In the rapidly evolving landscape of cryptocurrency regulation, the European Union’s Markets in Crypto-Assets Regulation (MiCAR) emphasizes the need for maximum transparency, particularly for stablecoin issuers. The former Payvision founder and COO, Gijs op de Weegh, founder and CEO of the new stablecoin issuer StablR, recently presented a bold piece of partially accurate biographical information that can mislead potential investors.

The Presented Narrative

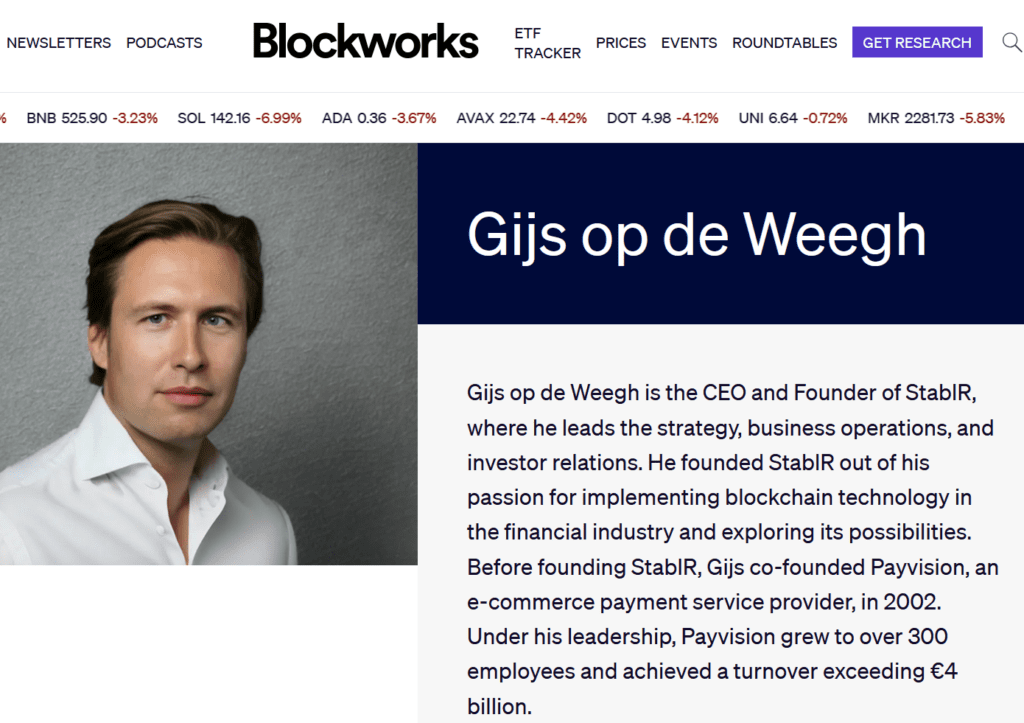

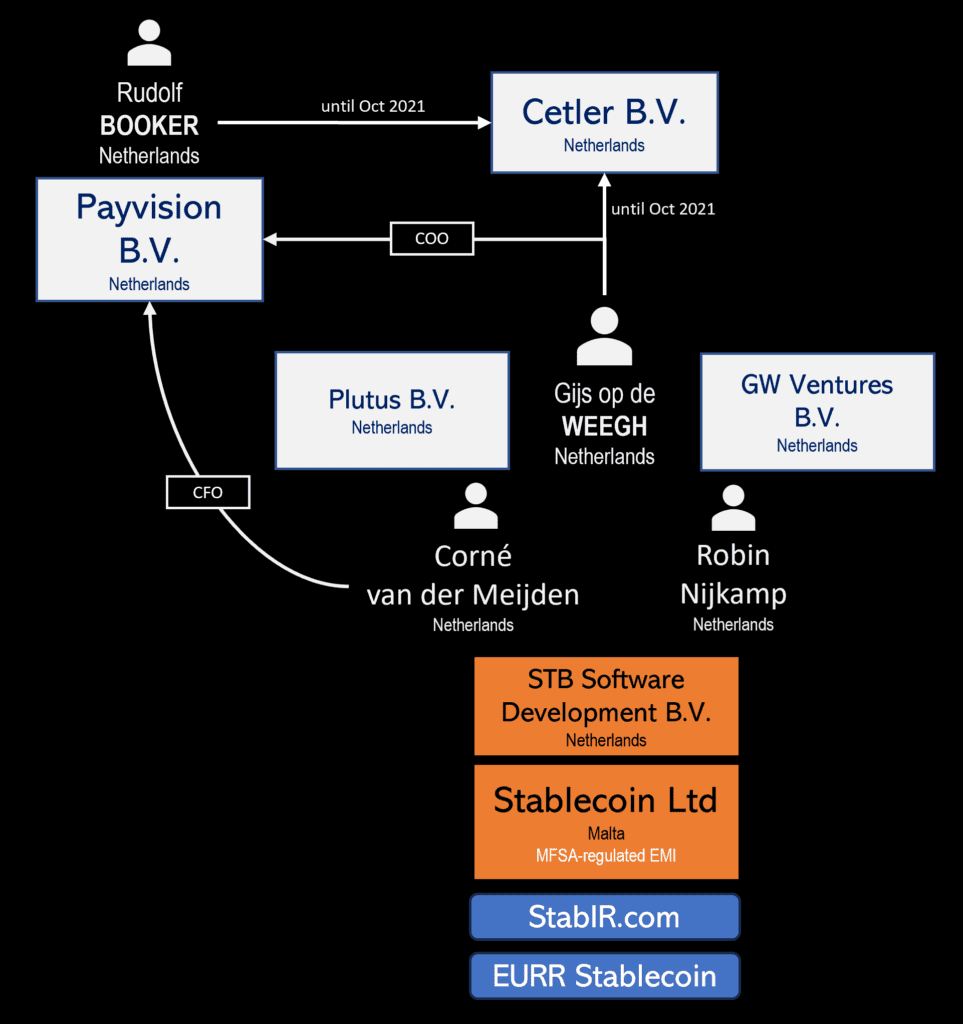

Gijs op de Weegh, a Dutch national, is the CEO and founder of the stablecoin issuer StablR, where he oversees strategy, operations, and investor relations.

On August 2, 2024, op de Weegh authored an article on Blockworks, expressing his enthusiasm for the new EU crypto regulation MiCAR, highlighting its potential benefits for stablecoin issuers. While his positive outlook on regulatory developments is commendable, the author’s biography (pictured left) accompanying his article paints a dramatically incomplete picture of his professional history.

In this short biography, Payvision, under the leadership of Gijs op de Weeg, is presented as a billion-dollar company. This sounds impressive, but is only half the truth and is therefore likely to give a false impression of the the author and StablR CEO.

The Real Payvision Legacy

Op de Weegh’s biography states that he co-founded Payvision, a high-risk payment processor, in 2002. He proudly notes that under his leadership, Payvision grew to over 300 employees and achieved a turnover exceeding €4 billion. At first glance, this seems like a testament to his successful leadership and industry acumen. However, this narrative omits significant and critical details about Payvision’s controversial past.

Under op de Weegh’s tenure as Chief Operating Officer (COO), Payvision was deeply embroiled in money laundering activities and the facilitation of cybercrime. The Dutch financial market regulator, De Nederlandsche Bank (DNB), conducted an investigation that resulted in charges against Payvision for violating financial laws and money laundering regulations. Law enforcement agencies imposed substantial penalties on Payvision and its responsible executives.

The Omitted Facts & FinTech Cowboys

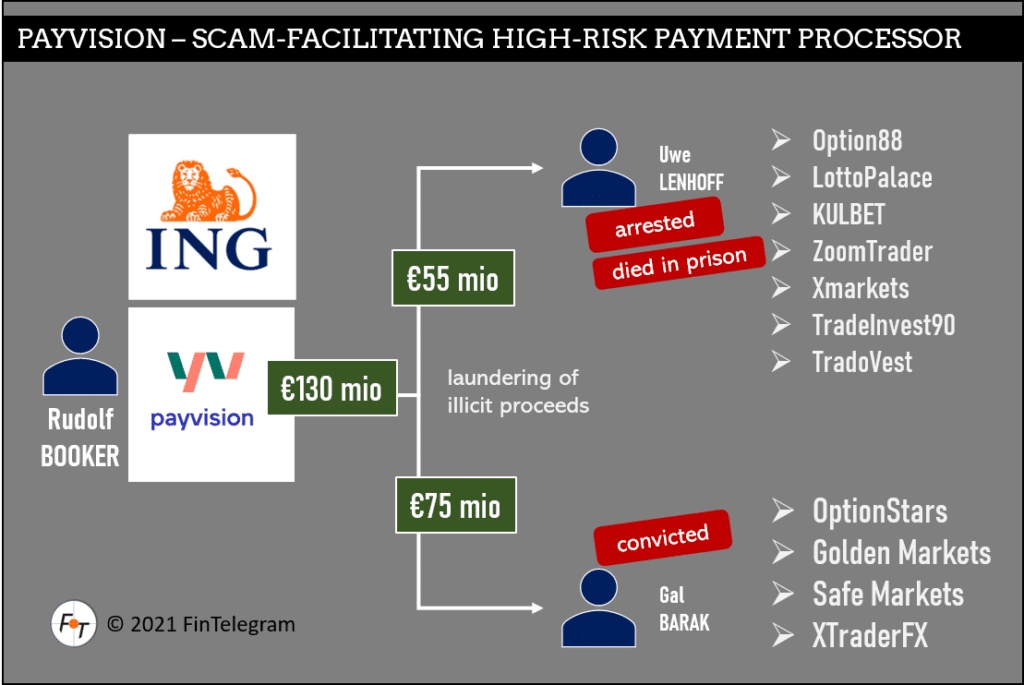

Crucially, Gijs op de Weegh signed the contracts with merchants involved in fraudulent schemes. One notable client was Gal Barak, an Israeli national convicted of money laundering and investment fraud. Barak’s companies, onboarded by Payvision under op de Weegh’s oversight, defrauded tens of thousands of small investors, funneling hundreds of millions of euros through illicit activities.

Another cybercrime mastermind who worked closely with Payvision was the German Uwe Lenhoff, who died in prison in 2020. Although his criminal record already included several fraud convictions, Lenhoff became a reseller of Payvision, operated a network of scams, such as Option888, via the Veltyco Group, and defrauded tens of thousands of victims.

Despite these severe issues, the founders sold Payvision to ING in 2018 for a valuation of €360 million. However, the legacy of misconduct and regulatory violations forced ING to announce the closure of Payvision in October 2021, a mere three years post-acquisition. With this failed fintech transaction, ING lost hundreds of millions.

Payvision and its parent company, ING, are currently being sued by the victims of Barak and Lenhoff. The victims accuse the two of facilitating the fraud schemes and thus contributing to the fraud. The findings of the law enforcement authorities support the victims’ claims.

The Dutch investigative platform Follow the Money portrayed the then-CEO Rudolf Booker and Gijs op de Weegh as FinTech cowboys (see picture above) who would know how to do it (read our report here).

Read our Payvision reports here.

The Need for Comprehensive Transparency

The MiCAR framework mandates stringent transparency for stablecoin issuers, aiming to protect investors and maintain market integrity. In this context, the selective disclosure of op de Weegh’s professional history is troubling. Potential investors and stakeholders in StablR deserve a complete and accurate account of his background, including the full scope of his involvement with Payvision.

While op de Weegh’s achievements and insights into the benefits of MiCAR are valuable, omitting the controversial aspects of his career could mislead investors. Full transparency is not just a regulatory requirement but a fundamental aspect of building trust in the volatile and nascent crypto market.

Conclusion

As MiCAR continues to shape the regulatory environment for crypto-assets in the EU, industry leaders like Gijs op de Weegh must provide comprehensive and truthful accounts of their professional histories. The partial biography presented may fulfill the need for a positive public image, but it falls short of the transparency required by both regulators and investors. FinTelegram urges all stakeholders to demand full disclosure to ensure informed decision-making in the crypto ecosystem.

{kind=link}