FinTelegram’s review of GoldenBet shows a diversified payment architecture around the Santeda Group: card deposits evidenced through Payabl, wallet deposits showing Santeda International Limited as beneficiary via MiFinity, and an Open Banking rail through Bilderlings → Yapily Connect → Revolut’s Open Banking API. This is no longer a single-PSP complaint story. It is a Rail Atlas case study in how offshore casino operators maintain EU-facing payment continuity across cards, wallets, crypto, and account-to-account banking rails.

Key Findings

- GoldenBet offers a multi-rail cashier. The uploaded screenshot shows deposit options for cards, MiFinity, Open Banking, Google Pay, Jetonbank, eZeeWallet, Bitcoin and Ethereum.

- Payabl processed card deposits to Santeda. The GDPR transaction list disclosed by Payabl shows successful Mastercard transactions to SantedaInternationalLimited totaling €565.00.

- Payabl refused refund action. Payabl told the player that it provides services to direct clients and could not execute a refund because the player had no direct contractual relationship with Payabl.

- MiFinity confirms Santeda as beneficiary. The uploaded MiFinity simulation shows a €50 deposit to Santeda International Limited.

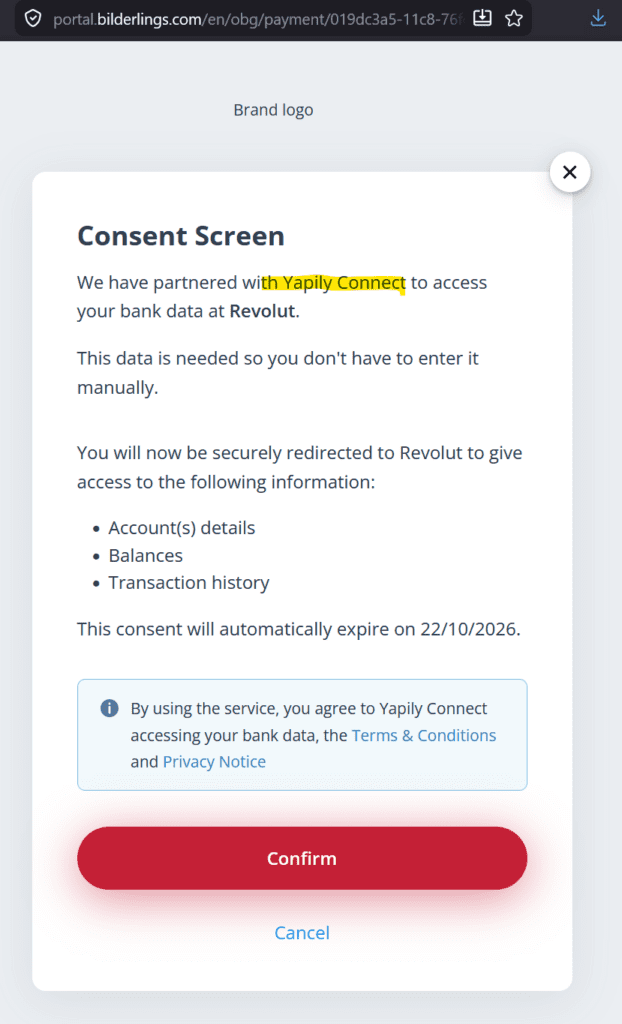

- Open Banking rail confirmed. The screenshots show GoldenBet’s Open Banking option routing into portal.bilderlings.com, then to a bank-selection screen listing Revolut, then a consent screen referencing Yapily Connect, and finally

oba.revolut.com. - Bilderlings is an FCA-authorised EMI. The FCA Register lists Bilderlings Pay Limited as an authorised electronic money institution since 1 May 2018.

- Yapily Connect is a regulated Open Banking provider. Yapily states that Yapily Connect Ltd is FCA-regulated and Yapily Connect UAB is regulated by the Bank of Lithuania.

- Payabl’s Cyprus AML history matters. The Central Bank of Cyprus register records a €350,000 fine against Payabl. Cy Ltd under Cyprus AML legislation, announced on 3 October 2025, with judicial review pending.

The GoldenBet Rail Map

GoldenBet / Santeda casino cashier

│

├── Rail 1: Card deposits

│ GoldenBet card option

│ → Payabl card-processing / acquiring layer

│ → GPay card-processing

│ → Merchant: Santeda International Limited

│ → GDPR transaction list: shows successful transactions

│

├── Rail 2: Wallet deposits

│ GoldenBet MiFinity option

│ → MiFinity

│ → Jetonbank

│ → eZeeWallet

│ → Beneficiary: Santeda International Limited

│

├── Rail 3: Open Banking deposits

│ GoldenBet “Deposit with Open Banking”

│ → portal.bilderlings.com / OBG payment layer

│ → Bilderlings bank-selection interface

│ → Yapily Connect consent screen

│ → oba.revolut.com

│ → Revolut authorisation

│

└── Rail 4: Crypto deposits

GoldenBet several cryptocurrency options

→ direct wallet transfer via wallet address

→ high-risk value-transfer channel

Analysis: The Multi-Rail Architecture

GoldenBet’s cashier does not depend on one payment provider. It presents a resilient payment stack across cards, wallet payments, Open Banking and crypto. That architecture matters because it reduces dependency on any single rail and allows deposits to continue even if one channel becomes disputed, blocked, or scrutinised.

The Payabl evidence is documentary: Payabl’s own GDPR disclosure lists multiple successful card transactions to SantedaInternationalLimited in August 2025. Payabl’s complaint team then rejected the player’s refund request on the basis that the player was not Payabl’s direct customer.

Read the GoldenBet/Payabl GDPR case here.

The MiFinity evidence independently supports the same payment-agent structure: the simulation screenshot shows the deposit beneficiary as Santeda International Limited.

The new Open Banking evidence adds the systemic Rail Atlas angle. The user journey moves from GoldenBet into a Bilderlings-hosted payment page, then to a Yapily Connect consent screen, and then to Revolut’s oba.revolut.com authorisation layer. Revolut’s own help pages explain that Open Banking requires explicit approval and allows regulated third-party providers to access data or initiate payments.

Why The Bilderlings/Yapily/Revolut Rail Matters

The screenshots (left) show a clean Open Banking chain:

GoldenBet

→ Bilderlings OBG payment page

→ “Choose your bank”

→ Revolut selected

→ Yapily Connect consent

→ Revolut authorisation at oba.revolut.com

This is sensitive because Open Banking payments can look like user-authorised account-to-account transfers rather than classic gambling card payments. That may reduce the visibility of merchant category codes and weaken chargeback-style consumer remedies.

Bilderlings’ FCA status and Yapily’s regulated Open Banking status do not remove the underlying compliance question: what upstream merchant context is visible, screened and passed through the chain?

Compliance Red Flags

| Red Flag | Why It Matters |

|---|---|

| Same casino, multiple rails | Demonstrates payment resilience, not incidental processing |

| Santeda clearly identified | Payabl and MiFinity evidence identify the beneficiary/merchant |

| Open Banking route to Revolut | Shows A2A banking rail for casino deposits |

| Yapily consent references bank data and Revolut | Confirms regulated Open Banking layer |

| Crypto options in cashier | Adds value-transfer and AML complexity |

| Payabl AML penalty context | CBC already sanctioned Payabl under AML law in 2025 |

| No direct-customer refund defence | PSP accountability gap where player is harmed but not contractual client |

Interpretation In The Rail Atlas Narrative

The GoldenBet case is a flagship Rail Atlas case because it illustrates the modern offshore-casino payment perimeter:

regulated PSPs + wallet providers + Open Banking infrastructure + crypto rails + offshore casino operator

The crucial point is not that each rail is inherently unlawful. Cards, MiFinity, Bilderlings, Yapily and Revolut are all legitimate infrastructures. The issue is how these infrastructures appear to be combined to support casino deposits for an operator alleged to lack the relevant EU/German/Dutch licences.

Evidence & Confidence Table

| Rail Element | Observed Role | Evidence Type | Confidence Grade |

|---|---|---|---|

| GoldenBet | Casino cashier / originating merchant environment | Screenshot | Confirmed |

| Santeda International Limited | Merchant / payment agent | Payabl GDPR list + MiFinity screenshot | Confirmed |

| Payabl | Card-processing layer | GDPR disclosure + email correspondence | Confirmed |

| MiFinity | Wallet deposit channel | Screenshot simulation | Confirmed |

| Bilderlings portal.bilderlings.com | Open Banking gateway layer | Uploaded screenshots + FCA register | Corroborated |

| Yapily Connect | Open Banking connector | Consent screen + public regulatory status | Confirmed |

Revolut / oba.revolut.com | Bank authorisation endpoint | Uploaded screenshot | Confirmed |

Open Questions To GoldenBet / Santeda

- Which Santeda entity is the contractual merchant of record for GoldenBet deposits?

- Does Santeda International Limited act as payment agent for all Santeda casino brands?

- Which countries are targeted by GoldenBet, and what licences does it hold in each?

- Why are Open Banking and crypto rails offered to EU players if licensing is disputed?

- What responsible-gambling safeguards are applied across sister brands?

Open Questions To Payabl

- Was Santeda classified as a high-risk gambling merchant?

- What due diligence was conducted regarding Santeda’s German/EU licensing status?

- Did Payabl review the merchant after the player explicitly raised illegality and gambling-addiction concerns?

- Did Payabl file internal alerts or SARs?

- How does Payabl reconcile this case with the CBC’s €350,000 AML fine?

Open Questions To Bilderlings

- Is Bilderlings providing the Open Banking gateway shown in the GoldenBet flow?

- Who is Bilderlings’ direct client in this transaction chain?

- Does Bilderlings identify the upstream merchant as GoldenBet or Santeda?

- Does Bilderlings permit Open Banking payments for offshore casino operators?

- Are gambling merchants geo-blocked where no local licence exists?

Open Questions To Yapily

- What merchant-origin information is passed to Yapily in this flow?

- Does Yapily know that the Open Banking request originates from GoldenBet?

- Does Yapily screen iGaming merchants for target-market licensing?

- Does Yapily pass upstream merchant data to Revolut?

Open Questions To Revolut

- Does Revolut see GoldenBet or Santeda as the originating merchant?

- Does Revolut classify the transaction as gambling, generic Open Banking, or account-information/payment access?

- Does Revolut monitor Bilderlings/Yapily casino flows as high-risk?

- Are transactions blocked where casino operators lack local licences?

Conclusion

GoldenBet’s payment stack is not a single payment incident. It is a multi-rail architecture.

The Payabl GDPR disclosure documents card processing to Santeda. The MiFinity simulation identifies Santeda International Limited as beneficiary. The new screenshots show an Open Banking path via Bilderlings and Yapily into Revolut’s Open Banking API.

This makes GoldenBet a flagship Rail Atlas case: it demonstrates how offshore casinos can combine regulated payment institutions, wallet providers, Open Banking connectors and crypto rails into a resilient EU-facing cashier system.

The compliance question is now unavoidable: are regulated financial institutions and Open Banking providers adequately detecting, classifying and blocking casino flows where the operator lacks the required target-market licence?

Whistle42 Call

FinTelegram invites insiders from Santeda, Payabl, MiFinity, Bilderlings, Yapily, Revolut, casino affiliates, payment agents and compliance teams to submit evidence confidentially via Whistle42. We are seeking merchant onboarding files, Open Banking logs, payment descriptors, settlement records, licensing reviews, SAR filings, internal alerts and screenshots of live cashier flows.

{kind=link}