Revolut has announced on X that it is now a “fully licensed bank” in the UK, confirming that the PRA has lifted the restrictions attached to its 2024 authorisation and allowed the launch of Revolut Bank UK Ltd. The move is a major strategic milestone for the fintech group, but it does not end the regulatory scrutiny around how Revolut’s rails appear across high-risk crypto and offshore-gambling flows.

Key Findings

- Revolut says it is now a fully licensed bank in the UK; the PRA has approved its exit from mobilisation.

- The UK licence enables FSCS-protected deposit accounts and opens the door to broader lending products.

- Revolut’s latest official annual-report metrics show 52.5 million retail customers at year-end 2024, £3.1 billion revenue, £1.089 billion profit before tax, and £1 trillion transaction volume; more recent company statements say it now serves more than 70 million customers globally.

- In the EU, Revolut combines a Lithuanian bank, a Lithuanian MiFID investment firm, and a Cyprus MiCA CASP entity.

- FinTelegram continues to see Revolut embedded in fiat-to-crypto and offshore-casino payment chains, including via Onramper and open-banking layers.

The Compliance Report

Compliance Situation in UK

Revolut, founded in 2015, has grown from a payments app into one of Europe’s largest fintech groups. Official 2024 figures show 52.5 million retail customers, £3.1 billion in revenue, £1.089 billion in profit before tax, £790 million net profit, and £1 trillion transaction volume. In March 2026, Revolut said it serves more than 70 million customers globally.

The immediate significance of the UK licence is straightforward: Revolut can now operate as a full UK bank rather than an e-money institution plus a bank-in-waiting. Its UK bank can offer eligible customers FSCS protection on deposits and can expand into current accounts, credit, and other balance-sheet products. That materially upgrades customer protection, funding flexibility, and regulatory credibility in its home market.

Read our Revolut reports here.

Compliance Situation in EU

In the EU, however, Revolut remains a multi-entity regulatory stack. Banking services are anchored in Revolut Bank UAB in Lithuania, licensed by the ECB and regulated by the Bank of Lithuania; since 2024, Revolut’s Lithuanian banking group has been under direct ECB supervision as a significant institution. Investment services are provided by Revolut Securities Europe UAB, a Lithuanian investment firm subject to MiFID II. Crypto services for EEA clients are now routed through Revolut Digital Assets Europe Ltd in Cyprus, licensed as a CASP under MiCA. Revolut’s own rules also state that tokens qualifying as MiFID II financial instruments are excluded from Revolut X, showing the fault line between MiCA crypto services and securities regulation.

High-Risk Payment Facilitator

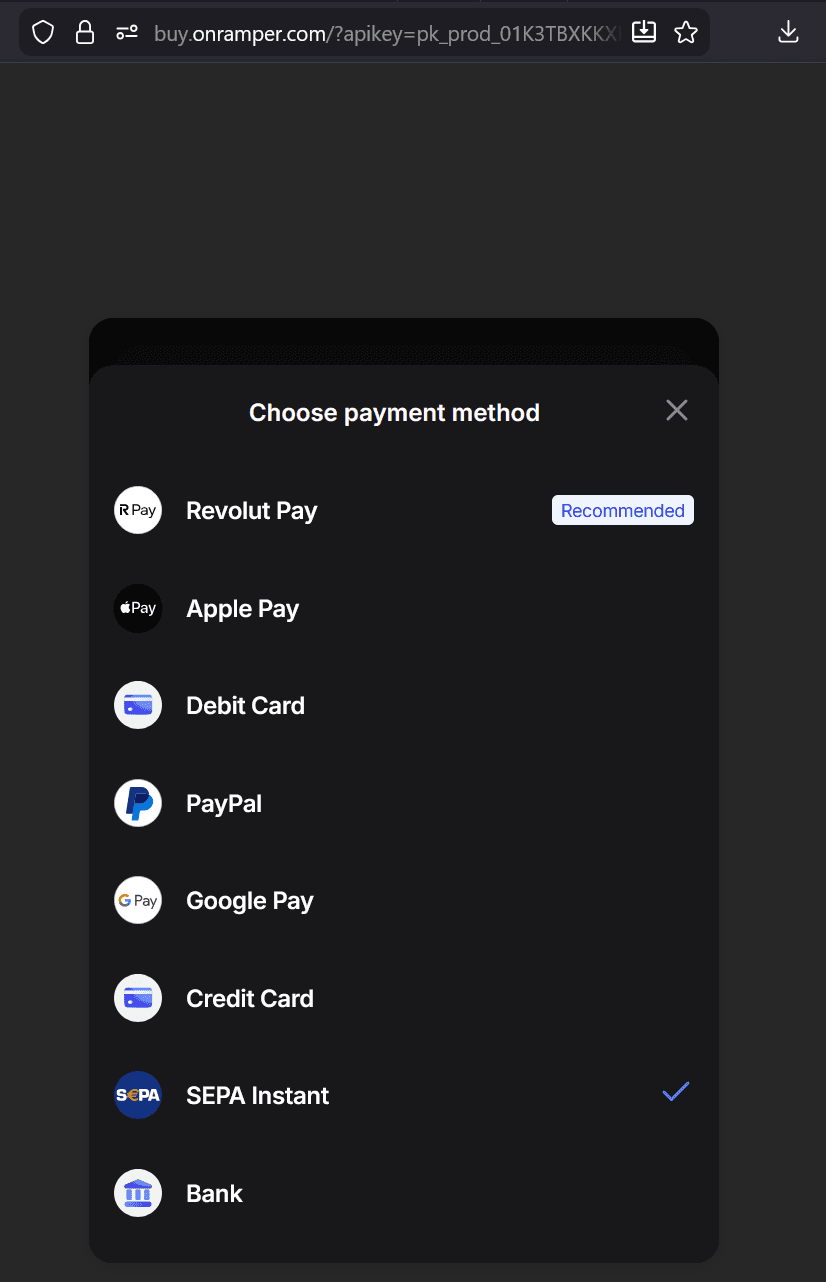

From a FinTelegram compliance perspective, that stronger licence perimeter in the UK does not neutralise the risk created by Revolut’s recurring appearance in high-risk rails. Onramper publicly lists Revolut among its ramp providers, and Onramper announced an Axiom integration for fiat-to-crypto access.

FinTelegram recently found Revolut presented as a primary rail in Axiom-related “Buy Crypto” journeys, while in the casino segment Revolut-linked rails and open-banking layers repeatedly surface in offshore payment architectures, often alongside intermediaries such as Yapily-type providers.

The compliance issue is therefore not Revolut’s licence status alone, but whether its controls sufficiently detect and restrict repeated exposure to unregulated brokers, DeFi perimeter-risk flows, and offshore gambling conversion chains.

Compliance Conclusion

Revolut’s full UK banking licence is a genuine milestone. But the stronger the licence, the stronger the expectation that its AML, merchant-risk, transaction-monitoring, and partner-oversight frameworks will prevent its rails from becoming repeat infrastructure for regulatory arbitrage.

Revolut Key Data

| Field | Details |

|---|---|

| Brand | Revolut |

| Main domain | revolut.com |

| Founded | 2015 |

| Current customer base | 70m+ globally (company, Mar 2026) |

| 2024 revenue | £3.1bn |

| 2024 profit before tax | £1.089bn |

| 2024 transaction volume | £1tn |

| UK entity | Revolut Bank UK Ltd / PRA-regulated UK bank launch; Revolut Ltd remains FCA-authorised EMI (FRN 900562) |

| EU banking entity | Revolut Bank UAB, Lithuania, ECB/Bank of Lithuania supervised |

| MiFID II entity | Revolut Securities Europe UAB, Lithuania |

| MiCA entity | Revolut Digital Assets Europe Ltd, Cyprus, CASP licence 001/2025 |

Call to Whistleblowers

If you have information on Revolut’s role in high-risk payment processing, open-banking routing, crypto on-ramping, offshore gambling, merchant monitoring, or AML escalation failures, contact FinTelegram confidentially.

{kind=link}