Editorial Note: After publication, Capitolio Inc. contacted FinTelegram and demanded removal of this report. Capitolio disputes FinTelegram’s interpretation and denies that its appearance as payee in the reviewed 1Go Casino payment flow constitutes any compliance violation. Capitolio also stated that it appears as the named payee in transactions processed through its Open Banking on-ramp infrastructure, describing this as standard technical architecture for such services. FinTelegram has reviewed the notice and made limited editorial adjustments: the category “Illegal Payment Services” was removed, a personal name was removed, and the term “scheme” was replaced by “operating model.” These changes do not affect the core finding: in the tested 1Go Casino Revolut/Yapily flow, CAPITOLIO INC. appeared as the visible payee. Capitolio has been invited to provide substantive answers regarding its role, merchant onboarding, upstream casino context, and relationship to the observed payment rail.

FinTelegram’s Revolut Rail Atlas review of 1Go Casino identified CAPITOLIO INC. as the visible payee in a tested Revolut/Yapily open-banking casino deposit flow. Capitolio presents itself as a Canadian MSB offering open-banking, fiat-to-crypto, payout, and digital-asset infrastructure — including for the “Gaming & Digital Economy” segment. This raises the central compliance question: why does a player deposit initiated inside an offshore casino cashier end up as an open-banking payment to a Canadian payment and crypto-infrastructure entity?

Executive Summary

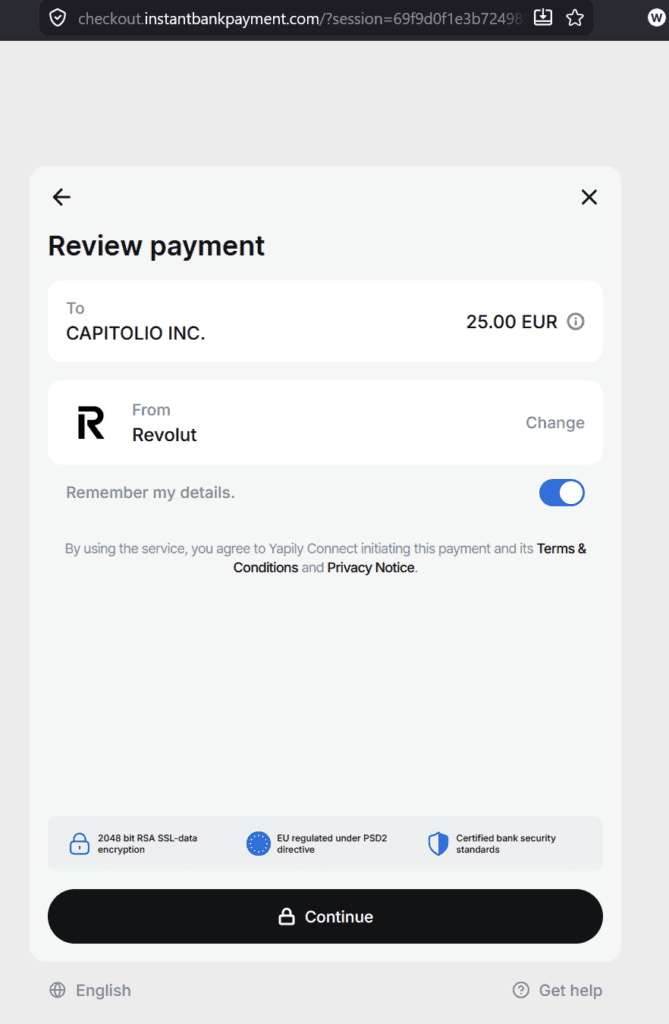

FinTelegram’s 1Go Casino payment-rail review exposed a layered casino-payment structure involving open banking, crypto infrastructure, changing payee names, and regulated chokepoints. In the tested Revolut/Yapily rail, the user journey started inside the 1Go Casino cashier and moved through BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily Connect UAB, and finally Revolut OBA. The payment-review screen then showed the visible beneficiary as CAPITOLIO INC.

Read our 1Go Payment Rails analysis here.

This is significant. Capitolio is not presented as the casino brand, not as 1Go Casino, and not as the apparent Curaçao casino operator Galaktika N.V. Instead, Capitolio’s website presents the company as an Alberta-incorporated Canadian MSB registered with FINTRAC under number M24928320, with stated activities including virtual currency exchange, virtual currency transfer, and money transfer. Capitolio also markets open-banking payments, account-to-account bank payments, fiat-to-crypto and crypto-to-fiat infrastructure, payouts, card acquiring, OTC liquidity, embedded widgets, and services for Gaming & Digital Economy platforms.

FinTelegram’s assessment is direct: in the tested 1Go flow, Capitolio was not merely a background technology provider. It was the named beneficiary of player funds at the Revolut/Yapily authorisation layer.

Whether Capitolio acted as merchant of record, payment agent, collection agent, settlement intermediary, crypto on/off-ramp provider, or processor for another upstream party requires clarification. But its appearance as payee is not a neutral technical detail. It is the compliance story.

Key Findings

- CAPITOLIO INC. appeared as the visible payee in the tested 1Go Casino Revolut/Yapily open-banking deposit flow.

- The payment originated inside the 1Go Casino cashier but, after several gateway layers, reached a Revolut/Yapily payment-review screen showing CAPITOLIO INC. as beneficiary.

- Capitolio presents itself as a Canadian MSB. Its regulatory-information page identifies CAPITOLIO INC. as an Alberta corporation with Corporate Access Number 2025599024, registered address in Calgary, and FINTRAC MSB number M24928320.

- Capitolio’s stated registered activities are virtual currency exchange, virtual currency transfer, and money transfer. These are listed on Capitolio’s own regulatory-information page.

- Capitolio markets itself as infrastructure for open banking, crypto conversion, card acquiring, payouts, and embedded payment widgets. Its website describes open-banking payments, account-to-account payments, fiat-to-crypto flows, card acquiring, payout infrastructure, on-ramp/off-ramp services, and OTC liquidity.

- Capitolio explicitly targets “Gaming & Digital Economy.” Its website says it enables players and users to fund accounts, purchase digital assets, and withdraw earnings through integrated payment and conversion infrastructure.

- Capitolio says it is not a bank, payment institution, or investment firm. Its regulatory page states that it does not accept deposits, does not provide investment services, and that funds transferred through Capitolio are not covered by CDIC protection.

- Capitolio’s public beneficial ownership remains unclear. The public pages reviewed disclose legal entity, address, MSB registration, services, and compliance claims, but do not disclose ultimate beneficial owners or controlling persons.

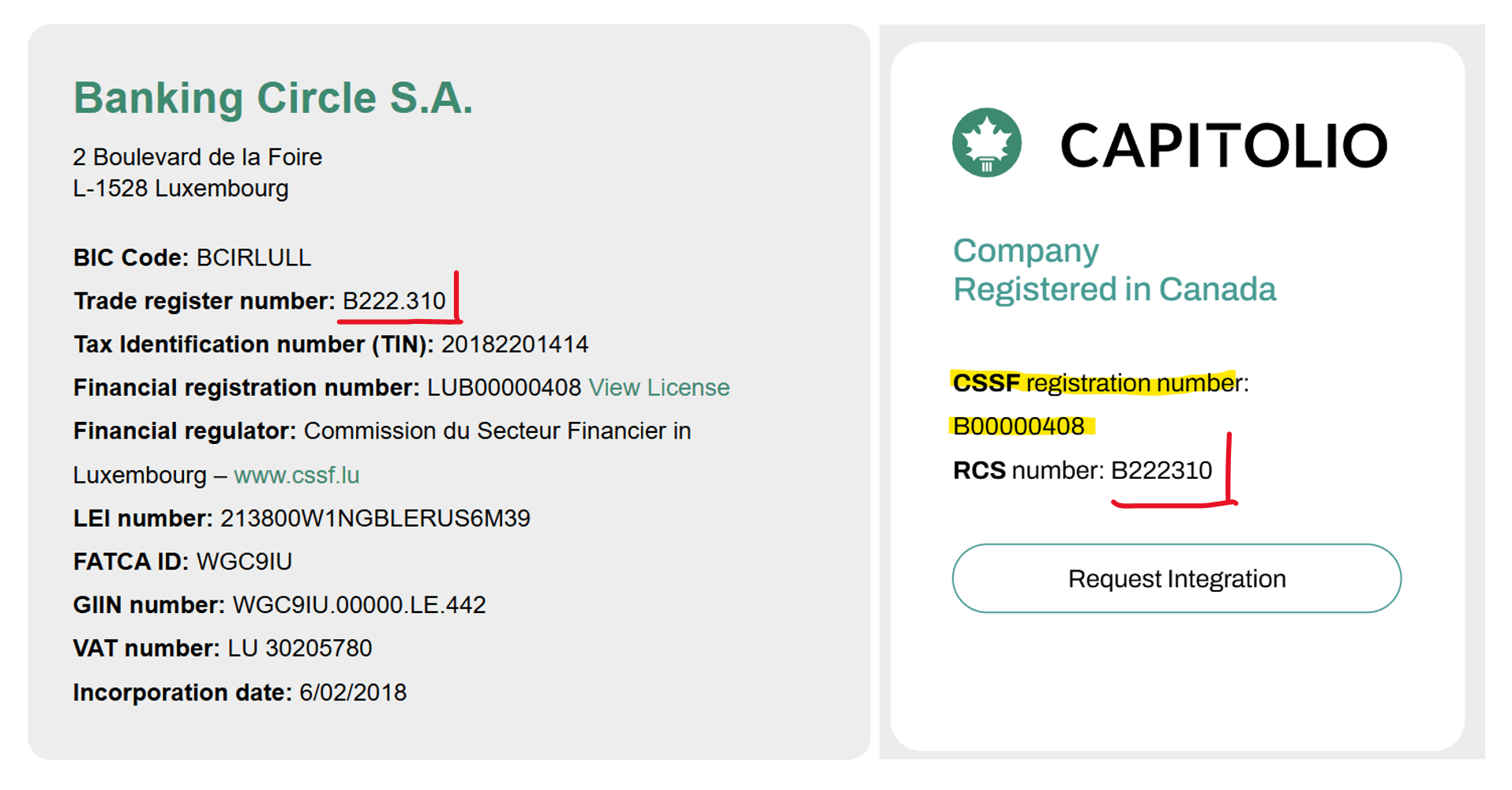

- Capitolio’s website contains an unexplained CSSF/RCS footer issue. Capitolio pages display CSSF registration number B00000408 and RCS number B222310, while the same identifiers appear on Banking Circle’s official regulatory-information page. Capitolio should clarify why those Luxembourg banking identifiers appear on its Canadian MSB website.

Read our Revolut Rail Atlas reports here.

Source Discipline: What Is Confirmed, What Is Inferred, What Remains Open

| Category | Status | Evidence / Comment |

|---|---|---|

| CAPITOLIO INC. appeared as payee in 1Go Casino rail | Confirmed from FinTelegram test evidence | Screenshot from the tested Revolut/Yapily payment-review screen showed CAPITOLIO INC. as beneficiary. |

| 1Go payment originated inside casino cashier | Confirmed from FinTelegram test evidence | The user journey began at the 1Go Casino deposit interface. |

| Capitolio legal entity and Alberta registration details | Confirmed from Capitolio disclosure | Capitolio identifies CAPITOLIO INC., Alberta Corporate Access Number 2025599024, and Calgary address. |

| FINTRAC MSB number M24928320 | Confirmed from Capitolio disclosure; registry status should be independently verified before final publication | Capitolio discloses FINTRAC number M24928320. FINTRAC warns that registry details should be verified and that registration is not endorsement or licensing. |

| Capitolio’s business model | Confirmed from Capitolio disclosure | Open banking, account-to-account payments, fiat-to-crypto, crypto-to-fiat, payouts, OTC liquidity, embedded widgets. |

| Gaming and digital-economy targeting | Confirmed from Capitolio disclosure | Capitolio says it enables players/users to fund accounts, purchase digital assets, and withdraw earnings. |

| Capitolio’s exact role in the 1Go flow | Strong inference from payment evidence | Named payee status indicates apparent collection/payee role; merchant-of-record, processor, settlement, or agency role requires clarification. |

| Beneficial owners / controllers | Unresolved | Not disclosed in the public pages reviewed. |

| Contractual relationship with 1Go, Galaktika, BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily or Revolut | Unresolved | Requires contracts, onboarding files, settlement data, or responses from involved parties. |

| CSSF/RCS footer identifiers | Confirmed anomaly | Capitolio pages show identifiers also used by Banking Circle; no conclusion of relationship is drawn, but clarification is required. |

Summary Table: Capitolio Key Data

| Field | Information |

|---|---|

| Brand / name | Capitolio |

| Main domain | capitolio.io |

| Legal entity | CAPITOLIO INC. |

| Jurisdiction | Alberta, Canada |

| Alberta Corporate Access Number | 2025599024 |

| Registered address | 700-602 12 Ave SW, Calgary, Alberta, T2R 1J3, Canada |

| FINTRAC registration disclosed by Capitolio | M24928320 |

| Stated registered activities | Virtual Currency Exchange, Virtual Currency Transfer, Money Transfer |

| Stated products | Open banking, account-to-account payments, fiat-to-crypto on/off-ramp, payouts, card acquiring, OTC liquidity, embedded widgets |

| Target segments | Fintechs, marketplaces, exchanges, digital platforms, gaming and digital economy |

| Compliance tools disclosed | KYC/KYB review, AML/CFT programme, transaction monitoring, sanctions/PEP screening, blockchain analytics, SumSub biometric verification |

| Regulatory caveat | Capitolio states it is not a bank, payment institution, or investment firm; it does not accept deposits; funds are not CDIC-protected |

| Public UBO / executive information | Not identified in the public sources reviewed |

| 1Go Casino relevance | Appeared as visible payee in tested 1Go Casino Revolut/Yapily open-banking flow |

| Key compliance risk | Casino-origin payment, non-casino payee, open-banking endpoint, crypto/payment infrastructure, unclear merchant-of-record role |

| Website integrity issue | Capitolio pages show CSSF/RCS identifiers matching Banking Circle references |

The Capitolio Operating Model: Infrastructure, Not a Consumer Brand

The Capitolio case is important because it does not look like a traditional consumer-facing payment brand. Capitolio positions itself as backend infrastructure for platforms. Its website states that it provides regulated payment infrastructure, open-banking connectivity, and fiat-to-crypto on/off-ramp solutions for fintechs, platforms, and enterprises.

The operating model appears to combine several high-risk components:

| Component | Capitolio Positioning | Rail Atlas Relevance |

|---|---|---|

| Open banking / A2A payments | Account-to-account payments with bank authentication and instant settlement | Can be used to move player funds directly from bank accounts into platform ecosystems. |

| Fiat-to-crypto on-ramp | Users can purchase digital assets using bank accounts, cards, or local alternative methods | Creates a bridge between bank money and crypto-funded casino or gaming flows. |

| Crypto-to-fiat off-ramp | Digital assets can be converted into fiat and paid out to bank accounts | Relevant for settlement, withdrawals, and cash-out layers. |

| Payout infrastructure | Funds can be sent to bank accounts | Useful for platform withdrawals, partner payouts, refunds, or settlement structures. |

| Embedded widgets | Payment modules integrated into third-party platforms | Reduces visibility of the underlying processor for end-users. |

| Gaming & Digital Economy | Players/users can fund accounts, purchase digital assets, and withdraw earnings | Directly overlaps with the type of payment context observed in the 1Go Casino review. |

| MSB registration | Canadian FINTRAC registration, not bank/payment-institution status | Registration creates AML obligations but is not a prudential licence or endorsement. |

This is the core of the Capitolio scheme as observed by FinTelegram: Capitolio appears to provide infrastructure that can sit behind platforms and receive or move funds without being the consumer-facing merchant brand. In the 1Go case, that model becomes highly relevant because the consumer-facing merchant was a casino cashier, while the bank-facing payee was Capitolio.

The 1Go Casino Link: Where Capitolio Appears in the Rail

FinTelegram’s 1Go Casino payment-rail review reconstructed the following tested Revolut route:

1Go Casino cashier

→ pay.billblend.com/checkout

→ tx.segopay.com/payment

→ tryzto.com/ct/check

→ checkout.instantbankpayment.com

→ Yapily Connect UAB

→ Revolut OBA

→ Payee: CAPITOLIO INC.

The final Revolut/Yapily payment-review screen did not show the casino brand as the beneficiary. It did not show Galaktika N.V. It showed CAPITOLIO INC.

That makes Capitolio a central entity in the payment trail. In the tested transaction, Capitolio appears to be the entity designated to receive funds originating from a player deposit at 1Go Casino. Functionally and economically, this indicates an apparent collection/payee role in the casino deposit flow.

This is the core Rail Atlas concern: by the time the transaction reaches the regulated banking interface, the visible beneficiary is no longer the casino brand. The bank-facing layer sees a corporate payee. The player knows the money is being deposited into a casino account.

Red Flags

| Red Flag | Why It Matters |

|---|---|

| Casino-origin transaction | The payment began in a 1Go Casino deposit cashier. |

| Non-casino payee | CAPITOLIO INC. appeared instead of 1Go Casino or Galaktika N.V. |

| Open-banking endpoint | Revolut/Yapily was used as the final authorisation layer. |

| Payment-purpose dilution | The economic purpose was a casino deposit, but the visible payee was a payment/crypto infrastructure entity. |

| Gaming-targeted infrastructure | Capitolio markets services to the “Gaming & Digital Economy” segment. |

| Crypto on/off-ramp model | Fiat-to-crypto and crypto-to-fiat flows create elevated AML, source-of-funds, and transaction-monitoring risk. |

| UBO opacity | Public sources reviewed did not identify controlling owners or ultimate beneficial owners. |

| Regulatory ambiguity | FINTRAC registration is not a licence, prudential supervision, or endorsement. |

| Website integrity issue | Capitolio pages show CSSF/RCS identifiers that match Banking Circle’s Luxembourg regulatory identifiers. |

| Gateway layering | BillBlend, SegoPay, Tryzto, and InstantBankPayment appeared upstream of Yapily/Revolut in the tested flow. |

Legal Entity, Jurisdiction, and FINTRAC Status

Capitolio’s regulatory-information page identifies CAPITOLIO INC. as a company registered under Alberta’s Business Corporations Act, with Alberta Corporate Access Number 2025599024 and a registered address in Calgary, Alberta. It also states that Capitolio is registered with FINTRAC as an MSB under number M24928320, with registered activities of virtual currency exchange, virtual currency transfer, and money transfer.

Capitolio may disclose a FINTRAC MSB registration, but FINTRAC registration is not a banking licence, not prudential supervision, not an investment-firm licence, and not a statement that the business model is low-risk.

FINTRAC’s consumer guidance also states that FINTRAC regulates MSBs only within the framework of Canada’s AML law and does not assess their broader business practices, approve or cancel transactions, freeze funds, access customer accounts, or help customers recover funds.

The Regulatory Caveat: Not a Bank, Not a Payment Institution

Capitolio’s regulatory-information page states that Capitolio is not a bank, payment institution, or investment firm, does not accept deposits, and does not provide investment services. It also states that funds transferred through Capitolio are not covered by Canada Deposit Insurance Corporation protection.

This is important because Capitolio’s public product language looks like payment infrastructure: open banking, account-to-account payments, card acquiring, payouts, embedded widgets, and crypto conversion. Yet the same website disclaims bank/payment-institution status.

For FinTelegram, this is the classic boundary-zone profile: an entity offering regulated-looking payment and crypto infrastructure, while operating under an MSB-registration framework rather than a bank or payment-institution framework. When such an entity appears as payee in an offshore casino deposit flow, enhanced scrutiny is warranted.

AML/CFT Claims and Compliance Infrastructure

Capitolio’s AML/CFT policy summary says the company is subject to Canada’s Proceeds of Crime (Money Laundering) and Terrorist Financing Act and FINTRAC guidelines. It states that Capitolio’s services include fiat-to-crypto and crypto-to-fiat virtual currency exchange, virtual currency transfer, and money transfers.

The same policy summary describes a risk-based AML approach, customer identification, enhanced due diligence, sanctions screening, transaction monitoring, blockchain analytics, suspicious transaction reporting, recordkeeping, and staff training. Capitolio also says it uses biometric verification via SumSub and screens transactions against sanctions lists including UN, OSFI, EU and PEP databases.

That is relevant to the 1Go Casino finding. If Capitolio was the visible payee in a casino-origin deposit, its AML/CFT programme should have captured at least three critical risk signals:

- the upstream merchant context;

- the gambling-related payment purpose;

- the multi-layer gateway chain leading into the open-banking payment.

If Capitolio’s systems did not detect those risk signals, the issue is operational. If they did detect them and the flow was permitted anyway, the issue is more serious.

The Website Integrity Issue: Banking Circle Footer Data?

One unusual finding deserves attention. Capitolio pages contain footer references to “CSSF registration number: B00000408” and “RCS number: B222310.” Capitolio otherwise presents itself as a Canadian company registered in Alberta and as a FINTRAC MSB.

The same CSSF and RCS identifiers appear on Banking Circle’s official regulatory-information page (screenshot above), where they are presented as Banking Circle’s Luxembourg registration details.

FinTelegram does not conclude from this alone that Capitolio is connected to Banking Circle. The more immediate conclusion is a website-integrity and regulatory-representation problem: Capitolio appears to display regulatory footer data that corresponds to another financial institution or was copied from another website template. For a payment and crypto-infrastructure provider, such ambiguity is not harmless. It should be corrected or explained.

Beneficial Ownership and Management: What Is Publicly Visible?

Capitolio’s public website identifies the legal entity, jurisdiction, MSB registration, address, services, compliance policies, and regulatory caveats. It does not clearly disclose ultimate beneficial owners, controlling shareholders, directors, or senior managers in the pages reviewed.

That is a material gap. A company appearing as payee in offshore casino payment flows should disclose who controls the entity, who is responsible for compliance, and who approved gaming-related merchants or payment partners.

The Alberta corporate registry may provide additional filing data through official searches. Until those filings are obtained and reviewed, FinTelegram treats Capitolio’s beneficial ownership and control structure as unresolved.

Compliance Assessment

1. Apparent Collection Role in Casino Deposit Flow

In the tested 1Go Casino Revolut/Yapily rail, Capitolio appeared as the visible beneficiary of player funds. FinTelegram’s view is direct: Capitolio was not a passive observer in the tested payment screen. It was the named payee.

This places Capitolio at the collection end of a casino-origin payment flow.

2. Non-Casino Payee Risk

The player starts at 1Go Casino, but the Revolut/Yapily screen shows Capitolio. This payee mismatch creates the risk that regulated institutions classify the transaction as a transfer to a Canadian MSB/payment infrastructure provider rather than as a casino deposit.

3. Open-Banking Chokepoint Risk

The presence of Yapily Connect UAB and Revolut OBA in the flow shows how open banking can become the final authorisation layer for offshore gambling payments. Capitolio’s appearance as payee raises the question of whether the upstream casino context was visible to Yapily and Revolut.

4. Crypto Infrastructure Risk

Capitolio markets fiat-to-crypto and crypto-to-fiat infrastructure, digital-asset conversion, payout channels, and OTC liquidity. Those services are high-risk by nature and require strong merchant monitoring, especially where the upstream merchant environment includes online gambling.

5. Gaming Targeting Risk

Capitolio explicitly markets to Gaming & Digital Economy and says its infrastructure enables players and users to fund accounts, purchase digital assets, and withdraw earnings. That does not make its activity unlawful. But it makes the 1Go Casino finding highly relevant.

6. Regulatory Representation Risk

The unexplained CSSF/RCS footer references create an avoidable but serious credibility issue. Payment-infrastructure providers must be precise about regulatory status. Copy-pasted or unexplained regulatory identifiers can mislead merchants, counterparties, or users.

Questions for Capitolio

FinTelegram invites Capitolio to answer the following questions:

- Did Capitolio onboard 1Go Casino, Galaktika N.V., or any intermediary connected to the 1Go Casino cashier?

- Why did CAPITOLIO INC. appear as the visible payee in the tested 1Go Casino Revolut/Yapily payment flow?

- Was Capitolio acting as merchant of record, payment agent, collection agent, settlement intermediary, processor, or crypto on/off-ramp provider?

- Did Capitolio know that the payment originated from a casino cashier?

- What KYB and merchant due diligence did Capitolio perform on the upstream merchant and gateway stack?

- Did Capitolio classify the transaction as gambling-related?

- What was the role of BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily Connect UAB, and Revolut in relation to Capitolio?

- Does Capitolio provide services to offshore casino operators, gambling affiliates, gaming payment agents, or crypto-casino infrastructure providers?

- Who are Capitolio’s ultimate beneficial owners and controlling persons?

- Why do Capitolio webpages display CSSF/RCS identifiers that also appear on Banking Circle’s regulatory-information page?

Conclusion

Capitolio is exactly the type of entity FinTelegram’s Rail Atlas was designed to identify.

It sits at the intersection of open banking, crypto conversion, payouts, account funding, gaming platforms, and regulated payment rails. In the 1Go Casino review, CAPITOLIO INC. did not appear in a footnote. It appeared as the visible payee in the tested Revolut/Yapily payment flow.

That matters.

A player started inside an offshore casino cashier. After passing through multiple gateway layers, the payment reached Revolut and Yapily. The beneficiary shown was CAPITOLIO INC., a Canadian MSB and digital-asset/payment infrastructure provider — not the casino brand.

This is the recurring compliance problem: the consumer-facing merchant is gambling, but the bank-facing payee may be a payment infrastructure company. If banks, payment-initiation providers, and regulators cannot see through this structure, then open banking becomes a high-risk funding rail for offshore casinos.

Capitolio should explain its role. Yapily and Revolut should explain what upstream merchant context they saw. Regulators should ask whether Canadian MSB infrastructure is being used as a collection layer for European offshore casino deposits.

FinTelegram will continue following the rail.

Whistleblower Call

FinTelegram invites insiders, former employees, casino players, payment-processing staff, compliance officers, merchant-onboarding teams, PSP partners, and open-banking specialists to provide information about CAPITOLIO INC., its merchants, processors, banks, crypto partners, gaming clients, and settlement flows.

We are particularly interested in information about Capitolio’s beneficial owners, merchant onboarding files, casino or gaming clients, relationships with BillBlend, SegoPay, Tryzto, InstantBankPayment, Yapily, Revolut, or related payment gateways, payment descriptors, beneficiary names, bank-account details, crypto on/off-ramp flows linked to online casinos, and internal AML/CFT concerns.

Information can be submitted confidentially through the Whistle42 whistleblower system.

{kind=link}