:

Casino brand → Impaya / Aceiro / gateway layer → Paysolo open banking → Pellopay / Yapily Connect → Revolut EU

Evidence & Confidence Table

| Entity / Rail Element | Observed Role | Evidence Type | Confidence |

|---|---|---|---|

| Kingdomcasino | Casino deposit origin | Uploaded video | Corroborated |

| Paysolo openbanking.paysolo.net | Bank-selection / Paysolo payment page | Uploaded video + screenshot | Confirmed in evidence |

| Revolut | Listed bank option | Uploaded screenshot/video | Confirmed in evidence |

| Pellopay Finance LTD | Named in payment-consent footer | Uploaded screenshot/video | Confirmed in evidence |

| Yapily Connect | Named as payment-initiation partner | Uploaded screenshot/video + public open-banking records | Corroborated |

| Impaya | Alleged URL/payment-flow layer | Whistleblower statement | Indicated |

| NewTech Mobile SIA | Alleged EU representative / Impaya-linked entity | Whistleblower statement + Latvian company record | Indicated |

| Aceiro | Alleged name in payment links | Whistleblower statement | Indicated |

Compliance Analysis

1. Open Banking Replaces Chargeback Logic

The whistleblower’s complaint highlights a key consumer-protection issue: where payments are made through open banking, the user may not have the same practical chargeback route as with card payments. That matters in gambling flows, where disputes, failed withdrawals, and merchant opacity are frequent.

2. Yapily’s iGaming Positioning Creates A Compliance Question

Yapily openly presents iGaming as one of its supported solution categories and says its open-banking payments can cut fees and improve first-time player deposit success. That is not improper by itself. Licensed iGaming is a legitimate industry. But if the same rails appear in unlicensed or offshore casino environments targeting Dutch users, the compliance question becomes acute.

3. Revolut Appears As A Downstream Bank Option

The Paysolo page offers Revolut EU among the selectable banks. That does not prove Revolut has a direct relationship with the casino or Paysolo. But it shows that the player journey can be routed toward Revolut through an open-banking interface.

4. Paysolo Sits At The Critical Conversion Point

Paysolo’s presence is significant because earlier Rail Atlas findings already placed openbanking.paysolo.net in a traffic corridor involving Pagagate, Urbenics and oba.revolut.com. The new video now adds transaction-level context: a casino deposit journey visibly reaches the Paysolo bank-selection layer.

Questions To Send To The Parties

To Paysolo

- Is Paysolo the operator of

openbanking.paysolo.net? - Does Paysolo process payments for Kingdomcasino6.io, Luckzie.io, Jinxcasino.io, Pagagate, Urbenics, Impaya, Aceiro or Pellopay?

- Does Paysolo screen upstream merchants for gambling activity and Dutch licensing status?

To Pellopay

- What is Pellopay Finance LTD’s role in the observed Paysolo payment page?

- Is Pellopay the merchant, payment initiator, technical service provider or contractual PSP?

- Does Pellopay onboard or monitor casino-related merchants?

To Yapily

- Was Yapily Connect involved in the payment initiation shown in the uploaded evidence?

- Does Yapily allow its infrastructure to be used for offshore casino deposits targeting Dutch players?

- What upstream merchant information is passed to banks such as Revolut?

To Revolut

- Does Revolut detect that these open-banking flows originate from casino deposit journeys?

- Does Revolut monitor Paysolo, Pellopay, Impaya, Pagagate or Urbenics as high-risk open-banking corridors?

- Are payments to unlicensed casino operators blocked when they arrive through open-banking intermediaries?

To Impaya / NewTech Mobile / Aceiro

- What role do Impaya, NewTech Mobile and Aceiro play in the observed payment links?

- Are these entities providing gateway or cashier technology for offshore casinos?

- Who is the merchant of record in the observed transaction flow?

Conclusion

The new evidence gives FinTelegram a stronger transaction-level case study. It shows a casino deposit flow reaching Paysolo, presenting Revolut EU as a bank option, and naming Pellopay Finance LTD and Yapily Connect in the payment-consent layer.

This does not prove knowing facilitation by Revolut, Yapily, Paysolo, Pellopay or Impaya. But it does show how open banking can be embedded inside casino-payment journeys in ways that may obscure the underlying merchant, weaken chargeback protections, and shift risk into account-to-account payment rails.

For regulators, the message is simple: the casino-payment perimeter has moved from card acquiring to open banking.

{kind=link}