Editorial Note: The legal notice was signed by a person identifying himself as Hennadii Postnov, Director of Capitolio Inc. FinTelegram has not yet been able to independently verify this individual’s director status from publicly accessible sources. Capitolio is invited to provide an Alberta corporate registry extract, director resolution, or other evidence confirming Mr. Postnov’s authority to act for the company.

After FinTelegram identified CAPITOLIO INC. as the visible payee in a tested 1Go Casino Revolut/Yapily open-banking deposit flow, the Canadian MSB demanded removal of the report. But Capitolio’s own notice does not refute the key payment-rail finding. On the contrary, it confirms that Capitolio appears as named payee in transactions processed through its open-banking on-ramp infrastructure. Since publication, Capitolio appears to have corrected regulatory information on its website, and 1Go Casino appears to have removed the Revolut option from its cashier. This is precisely why FinTelegram’s Rail Atlas matters.

2-Minutes Briefing

FinTelegram’s Rail Atlas was created to document how offshore casino deposit flows travel through payment gateways, open-banking providers, wallets, crypto rails, and regulated chokepoints before reaching the final bank-facing payment screen. The recent 1Go Casino / Capitolio case provides a useful methodology example.

Read the 1Go Casino rail analysis here.

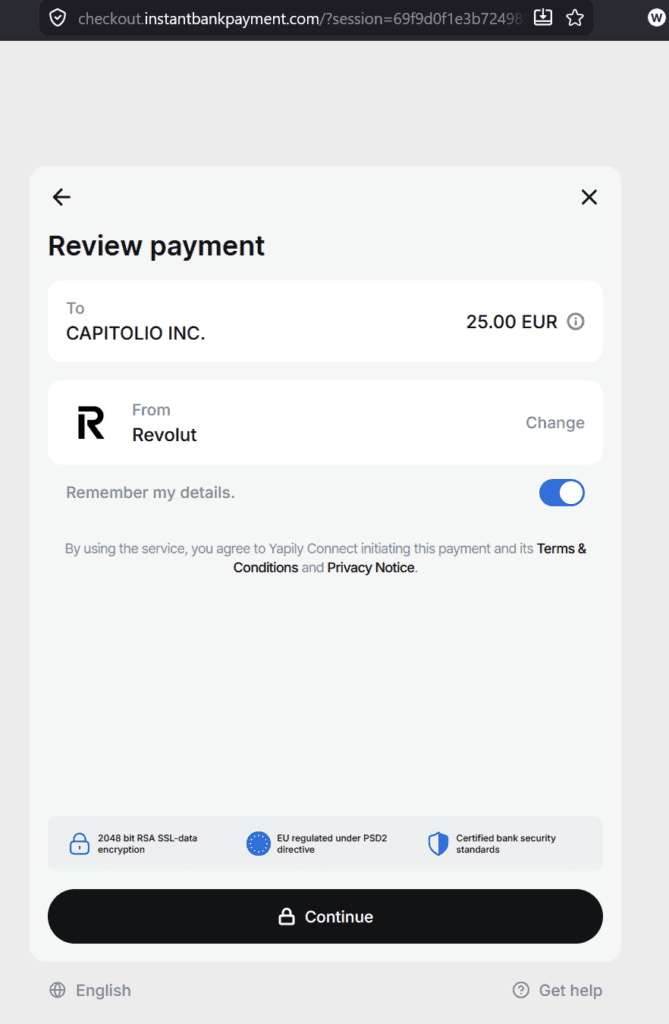

In the original FinTelegram review, a tested 1Go Casino deposit flow led from the casino cashier through several gateway layers and ultimately to a Revolut/Yapily open-banking screen where CAPITOLIO INC. appeared as the visible payee.

Capitolio later sent FinTelegram a formal legal notice demanding removal of the article. The notice alleges defamation and demands full removal, but it does not appear to refute the central screenshot-based finding. Instead, Capitolio states that it appears as named payee in transactions processed through its Open Banking on-ramp infrastructure, describing this as standard technical architecture.

That statement is important. It means the core issue is not whether FinTelegram correctly saw Capitolio as payee. Capitolio’s position appears to confirm that this can be the normal setup for its on-ramp infrastructure. The real question is whether open-banking rails, PISPs, PSPs, MSBs, and banks can detect the underlying commercial purpose when the user starts inside an offshore casino cashier but the bank-facing payee is a payment-infrastructure entity.

Since the publication, two further developments strengthen the Rail Atlas thesis:

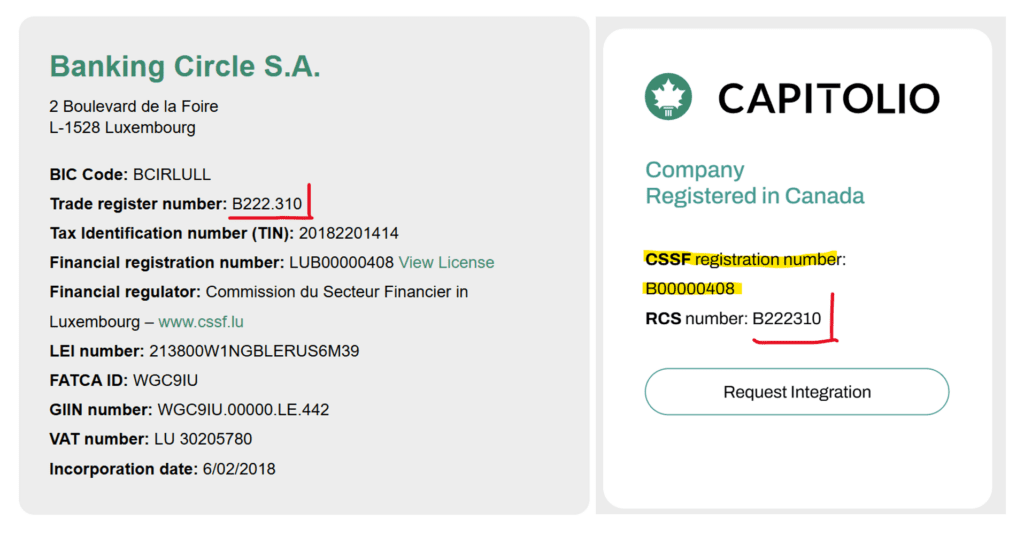

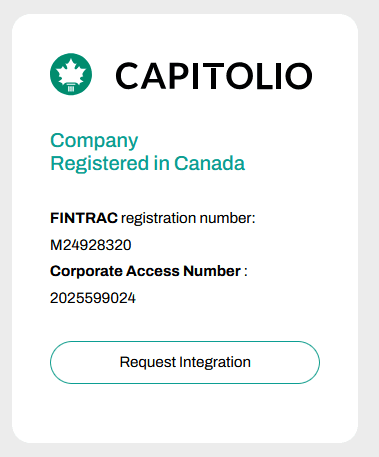

- First, Capitolio appears to have modified its website. Earlier screenshots showed Capitolio displaying CSSF registration number B00000408 and RCS number B222310 under the headline “Company Registered in Canada.” Those identifiers match Banking Circle’s Luxembourg regulatory references; Banking Circle’s own website identifies Banking Circle S.A. as a Luxembourg credit institution supervised by the CSSF and lists financial registration number LUB00000408 and trade register number B222.310, with its footer also showing CSSF registration number B00000408 and RCS number B222310. Capitolio’s current public pages now present the Canadian registration and FINTRAC information, including FINTRAC registration M24928320 and Corporate Access Number 2025599024.

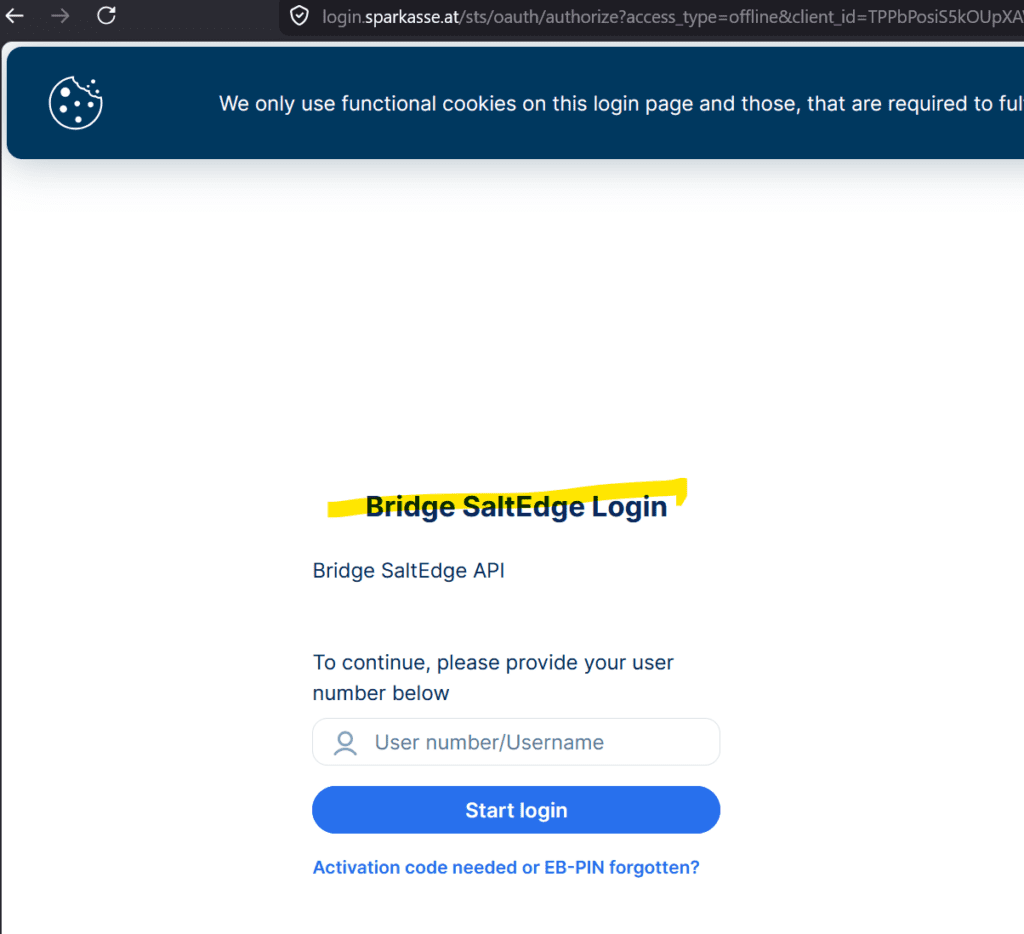

- Second, a fresh review of the 1Go Casino cashier indicates that the Revolut rail has apparently been removed, while other open-banking / Pay by Bank rails remain available. In the updated review, FinTelegram again found Domus Payment Solutions as payee in a Pay by Bank rail, and an additional open-banking route led via

secure.bankgate.iotoward a bank login interface showing Bridge SaltEdge API. Salt Edge publicly markets payment initiation and open-banking products, and Bridge documentation describes open-banking payment initiation functionality.

This is the broader message: payment-rail reporting works. It creates visibility. It forces processors to respond. It causes infrastructure changes. And it exposes the structural weakness in open-banking casino payments: the visible payee may not be the player-facing casino brand.

Key Findings

- Capitolio demanded removal of FinTelegram’s report but did not identify a clear factual error in the core rail evidence. The notice mainly objects to categorisation, framing, lack of pre-publication contact, and personal-data handling.

- Capitolio appears to confirm the central payee finding. Its notice states that Capitolio appears as named payee in transactions processed through its Open Banking on-ramp infrastructure.

- This confirmation is methodologically important. It supports FinTelegram’s core Rail Atlas concern: in open-banking rails, the bank-facing payee may be the infrastructure/on-ramp provider rather than the underlying merchant or casino brand.

- FinTelegram made proportionate editorial adjustments. The category “Illegal Payment Services” was removed, a personal name was removed, and the word “scheme” was replaced with “operating model.” These changes do not alter the core payment-rail finding.

- Capitolio appears to have corrected its website after publication. Earlier evidence showed CSSF/RCS identifiers matching Banking Circle references; the currently visible Capitolio pages now present Canadian and FINTRAC registration details. Capitolio identifies itself as an Alberta corporation and FINTRAC-registered MSB with registration number M24928320.

- The original CSSF/RCS issue was real and relevant. Banking Circle’s official regulatory-information page lists the same Luxembourg-style identifiers: CSSF registration number B00000408 and RCS number B222310.

- The 1Go Casino cashier appears to have changed after FinTelegram’s report. A fresh FinTelegram review indicates that the Revolut option was removed from the cashier, while Pay by Bank and crypto-related rails remained visible.

- Domus Payment Solutions still appeared as payee in a Pay by Bank rail. This means the non-casino-payee issue did not disappear; it shifted to another rail.

- Bridge / SaltEdge appeared in the updated open-banking route. The updated review showed a bank login page referencing Bridge SaltEdge API, reached after routing through

secure.bankgate.io. Salt Edge and Bridge both publicly describe open-banking / payment-initiation infrastructure.

What Capitolio’s Notice Actually Says

Capitolio’s notice is framed as a formal legal demand. It alleges that FinTelegram’s article is inaccurate, misleading, and defamatory, and it demands complete removal. It relies on Alberta defamation law, Austrian law, EU platform rules, and GDPR arguments.

However, from a Rail Atlas perspective, the most important sentence is not the legal threat. It is this position:

Capitolio states that it appears as named payee in all transactions processed through its Open Banking on-ramp infrastructure.

Capitolio presents this as a defence: it says the payee appearance is a standard technical architecture and not a compliance violation. FinTelegram’s interpretation is different.

The fact that Capitolio appears as payee may indeed be part of its technical model. But that is exactly why the case matters. If the technical architecture of an open-banking on-ramp means that the infrastructure provider appears as the visible payee for casino deposits, then the decisive compliance question becomes:

Does the bank, PISP, MSB, processor, and transaction-monitoring system still see the upstream casino context?

If not, open banking can create payment-purpose dilution.

Capitolio’s Position vs. FinTelegram’s Interpretation

| Issue | Capitolio’s Position | FinTelegram’s Interpretation |

|---|---|---|

| Payee appearance | Capitolio says it appears as named payee in transactions processed through its Open Banking on-ramp infrastructure. | This confirms the observed payee role. The unresolved question is whether the upstream casino context was visible and monitored. |

| Technical architecture | Capitolio argues this is standard and not a violation. | Standard architecture can still create systemic compliance risk if it masks the underlying merchant purpose. |

| 1Go Casino connection | Capitolio disputes FinTelegram’s framing and demands removal. | The screenshot-based finding remains: a tested 1Go Casino flow showed CAPITOLIO INC. as payee. |

| Article categories | Capitolio objected to “Illegal Gambling” and “Illegal Payment Services.” | FinTelegram removed “Illegal Payment Services” and can keep the focus on payment-rail evidence, not adjudicated liability. |

| “Scheme” wording | Capitolio objected to the word “scheme.” | FinTelegram replaced it with “operating model.” |

| Compliance officer name | Capitolio objected to personal-data use. | FinTelegram removed the personal name. |

| Core Rail Atlas issue | Capitolio says no compliance violation is established. | FinTelegram says the structure raises legitimate questions about merchant visibility, KYB, payment-purpose classification, and casino-origin funds. |

Why the Capitolio Response is Interesting

The Capitolio letter is important because it illustrates a recurring pattern in payment-rail investigations. Payment processors and infrastructure providers may not deny the architecture. Instead, they may argue that the architecture is standard, technical, or necessary. That is not the end of the inquiry. It is the beginning.

If the architecture causes a bank-facing payee to differ from the consumer-facing merchant, then compliance teams must ask:

- Who is the real merchant?

- Who onboarded the merchant?

- Who knows the payment is casino-related?

- What does the bank see?

- What does the PISP see?

- What does the MSB see?

- What does the consumer see?

- Is the payment classified as gambling, gaming, crypto, or ordinary services?

- Are high-risk jurisdictions and unlicensed gambling markets blocked?

The answer cannot simply be: “This is how open banking works.” If open banking works in a way that removes the casino brand from the bank-facing payee layer, then regulators should examine whether the model creates a blind spot.

The Website Correction: Why the CSSF/RCS Issue Matters

One of FinTelegram’s findings in the Capitolio article concerned an unusual regulatory-information issue. Earlier screenshot evidence showed Capitolio’s website displaying:

Company Registered in Canada

CSSF registration number: B00000408

RCS number: B222310

That was problematic because CSSF/RCS identifiers are Luxembourg regulatory/company references, not Canadian corporate identifiers. Banking Circle’s official regulatory page lists Banking Circle S.A. as a Luxembourg credit institution supervised by the CSSF and provides financial registration number LUB00000408 and trade register number B222.310; its footer also displays CSSF registration number B00000408 and RCS number B222310.

FinTelegram did not claim that Capitolio was connected to Banking Circle. The issue was website integrity and regulatory representation. A Canadian MSB should not display unexplained Luxembourg banking identifiers that appear to correspond to another financial institution.

After the FinTelegram report, Capitolio appears to have modified the website. The currently visible Capitolio pages now present Canadian registration information, including FINTRAC registration number M24928320 and Alberta Corporate Access Number 2025599024.

That is a concrete impact. FinTelegram identified an apparent regulatory-information anomaly. The website appears to have been corrected. That is precisely what compliance reporting is supposed to achieve.

The Updated 1Go Casino Cashier: Revolut Removed, Rails Remain

A fresh FinTelegram review of the 1Go Casino cashier indicates that the Revolut tile has apparently disappeared from the visible payment options. The updated cashier still showed:

- Crypto Currency;

- ByBit;

- Pay by Bank;

- another Pay by Bank-style rail;

This suggests that the specific Revolut rail identified in the original report may have been removed or disabled after publication. If so, that would be another meaningful impact of the Rail Atlas report. However, the broader rail problem remains.

The updated 1Go Casino review found Domus Payment Solutions as payee in the Pay by Bank rail. In addition, the open-banking route now led through secure.bankgate.io and into a bank login page that displayed Bridge SaltEdge API.

Salt Edge publicly describes payment-initiation services as enabling payments through open-banking channels, and Bridge’s documentation describes open-banking payment initiation via payment requests.

This means the 1Go cashier may have changed rails, not necessarily reduced risk. The names may change. The methodology remains the same: follow the rail from the casino cashier to the bank-facing authorisation screen and identify the real payee, the PISP, the gateway, and the responsible processor.

The Updated 1Go Rail Map

Original Revolut / Yapily / Capitolio Rail

| Layer | Observed Element | Compliance Relevance |

|---|---|---|

| Casino front-end | 1Go Casino cashier | User starts a casino deposit. |

| Gateway layer | BillBlend | First visible payment-routing layer. |

| Gateway layer | SegoPay | Additional payment-routing layer. |

| Gateway layer | Tryzto | Opaque intermediary layer. |

| Open-banking bridge | InstantBankPayment | Bridge into bank/open-banking flow. |

| Regulated PISP layer | Yapily Connect UAB | User authorised Yapily through Revolut OBA. |

| Bank-facing endpoint | Revolut OBA | Final authorisation interface. |

| Visible payee | CAPITOLIO INC. | Non-casino payee shown at bank-facing layer. |

Updated Pay by Bank / Bridge / SaltEdge Route

| Layer | Observed Element | Compliance Relevance |

|---|---|---|

| Casino front-end | 1Go Casino cashier | User starts a casino deposit. |

| Payment option | Pay by Bank | Account-to-account deposit rail remains available. |

| Gateways | secure.bankgate.iocheckout.instantbankpayment.com | Routing layer into bank-authentication flow. |

| Open-banking interface | Bridge SaltEdge API | New or alternative open-banking layer observed in the updated review. |

| Open banking facilitators | Bridge by Perspecteev (https://bridgeapi.io) SaltEdge (https://saltedge.com) | Bridge (Perspecteev) and SaltEdge are operated by regulated financial service providers in the UK and France and should not facilitate illegal casinos. |

| Bank login | Selected bank login screen | User is directed into bank authentication. |

| Visible payee in related Pay by Bank flow | Domus Payment Solutions | Non-casino payee issue remains present in the 1Go cashier environment. |

Rail Atlas Methodology: The Lesson From Capitolio

The Capitolio case demonstrates why FinTelegram does not merely report “payment options.” It maps payment rails. A casino cashier screenshot is only the starting point. The relevant questions emerge only after following the user journey:

- Which gateway appears first?

- Which intermediary domains are used?

- Which regulated PISP or open-banking provider appears?

- Which bank authorisation screen appears?

- Who is the visible payee?

- Is the payee the casino brand, the operator, a payment agent, an MSB, or a third-party collection entity?

- Does the payment purpose remain visible as gambling?

- Do the rails change after public exposure?

The Capitolio case answers one of these questions in a particularly important way. Capitolio’s notice states that Capitolio appears as named payee in its open-banking on-ramp transactions. That may be technically standard for Capitolio. But in a casino-origin flow, it raises exactly the compliance issue FinTelegram identified.

The question is not merely whether the payee name is technically correct.

The question is whether the payment ecosystem understands that the money started as a casino deposit.

Why This Matters for Payment Processors

FinTelegram’s reporting is designed to create visibility and accountability across high-risk payment rails. The objective is not to attack legitimate payment innovation. The objective is to ensure that regulated and semi-regulated payment infrastructure is not used to support offshore casinos that target users in jurisdictions where they do not hold the required local licence.

1Go Casino is publicly associated with Galaktika N.V. and a Curaçao licence. Public casino pages identify Galaktika N.V. as the operator and reference Curaçao licence OGL/2024/169/0146. The Cyprus-based Unionstar Limited is named as the casinos payment agent. A Curaçao licence does not automatically authorise an operator to target players in every EU jurisdiction. In many European markets, online gambling requires local authorisation, national licensing, or strict compliance with domestic gambling rules.

This is where payment processors become relevant. If a casino cannot lawfully operate in a target jurisdiction, payment processors should not provide hidden or indirect funding channels into that market.

The key compliance expectation is simple: Do not let payment architecture turn an illegal or unauthorised casino deposit into an ordinary-looking bank transfer to a payment-infrastructure company.

Regulatory Questions Raised

The Capitolio response and the updated 1Go cashier raise several questions for regulators and payment firms:

- If an open-banking on-ramp provider appears as named payee, how is the underlying merchant shown to the user, the bank, and the PISP?

- If the payment originates in a casino cashier, who is responsible for classifying the transaction as gambling-related?

- Can banks detect casino-origin deposits where the visible payee is an MSB, PSP, or payment agent?

- Do PISPs and open-banking aggregators receive upstream merchant-category information from gateways and payment orchestrators?

- Are processors required to block merchants that target jurisdictions where the casino lacks local authorisation?

- What happens when a rail is removed after media exposure? Is the merchant terminated, migrated, or simply re-routed?

- Does the replacement of one rail with another indicate genuine compliance remediation or merely payment-rail rotation?

- Should open-banking consent screens disclose the underlying merchant and commercial purpose, not only the technical payee?

These are not theoretical questions. They are now visible in live casino payment flows.

Conclusion

Capitolio’s legal notice did not undermine FinTelegram’s Rail Atlas reporting. It strengthened the methodology.

The central finding was that CAPITOLIO INC. appeared as the visible payee in a tested 1Go Casino Revolut/Yapily open-banking deposit flow. Capitolio’s response did not clearly refute that. Instead, it stated that Capitolio appears as named payee in transactions processed through its open-banking on-ramp infrastructure.

That is exactly the point.

The payment industry may regard this as normal technical architecture. FinTelegram regards it as a critical compliance question when the upstream transaction originates from an offshore casino cashier. If the casino brand disappears before the transaction reaches the bank-facing layer, payment-purpose dilution has occurred.

The aftermath is also telling. Capitolio appears to have corrected its website after FinTelegram highlighted the CSSF/RCS anomaly. 1Go Casino appears to have removed the Revolut rail after FinTelegram exposed the Revolut/Yapily/Capitolio flow. But other rails remain, including Pay by Bank routes, Domus Payment Solutions as payee, and a newly observed Bridge/SaltEdge route through secure.bankgate.io.

That is the Rail Atlas lesson:

The rail may change.

The payee may change.

The gateway may change.

The compliance question remains.

FinTelegram will continue following the payment rails, documenting the chokepoints, and asking payment processors, PISPs, MSBs, banks, and regulators the same question:

Do your systems know when an ordinary-looking account-to-account payment is actually an offshore casino deposit?

Call for Information

If you, as a player or insider, have information about Capitolio or other payment facilitators in the casino industry, please share it with us via our whistleblower platform, Whistle42. If you have any relevant payment documents or screenshots, please send them to us.

{kind=link}